[Cross-posted from MusicTechPolicy]

by Chris Castle

A performance metric one hears from the digerati is the term “conversion rate.” “Conversion rate” for a streaming service usually means the rate at which users of an ad-supported free service are “converted” to paying users. That motivation is usually because they are so fed up with the advertising they are willing to pay. (This was one of the many failed pitches from Spotify before people stopped trying to justify hanging on until the IPO riches flowed in.)

YouTube, of course, has never been too terribly interested in anything that moves users away from advertising. That resistance (and potential internal competition between the massive ad sales team and the ever changing YouTube managers), may explain the many failed efforts at launching a YouTube subscription service by a company that knows more about user behavior than anyone in history. They just couldn’t seem to get it right for the longest time. You don’t suppose that YouTube’s apparent lack of interest in getting large numbers of users to substitute away from free to subscription was because YouTube made a lot more money from the ads than they ever would from the subscriptions?

One of the ways that YouTube (and Google) makes money from advertising is by taking money that is not theirs to take (sometimes called “monetizing” content). The civil law calls that act a claim of “conversion” and the criminal law calls it the crime of “theft”. Conversion and theft are two sides of the same coin and often one implies the other, albeit with different burdens of proof.

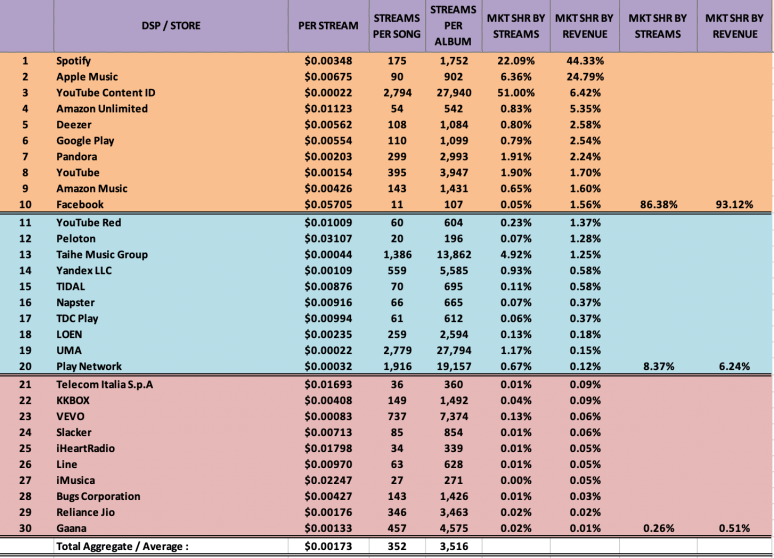

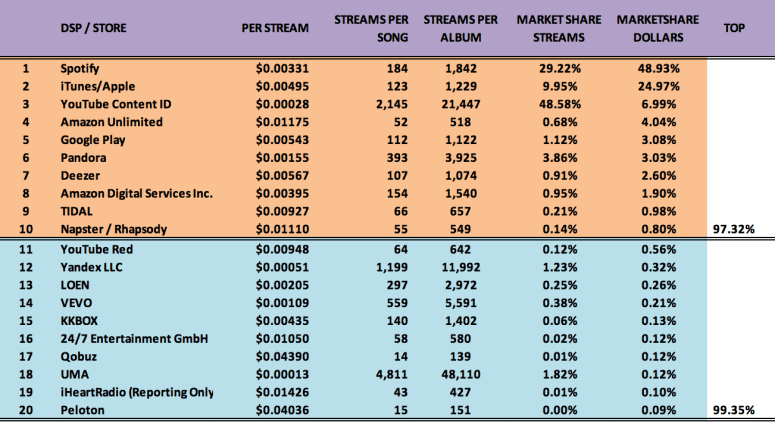

YouTube’s Content ID tool is a way for copyright owners to block or permit advertising on user-generated content that includes their copyrights, often music. Users of Content ID will tell you that it works just well enough that Google can say it is an effective tool, but even with Content ID music still gets through (and is often monetized by YouTube) for a variety of reasons. This requires time consuming and costly manual searches. Companies like AdRev make it a bit easier, but are essentially third party Content ID users. These companies are compensated with a commission on infringing works they find on YouTube that they convert–there’s that word again–from infringing to monetized, which means that YouTube now splits the advertising revenue with the copyright owners who in turn split their share with an AdRev.

But see what happened there? If you have Content ID, you can block on the upload some of the time, or you can do a search. If you don’t have Content ID (see Maria Schneider’s class action) then you can’t block on the upload only chase the infringements manually. But quite rightly from an economic perspective, companies like AdRev are not that interested in doing that work on a rev share basis if there’s no rev share when you block.

Here’s the point–you have a property right in your copyright. You have a property right to license that copyright. Any revenue derived from exploitations of that copyright is your money. YouTube uses its monopoly power to impose a deal to monetize your copyright (under duress, of course, due to whack a mole DMCA). That deal involves a revenue share. (Let’s just assume you decide to take the King’s shilling and accept Google’s deal under duress which you shouldn’t have to do and which may not even be enforceable.)

The question is, when should that revenue share attach–when they start exploiting your copyright in violation of your property rights or when you catch them doing it. And if (1) you catch them violating your property rights and (2) agree to monetize, when should they pay you your agreed upon share of the revenue from monetizing? Should they pay retroactively to the first exploitation? Or only prospectively after you catch them?

The correct answer is they should pay retroactively. But they don’t. They just keep the money. For millions of infringements. And they get away with it because of their monopoly power, which leaves one choice most artists won’t make, which is to sue them like Maria has.

Remember–Content ID operates largely like any other fingerprinting tool. (Psychoacoustic fingerprinting is old technology–remember Jonesy in “The Hunt for Red October”? That’s fingerprinting. A “fingerprint” is simply a mathematical rendering of the waveform of an audio file.)

There is a reference databases of recordings that are “known knowns” (which is why it is important to be included in the Content ID database as Maria Schneider correctly points out in her class action.) The fingerprinting tool encounters a new file, takes a fingerprint, then looks for a match in the reference database and reports a result that triggers an action. Typically, fingerprinting tools are binary: match or no match. What happens after the tool finds a match is entirely in the control of the operator. (So while the tool could have a match rate of 90%, the operator could report a random number of matches or a fixed number of matches, like one every ten, or one every 1000. That means 90% accuracy could turn into a much lesser percentage of reported matches. It’s important to know how many matches trigger an action.)

Having had some experience with audio fingerprints, I think you will find that once a fingerprint is in the reference database, the recognition tool (Content ID in this case) will spot the reference fingerprint a very, very high percentage of the time. The fingerprinting tool I’m most aware of caught matches over 90% of the time. I can’t imagine that a tool developed by the biggest technology company in commercial history would do less–unless they wanted it to. Remember, this is not taking into account re-records unless the re-record is itself in the database, or pitch bends. This is an exact match which is very common use of Content ID. (See Maria’s class action complaint, and Kerry Muzzey has a great description of this in his recent Senate testimony.)

If Content ID is actually missing matches to known knowns on the upload (assuming exact matching is possible), I find it very odd that Content ID is missing much. Maybe it’s not, but one way to find out is to force Google to reveal the inner workings through discovery in the class action case.

But if Content ID does miss exact matches, it would be interesting to know what percentage of those misses end up being monetized, and of those, what percentage end up getting caught later by a subsequent use of Content ID or a manual investigative process. This will give an idea of the scale of the retroactive payment issue.

As Maria rightly points out, it is virtually impossible for an artist or film maker without Content ID to catch YouTube monetizing infringing works. But I think the analysis has to go a step further–even if you have Content ID, at the moment you catch YouTube monetizing illegal versions, you are in no different position than the artist who lacks access to the Content ID tool.

Both have the same problem–YouTube is profiting from illegal copies. If when you catch them you then elect to monetize, YouTube will pay you going forward, i.e., prospectively. But I do not believe they will pay you retroactivelyfor the illegal use. (There is a rumor that some music publishers do get paid retroactively under some settlement, but that needs to be confirmed.)

That means that YouTube is directly profiting from piracy for the retroactive views which could total into the hundreds of millions per day given the massive number of daily views on YouTube. If you elect to monetize due to YouTube’s monopoly power, you are essentially releasing them from liability under duress. If you catch them.

So YouTube takes your property, monetizes it, and refuses to pay you for how much they made before you caught them if you ever do catch them. They dare you to sue them because you would be taking on the biggest company in commercial history that controls 90% of the access to information in the world and routinely defies governments. Not everyone has the spine of Maria Schneider.

Failing to license at all or failing to pay retroactively means that YouTube profits from piracy by converting your property to their own. And as Maria rightly points out, Google scrapes user data through non-display uses in the background even if YouTube is not monetizing overtly which they then use to compile user profiles in “millions of buckets” (which dribbled out before Judge Koh in the Gmail litigation (In Re: Google, Inc. Gmail Litigation, Case No. 13-MD-02430-LHK, (U.S.D.C. N.D. California, San Jose Division, Sept. 26, 2013)).

In either case, the value of the amount converted or stolen should rightly include the value of these user profiles scraped in the background, as well as the advertising revenue.

And don’t forget that Google is controlled by Larry Page, Sergei Brin, and Eric Schmidt through their “supervoting” shares of stock. It’s hard to believe that this YouTube policy was created without their blessing.

The simplest move for Google would be to simply pay both retroactively and (if the copyright owner elects to monetize) prospectively. Otherwise, it seems like a huge number of crimes are going on in a very planned and organized way dreamed up by YouTube and Google employees. “Dreamed up” is also called a conspiracy, and if there’s an actual conspiracy it’s not a theory (which came up in an interesting trade secret misappropriation RICO case against Google they managed to wriggle out of, at least for the moment).

The law has another word for organized theft at scale–we sometimes call it “racketeering.”

You must be logged in to post a comment.