David Lowery sits down with John Patrick Gatta at Jambands for a wide-ranging conversation that threads 40 years of Camper Van Beethoven and Cracker through the stories behind David’s 3 disc release Fathers, Sons and Brothers and how artists survive the modern music economy. Songwriter rights, road-tested bands, or why records still matter. Read it here.

David Lowery toured this year with a mix of shows celebrating the 40th anniversary of Camper Van Beethoven’s debut, Telephone Free Landslide Victory, duo and band gigs with Cracker, as well as solo dates promoting his recently-released Fathers, Sons and Brothers.

Fathers, the 28-track musical memoir of Lowery’s personal life explored childhood memories, drugs at Disneyland and broken relationships. Of course, it tackles his lengthy career as an indie and major label artist who catalog highlights include the alt-rock classic “Take the Skinheads Bowling” and commercial breakthrough of “Teen Angst” and “Low.” The album works as a selection of songs that encapsulate much of his musical history— folk, country and rock—as well as an illuminating narrative that relates the ups, downs, tenacity, reflection and resolve of more than four decades as a musician.

Spotify recently rolled out a quiet but seismic change to its royalty system: if a track doesn’t get at least 1,000 streams in a 12-month period, it earns no royalties. Zero. The company claims this policy is about reducing “fraud” and redirecting money to “working artists,” but behind that PR gloss is a shift that disproportionately harms independent musicians and smaller rightsholders.

Let’s be clear—this isn’t just about removing noise from the system. It’s about redrawing the map of who gets paid in the streaming economy and who gets pushed out.

The Hidden Impact on Artists

At first glance, 1,000 streams might sound like a modest hurdle. But in the aggregate, this threshold excludes potentially millions of tracks from ever receiving a dime—even though Spotify continues to profit from their presence through ad revenue and user engagement. It’s easy to assume the affected tracks belong only to DIY artists or obscure creators. But that’s not necessarily true.

Spotify’s royalty model is track-focused, not artist-focused. You could have a single that racks up a million streams while the rest of the album struggles to clear a few hundred. Those lower-performing tracks—despite being part of a cohesive release—won’t earn a cent. Left to its own devices, the platform favors individual track performance over albums or an artist’s entire catalog. And that has sweeping implications not only for how artists are paid, but for how music is created, released, and valued in the streaming age.

It’s Not About Growing the Pie—It’s About Cutting Out the Bottom

The most revealing part of this policy isn’t what it claims to fix, but what it quietly avoids. Spotify is likely under enormous pressure—from major labels and rights holders—to raise the artist payouts. No matter how much Spotify denies the per-stream rate, there will always be a per-stream rate even if they pay a “stream share” to a label for the very simple reason that the label has to convert that revenue share into a per stream rate in order to allocate it to their several artists. That’s as simple as gross vs. net.

Plus we know just how bad the gross is from indie artists who get paid 100% of the “stream share”. It’s shit, ok? That’s why we know Spotify are under pressure to increase royalties.

But arbitrarily raising the total royalty pool would have consequences: it could trigger most-favored-nation clauses, obligate Spotify to pay more across the board.

Another way to raise royalties would be to “flatten” some of the minimum guarantee, i.e., make a portion of it nonrecoupable from future royalty payments. This was the practice with record clubs—a nonrecoupable payment has the added benefit of not being shared with artists as a kind of catalog-wide payment. This would also likely trigger MFNs, so that’s not super appealing either.

So by excluding low-performing tracks from the royalty pool, Spotify isn’t reducing fraud or increasing fairness. It’s reallocating revenue. And not randomly—it’s redistributing it upward. The money those artists would have earned is now being handed to the top-performing tracks, which overwhelmingly belong to major labels and large catalog owners.

Don’t you think that if the goal was to reduce costs, Spotify would just shrink the pie and pocket the difference? It seems to me that more money to fewer people is likely the real purpose of the 1,000-stream rule.

The Threat of Industry-Wide Collusion

Spotify isn’t alone. Amazon Music and Deezer have introduced similar thresholds, raising serious concerns about whether this is a coordinated move by dominant platforms to marginalize smaller rightsholders. When multiple major services adopt the same gatekeeping metric at the same time, and benefit in the same way, it’s not unreasonable to ask whether they’re acting in lockstep. In fact, this concept in antitrust law is called tacit collusion (or “conscious parallelism”) which occurs when competitors coordinate their behavior—such as pricing or output—without explicit agreements or communication. Instead of entering into a formal cartel, companies mirror each other’s pricing or business strategies, knowing that mutual restraint benefits all of them

Even if there’s no smoking gun, the outcome is clear: fewer royalties paid to emerging and independent creators, and more concentrated control over who makes money from streaming.

Playlists, Penalties, and Platform Power

Here’s the twist: just because a track falls below 1,000 streams and no longer qualifies for royalties doesn’t mean Spotify stops using it. These sub-threshold tracks don’t vanish—they become part of what we might call Spotify’s “shadow catalog”: music that still populates playlists, fuels the recommendation algorithm, and keeps users listening, but doesn’t generate payouts.

Every time a user plays a low-performing track, Spotify collects engagement data. That information feeds into its personalization systems, sharpening the algorithm’s ability to retain users and increase time-on-platform. That extra engagement helps Spotify serve more ads, train better models, and keep listener churn down. It also enriches Spotify’s advertising and data ecosystem, especially on the free tier where listening time directly translates to ad revenue.

In other words, these unpaid tracks are still part of the machine. Spotify uses them to optimize engagement and advertising—but without paying the creators a cent. It’s profit without payout. Value extraction without compensation. And in the long tail of the music economy, that adds up to millions of tracks silently pulling their weight for free.

So it seems that this is the quid for the pro quo.

A Cautionary Tale for Songwriters

The 1,000-stream threshold is a cautionary tale for songwriters as they approach Phonorecords V. What began as a “fraud prevention” tool is now a benchmark for excluding smaller rights holders from royalties altogether. Streaming services will point to these thresholds as precedent—arguing that if labels can accept payout limits, publishers should too. Without strong opposition, platforms could push for mechanical royalty thresholds that mirror streamshare rules, cutting off compensation to low-earning songs. This isn’t just about recorded music anymore. It’s a warning: once a gate is built, it can be copied—and used to lock out songwriters next.

A Royalty System That Punishes the Wrong People

Spotify’s royalty threshold is spun as a way to fight fraud and reward “working artists,” you know, kind of like don’t be evil. But in reality, it codifies a system where only the most popular tracks get paid—regardless of how much they contribute to the overall value of the platform.

And when other streaming services follow the same path, it stops looking like business as usual and starts to resemble a coordinated effort to narrow the market and marginalize everyone but the top-tier players.

This isn’t a royalty system built on fairness or transparency. It’s a redistribution scheme—not to help more artists earn a living, but to serve bigger slices to fewer people.

And that should raise alarms far beyond the music industry. Looking at you, Gail Slater.

One of the hallmarks of mania is the rapid rise and complexity of the rates of fraud. And did you know they’re going up?

The Big Short, screenplay by Charles Randolph and Adam McKay, based on the book by Michael Lewis

We have often said that if screwups were Easter eggs, Spotify CEO Daniel Ek would be the Easter bunny, hop hop hopping from one to the next. That’s is not consistent with his press agent’s pagan iconography, but it sure seems true to many people.

This week was no different. Mr. Ek cashed out hundreds of millions in Spotify stock while screwing songwriters hard with a lawless interpretation of the songwriter compulsory license. That interpretation is so far off the mark that he surely must know exactly what he is doing. It’s yet another manifestation of Spotify’s sudden obsession with finding profits after a decade of “get big fast.”

The Bunny’s Bundle

Let’s look under the hood at the part they don’t tell you much about. Mr. Ek evidently has what’s called a “10b5-1 agreement” in place with Spotify allowing staggered sales of incremental tranches of the common stock. Those sales have to be announced publicly which Spotify complied with (we think). And we’ll say it again for the hundredth time, stock is where the real money is at this stage of Spotify’s evolution, not revenue.

As a founder of Spotify, Mr. Ek holds founders shares plus whatever stock awards he has been granted by the board he controls through his supervoting stock that we’ve discussed with you many times. These 10b5-1 agreements are a common technique for insiders, especially founders, who hold at least 10% of the company’s shares, to cash out and get the real money through selling their stock.

A 10b5-1 agreement establishes predetermined trading instructions for company stock (usually a sale so not trading the shares) consistent with SEC rules under Section 10b5 of the Securities and Exchange Act of 1934 covering when the insider can sell. Why does this exist? The rule was established in 2000 to protect Silicon Valley insiders from insider trading lawsuits. Yep, you caught it–it’s yet another safe harbor for the special people. Presumably Mr. Ek’s personal agreement is similar if not identical to the safe harbor terms because that’s why the terms are there.

As MusicBusinessWorldWide reported, Mr. Ek recently sold $118.8 million in shares of Spotify at roughly the same time that he likely knew Spotify was planning to change the way his company paid songwriters on streaming mechanicals, or as it’s also known “material nonpublic information”.

As Tim Ingham notes in MusicBusinessWorldwide, Mr. Ek has had a few recent sales under his 10b5-1 agreement: “Across these four transactions (today’s included), Ek has cashed out approximately $340.5 million in Spotify shares since last summer.” Rough justice, but I would place a small wager that Ek has cashed out in personal wealth all or close to all of the money that Spotify has paid to songwriters (through their publishers) for the same period. In this sense, he is no different than the usual disproportionately compensated CEOs at say Google or Raytheon.

Stock buybacks artificially increase share price. Now why might Spotify want to juice its own stock price?

Spotify Shoves a “Bundled” Rate on Songwriters

Spotify’s argument (that may have caused a jump in share price) claims that its recent audiobook offering made Spotify subscriptions into a “bundle” for purposes of the statutory mechanical rate. (While likely paying an undiscounted royalty to the books.)

That would be the same bundled rate that was heavily negotiated in the 2021-22 “Phonorecords IV” proceeding at the Copyright Royalty Board at great expense to all concerned, not to mention torturing the Copyright Royalty Judges. These Phonorecords IV rates are in effect for five years, but the next negotiation for new rates is coming soon (called Phonorecords V or PR V for short). We’ll get to the royalty bundle but let’s talk about the cash bundle first.

You Didn’t Build That

Don’t get it wrong, we don’t begrudge Mr. Ek the opportunity to be a billionaire. We don’t at all. But we do begrudge him the opportunity to do it when the government is his “partner” so they can together put a boot on the necks of songwriters. This is how it is with statutory mechanical royalties; he benefits from various other safe harbors, has had his lobbyists rewrite Section 115 to avoid litigation in a potentially unconstitutional reach back safe harbor, and he hired the lawyer at the Copyright Office who largely wrote the rules that he’s currently bending. Yes, we do begrudge him that stuff.

And here’s the other effrontery. When Daniel Ek pulls down $340.5 million as a routine matter, we really don’t want to hear any poor mouthing about how Spotify cannot make a profit because of the royalty payments it makes to artists and songwriters. (Or these days, doesn’t make to some artists.) This is, again, why revenue share calculations are just the wrong way to look at the value conferred by featured and nonfeatured artists and songwriters on the Spotify juggernaut. That’s also the point Chris made in some detail in the paper he co-wrote with Professor Claudio Feijoo for WIPO that came up in Spain, Hungary, France, Uruguay and other countries.

Spotify pays a percentage of revenue on what is essentially a market share basis. Market share royalties allows the population of recordings to increase faster than the artificially suppressed revenue, while excluding songwriters from participating in the increases in market value reflected in the share price. That guarantees royalties will decline over time. Nothing new here, see the economist Thomas Malthus, workhouses and Charles Dickens‘ Oliver Twist.

The market share method forces songwriters to take a share of revenue from someone who purposely suppressed (and effectively subsidized) their subscription pricing for years and years and years. (See Robert Spencer’s Get Big Fast.). It would be a safe bet that the reason they subsidized the subscription price was to boost the share price by telling a growth story to Wall Street bankers (looking at you, Goldman Sachs) and retail traders because the subsidized subscription price increased subscribers.

Just a guess.

The Royalty Bundle

Now about this bundled subscription issue. One of the fundamental points that gets missed in the statutory mechanical licensing scheme is the compulsory license itself. The fact that songwriters have a compulsory license forced on them for one of their primary sources of income is a HUGE concession. We think the music services like Spotify have lost perspective on just how good they’ve got it and how big a concession it is.

The government has forced songwriters to make this concession since 1909. That’s right–for over 100 years. A century.

A decision that seemed reasonable 100 years ago really doesn’t seem reasonable at all today in a networked world. So start there as opposed to the trope that streaming platforms are doing us a favor by paying us at all, Daniel Ek saved the music business, and all the other iconographic claptrap.

Has anyone seen them in the same room at the same time?

The problem with the Spotify move to bundled subscriptions is that it can happen in the middle of a rate period and at least on the surface has the look of a colorable argument to reduce royalty payments. If you asked songwriters what they thought the rule was, to the extent they had focused on it at all after being bombarded with self-congratulatory hoorah, they probably thought that the deal wasn’t “change rates without renegotiating or at least coming back and asking.”

And they wouldn’t be wrong about that, because it is reasonable to ask that any changes get run by your, you know, “partner.” Maybe that’s where it all goes wrong. Because it is probably a big mistake to think of these people as your “partner” if by “partner” you mean someone who treats you ethically and politely, reasonably and in good faith like a true fiduciary.

They are not your partner. Don’t normalize that word.

A Compulsory License is a Rent Seeker’s Presidential Suite

But let’s also point out that what is happening with the bundle pricing is a prime example of the brittleness of the compulsory licensing system which is itself like a motel in the desolate and frozen Cyber Pass with a light blinking “Vacancy: Rent Seekers Wanted” surrounded by the bones of empires lost. Unlike the physical mechanical rate which is a fixed penny rate per transaction, the streaming mechanical is a cross between a Rube Goldberg machine and a self-licking ice cream cone.

The Spotify debacle is just the kind of IED that was bound to explode eventually when you have this level of complexity camouflaging traps for the unwary written into law. And the “written into law” part is what makes the compulsory license process so insidious. When the roadside bomb goes off, it doesn’t just hit the uparmored people before the Copyright Royalty Board–it creams everyone.

David and friends tried to make this point to the Copyright Royalty Judges in Phonorecords IV. They were not confused by the royalty calculations–they understood them all too well. They were worried about fraud hiding in the calculations the same way Michael Burry was worried about fraud in The Big Short. Except there’s no default swaps for songwriters like Burry used to deal with fraud in subprime mortgage bonds.

Here’s how the Judges responded to David, you decide if they are condescending or if the songwriters were prescient knowing what we know now:

While some songwriters or copyright owners may be confused by the royalties or statements of account, the price discriminatory structure and the associated levels of rates in settlement do not appear gratuitous, but rather designed, after negotiations, to establish a structure that may expand the revenues and royalties to the benefit of copyright owners and music services alike, while also protecting copyright owners from potential revenue diminution. This approach and the resulting rate setting formula is not unreasonable. Indeed, when the market itself is complex, it is unsurprising that the regulatory provisions would resemble the complex terms in a commercial agreement negotiated in such a setting.

It must be said that there never has been a “commercial agreement negotiated in such a setting” that wasn’t constrained by the compulsory license. It’s unclear what the Judges even mean. But if what the Judges mean is that the compulsory license approximates what would happen in a free market where the songwriters ran free and good men didn’t die like dogs, the compulsory license is nothing like a free market deal.

If the Judges are going to allow services to change their business model in midstream but essentially keep their music offering the same while offloading the cost of their audiobook royalties onto songwriters through a discount in the statutory rate, then there should be some downside protection. Better yet, they should have to come back and renegotiate or songwriters should get another bite at the apple.

Unfortunately, there are neither, which almost guarantees another acrimonious, scorched earth lawyer fest in PR V coming soon to a charnel house near you.

Eject, Eject!

This is really disappointing because it was so avoidable if for no other reason. It’s a great time for someone…ahem…to step forward and head off the foreseeable collision on the billable time highway. The Judges surely know that the rate calculation is a farce

But the Judges are dealing with people negotiating the statutory license who have made too much money negotiating it to ever give it up willingly although a donnybrook is brewing. This inevitable dust up means other work will suffer at the CRB. It must be said in fairness that the Judges seem to find it hard enough to get to the work they’ve committed to according to a recent SoundExchange filing in a different case (SDARS III remand from 2020).

That’s not uncharitable–I’m merely noting that when dozens of lawyers in the mechanical royalty proceedings engage in what many of us feel are absurd discovery excesses. When there are stupid lawyer tricks at the CRB, they are–frankly–distracting the Judges from doing their job by making them focus on, well, bollocks. We’ll come back to this issue in future. The dozens and hundreds of lawyers putting children through college at the CRB–need to take a breath and realize that judicial resources at the CRB are a zero sum game. This behavior isn’t fair to the Judges and it’s definitely not fair to the real parties in interest–the songwriters.

Tell the Horse to Open Wider

A compulsory license in stagflationary times is an incredibly valuable gift, and when you not only look the gift horse in the mouth but ask that it open wide so you can check the molars, don’t be surprised if one day it kicks you.

[This is the first in a series of three short posts examining how Spotify scores as an Environmental, Social and Governance (or “ESG”) investment. “ESG” is a Wall Street acronym often attributed to Larry Fink at Blackrock that designates a company as suitable for socially conscious investing based on its “Environmental, Social and Governance” business practices, that is “ESG”. See the Upright Net Impact data model on Spotify’s sustainability score. As of this writing, the last update of Spotify’s Net Impact score was before the Neil Young scandal and, of course, rocketing energy prices that compound the environmental impact of streaming. These posts first appeared on MusicTechSolutions]

Spotify closes $24 higher than its first day of trading after destroying the incomes of thousands of artists and even more songwriters. pic.twitter.com/HeHXnEXVHh

Spotify has an ESG problem, and a closer look may offer insights into a wider problem in the tech industry as a whole. If a decade of destroying artist and songwriter revenues isn’t enough to get your attention, maybe the Neil Young and Joe Rogan imbroglio will. But a minute’s analysis shows you that Spotify was already an ESG fail well before Neil Young’s ultimatum.

Streaming is an Environmental Fail

I first began posting about streaming as an environmental fail years ago in the YouTube and Google world. Like so many other ways that the BIg Tech PR machine glosses over their dependence on cheap energy right through their supply chain from electric cars to cat videos, YouTube did not want to discuss the company as a climate disaster zone. To hear them tell it, YouTube, and indeed the entire Google megalopolis right down to the Google Street View surveillance team was powered by magic elves running on appropriate golden flywheels with suitable work rules. Or other culturally appropriate spin from Google’s ham handed PR teams.

Mission creepy meets the Sound of Music

Greenpeace first wrote about “dirty data” in 2011–the year Spotify launched in the US. Too bad Spotify ignored the warnings. Harvard Business Review also tells us that 2011 was a demarcation point for environmental issues at Microsoft following that Greenpeace report:

In 2011, Microsoft’s top environmental and sustainability executive, Rob Bernard, asked the company’s risk-assessment team to evaluate the firm’s exposure. It soon concluded that evolving carbon regulations and fluctuating energy costs and availability were significant sources of risk. In response, Microsoft formed a centralized senior energy team to address this newly elevated strategic issue and develop a comprehensive plan to mitigate risk. The team, comprising 14 experts in electricity markets, renewable energy, battery storage, and local generation (or “distributed energy”), was charged by corporate senior leadership with developing and executing the firm’s energy strategy. “Energy has become a C-suite issue,” Bernard says. “The CFO and president are now actively involved in our energy road map.”

If environment is a C-suite issue at Spotify, there’s no real evidence of it in Spotify’s annual report (but then there isn’t at the Mechanical Licensing Collective, either). “Environment” word search reveals that at Spotify, the environment is “economic”, “credit”, and above all “rapidly changing.” Not “dirty”–or “clean” for that matter.

The fact appears to be that Spotify isn’t doing anything special and nobody seems to want to talk about it. But wait, you say–what about the sainted Music Climate Pact? (Increasingly looking like a PR effort worthy of Edward Bernays.) Guess who hasn’t signed up to the MCP? Any streaming service as far as I can tell. There is a “Standard Commitment Letter” that participants are supposed to sign up to but I wasn’t able to read it. Want to guess why?

That’s right. You know who wants to know what you’re up to.

If you haven’t heard much about streaming’s negative effects on the environment, don’t be surprised. It’s not a topic that’s a great conversation starter and very few journalists seem to have any interest in the subject at all. I wonder why.

But if you’re an artist who is concerned about the impact of streaming your music on the environment or an investor trying to see your way through the ESG investment, this should give you a few questions to ask about Spotify’s ESG score. And if that slipped by you, don’t feel bad–Blackrock reportedly holds 3.8 million shares of Spotify that are worth less all the time, so they didn’t catch it either. And Blackrock coined the phrase.

Next: Spotify’s “Social” Fail: Rogan, Royalties and The Uyghurs

We hate to say we told ya so, but… Below is our post from September 2015. Two years ago we predicted the inevitable truth of the all you can eat Spotify subcription model. Like many of our predictionsand proposals (example; windowing titles) we’ve had to wait for the industry to catch up to us. Today, two years later, Digital Music News confirms our prediction.

Read the report from Digital Music News by clicking the headline link here.

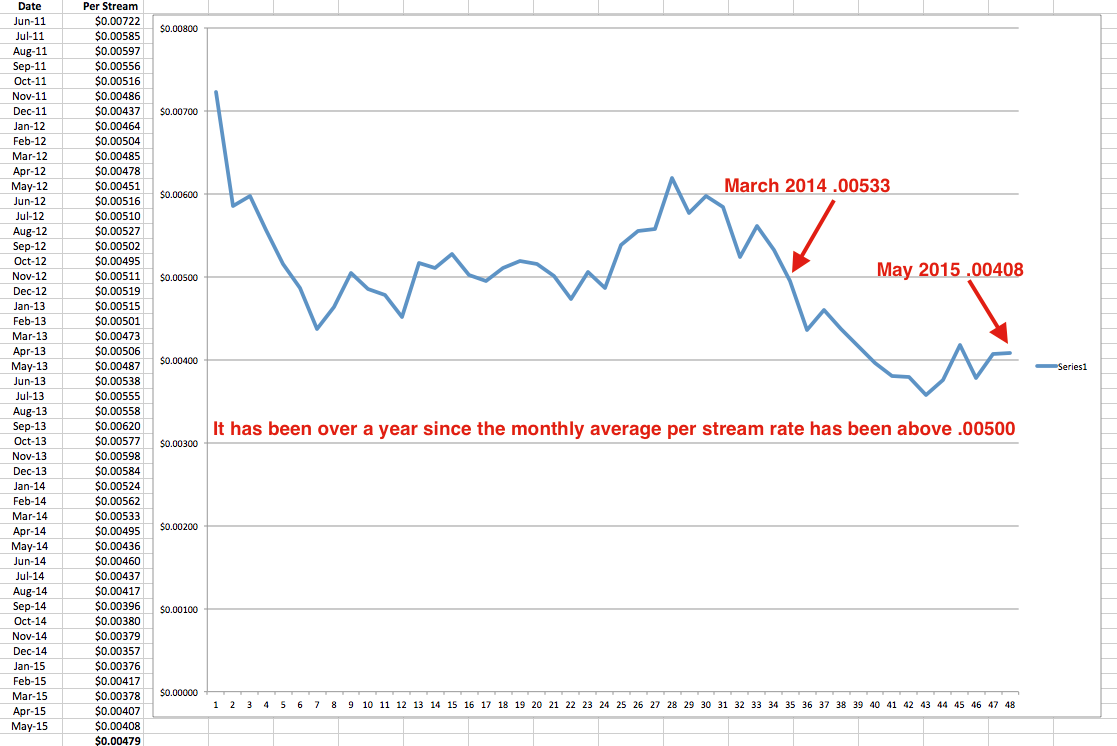

Down, down, down it goes, where it stops nobody knows… The monthly average rate per play on Spotify is currently .00408 for master rights holders.

48 Months of Spotify Streaming Rates from Jun 2011 thru May 2015 on an indie label catalog of over 1,500 songs with over 10m plays.

Spotify rates per spin appear to have peaked and are now on a steady decline over time.

Per stream rates are dropping because the amount of revenue is not keeping pace with the number of streams. There are several possible causes:

1) Advertising rates are falling as more “supply” (the number of streams) come on line and the market saturates.

2) The proportion of lower paying “free streams” is growing faster than the proportion of higher paying “paid streams.”

3) All of the above.

This confirms our long held suspicion that as a flat price “freemium” subscription service scales the price per stream will drop. As the service reaches “scale” the pool of streaming revenue becomes a fixed amount. The pie can’t get any larger and adding more streams only cuts the pie into smaller pieces!

The data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $4,080 / 1,000,000 = .00408 per stream). Multiple tiers and pricing structures are all summed together and divided to create an averaged, single rate per play.

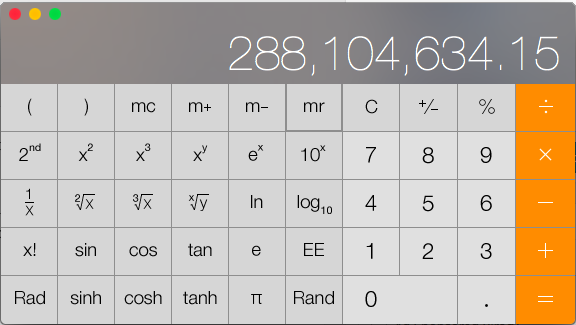

Spotify just posted their financials and Paul Resnikoff at Digital Music News was quick to point out that the average Spotify employee salary is $168, 747.

Contrast that to the plight of songwriters. There would be no music business without the fundamental efforts of songwriters. Yet, there is not a free market in songs. The federal government sets compensation for songwriters/publishers based on a percentage of revenue. An abysmal below market rate. In effect a subsidy for streaming services. Last I checked this rate was working out to about $0.00058 per spin. This includes both the public performance (BMI/ASCAP) and the streaming mechanical (IF they happen to pay it).

Best case scenario, if a songwriter retains all publishing rights to their song then a songwriter would need 288,104,634.15 spins to earn the reported average salary of a Spotify employee.

Music Business Worldwide is reporting that “GLOBAL MUSIC PIRACY DOWNLOADS GREW BY ALMOST A FIFTH IN 2015″.

The amount of music downloaded on illegal piracy sites grew by 16.5% in the second half of 2015 compared to the year’s opening six months.

That’s according to leading content protection and market analytics company MUSO, which tracked web activity on 576 sites which were ‘wholly dedicated to music piracy or contained significant music content’.

Across these sites, MUSO analysed over 2 billion visitor traffic hits globally.

Adele, Taylor Swift, Beyonce’, Coldplay and more artists are fully understanding the value of not giving away their work for free right out of the gate. This is especially important during the biggest consumer spending season of the year. Why would anyone with a solid fan base and known demand for their work give it away for free during most profitable window of the year? This then begs the question how many more records would you be selling this holiday season if your record was not available on free streaming platforms?

Spotify and other free streaming services should be structured more like Netflix. The film industry understands the value of strategic pricing in the context of time based value propositions. Friday night block buster movies are not available on Netflix at the same time for a good reason.

There has been a lot of good work and innovation by the film industry to create “day and date” titles that are available both in theaters and as video on demand at the time of release. However none of these are made available free to consumer on an advertising supported platform. In fact, all the major film and tv streaming services require payment of some kind, be it subscription (HuluPlus, Netflix, Amazon Prime) or transactional fees for rental or permanent download (Itunes, Amazon, Vudu).

“Or Else They’ll Steal It!”

The only argument that is ever made against the use of windows is that tired old song that they like to sing in Silicon Valley called, “Or Else They’ll Steal It.” The problem is of course, they’re already stealing it, and will continue to steal it until there are real consequences to not do so. But the film and tv industries are not listening to the song of Stockholm Syndrome. Instead the film and tv industries continue to innovate and experiment with new windows, digital distribution models and competitive pricing based on the new value propositions.

Converting consumers from “pirate 2 paid” is dependent upon giving consumers more value and pricing options, not less. If the record industry doubts this for even a split second the proof is expressed in a single word, “vinyl.”

By contrast the record industry has given away valuable profits to tech companies like Spotify who give little in return for the high value products that are being licensed. The ubiquity of distribution on streaming platforms drives the price of all products to zero.

Windowing allows for price elasticity and rewards consumers who are willing to spend more for the premier product or experience. Of course, for windowing to work there has to be a fair and regulated marketplace where artists and rights holders actually can withhold their work from various platforms should they chose to do so.

If we’ve learned anything at all in 2015 it is that YouTube is probably the single greatest threat to the ability of artists and rights holders to have a long term sustainable business. There can be no windows if everything appears on YouTube via User Pirated Content anyway.

The grand irony here is that in a well controlled and regulated distribution system, it is far more likely that all stakeholders would have the ability to generate greater profits within their sectors. We now have a decade and a half of data behind us while heading towards the second half, of the second decade, of the new millennium. It’s time to for the adults to put an end to play time. It’s just math and common sense.

Windows work. Period.

Business decisions need to developed through common sense, innovation and time tested principles of basic economics. We’ll repeat our previous suggestion for an industry wide, consistent windowing platform strategy below.

Windowing works better when there is a reasonable amount of consistency. Our friends in the film business have been highly effective at windowing for decades and there’s no reason why it can’t work similarly well for the record business.

Every new release should have the option to determine the release windows when the record is being set up. For example the default could be 0,30,60,90 day option for transactional sales, followed by 0,30,60,90 day option for Subscription Streaming prior to being available for Free Streaming.

Windowing is not new for the record business. The industry has never had pricing ubiquity across all releases, genres and catalogs. There has always been strategic and flexible pricing strategies to differentiate developing artists, hits, mid-line catalog, and deep catalog. An industry wide initiative to re-allign time proven price elasticity is the key to growing the business and developing a broad based sustainable ecosystem for more artists.

Windowing allows for Free Streaming to exist as a strategic price point.

Windowing allows for Subscription Streaming to exist as a strategic price point.

Windowing allows for Transactional Downloads to exist as a strategic price point.

Windowing allows for artists and rights holders to determine the best and most mutually beneficial way to engage with their fans.

Windowing is the key (as it always has been) in rebuilding a sustainable and robust professional middle class that will inevitably lead to more artists ascending to the ranks of stars. Some will become superstars and legends capable of creating the types of sales and revenues currently achieved by Adele, Taylor Swift and Beyonce’. To get there however we need to abandon Stockholm Syndrome and embrace windowing that works for everyone.

Today’s younger consumers who missed the glory days of the record store as a cultural hub will probably have little awareness of the cut-out bin. The cut-out bin was dreaded by artists and labels alike, but it served an important function in the ecosystem and economy of record sales. This was the rack in the record store where over manufactured titles made their last stop before the trash bin.

The cut-out bin was the last stop for an album, not the first stop. This is a very important consideration in today’s digital music economy. Artists, you deserve better service from your labels, management and partners.

Having your record appear in “the cut-outs” didn’t mean the album wasn’t successful, to the contrary, many of the records in cut-out bins were by well known name artists. Many of these records contained hit songs and singles. However, for whatever reason the quantities manufactured exceeded the markets ability to absorb those units into sales. At some point the decision was made to either monetize the overstock, or destroy the overstock.

The net result of the cut-out bin was that full length albums were often priced below the cost of a current 45 rpm single. However, this pricing distinction occurred at least a year or more after the initial release of the album. An album was “cut-out”after all of the front line sales, traditional discounts and higher margin retail channels had long been exhausted. Cut-out supplies were also limited and inconsistent. In other words, it was only the most patient and adventurous consumer who benefited from this deep discount.

Honestly, who would buy an album at full price if the same exact product (sans for the cut off top right corner) could be had for less than the price of current single?

So here we are a decade and a half into the new millennium and the best “new business model” for artists and rights holders in the 21st Century Digital Economy is to start at the last stop on the value chain? You’re kidding us, right? We wish.

So how did we get here? Well, in three words “Ad Funded Piracy.” The lowest price for a product or service sets the price floor for all other comparable products. In the case of music that price has been set at about zero for over a decade and a half. But that’s not say there’s no money being made in the distribution of music online. No, there’s actually a lot of money being made by the Internet Advertising Networks supplying the advertising that fuels the corporate profits to over half a million infringing pirate sites.

It should also be noted that the CEO of the leading ad-funded, free to consumer streaming service was also the creator of the most successful ad-funded, bit-torrent client, u-torrent. Yup, that’s none other than Spotify’s Daniel Ek. Shocker, right?

Obviously, pirates and thieves are going to pirate and steal. These people should not be the first concern of business executives seeking to expand their profits on digital platforms. Enterprise level piracy requires the political will to enforce the law against egregious digital robber barons. Anti-Piracy is an “in addition to” action, not an “instead of” action. The future of the music business must be rooted in both innovation and advocacy.

Windows work. Period.

Business decisions need to developed through common sense, innovation and time tested principles of basic economics. We’ll repeat our previous suggestion for an industry wide, consistent windowing platform strategy below.

Windowing works better when there is a reasonable amount of consistency. Our friends in the film business have been highly effective at windowing for decades and there’s no reason why it can’t work similarly well for the record business.

Every new release should have the option to determine the release windows when the record is being set up. For example the default could be 0,30,60,90 day option for transactional sales, followed by 0,30,60,90 day option for Subscription Streaming prior to being available for Free Streaming.

Windowing is not new for the record business. The industry has never had pricing ubiquity across all releases, genres and catalogs. There has always been strategic and flexible pricing strategies to differentiate developing artists, hits, mid-line catalog, and deep catalog. An industry wide initiative to re-allign time proven price elasticity is the key to growing the business and developing a broad based sustainable ecosystem for more artists.

Windowing allows for Free Streaming to exist as a strategic price point.

Windowing allows for Subscription Streaming to exist as a strategic price point.

Windowing allows for Transactional Downloads to exist as a strategic price point.

Windowing allows for artists and rights holders to determine the best and most mutually beneficial way to engage with their fans.

Windowing is the key (as it always has been) in rebuilding a sustainable and robust professional middle class that will inevitably lead to more artists ascending to the ranks of stars. Some will become superstars and legends capable of creating the types of sales and revenues currently achieved by Adele, Taylor Swift and Beyonce’. To get there however we need to abandon Stockholm Syndrome and embrace windowing that works for everyone.

Down, down, down it goes, where it stops nobody knows… The monthly average rate per play on Spotify is currently .00408 for master rights holders.

48 Months of Spotify Streaming Rates from Jun 2011 thru May 2015 on an indie label catalog of over 1,500 songs with over 10m plays.

Spotify rates per spin appear to have peaked and are now on a steady decline over time.

Per stream rates are dropping because the amount of revenue is not keeping pace with the number of streams. There are several possible causes:

1) Advertising rates are falling as more “supply” (the number of streams) come on line and the market saturates.

2) The proportion of lower paying “free streams” is growing faster than the proportion of higher paying “paid streams.”

3) All of the above.

This confirms our long held suspicion that as a flat price “freemium” subscription service scales the price per stream will drop. As the service reaches “scale” the pool of streaming revenue becomes a fixed amount. The pie can’t get any larger and adding more streams only cuts the pie into smaller pieces!

The data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $4,080 / 1,000,000 = .00408 per stream). Multiple tiers and pricing structures are all summed together and divided to create an averaged, single rate per play.

You must be logged in to post a comment.