The USC Lecture Serialized Into Chapters for easier viewing.

Read The Blog Post Here:

https://medium.com/@jonathantaplin/sleeping-through-a-revolution-8c4b147463e5

Watch the Full Lecture Here:

The USC Lecture Serialized Into Chapters for easier viewing.

Read The Blog Post Here:

https://medium.com/@jonathantaplin/sleeping-through-a-revolution-8c4b147463e5

Watch the Full Lecture Here:

We can’t help but think these two things are related. Read the full stories at DMN… Here and Here…

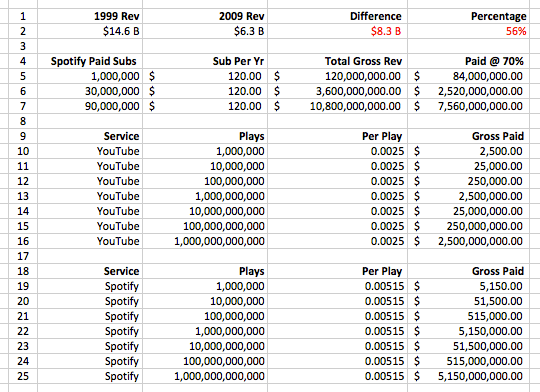

So how’s that $3.00 per “user” annual ARPU working out from free streaming?

It’s amazing to us that the current conversation and controversy is still focused on the free tier. We’re not entirely certain that Spotify can even work at $10 a month / $120 per yer, per subscriber. The number of subscribers needed to replace the revenue from transactional sales exceeds those of any current mature subscription business.

It will take 60 Million PAID subscribers at $10 a month to generate about $7.2b in gross revenues annually. It takes another 30 Million (or 90 Million PAID Total) to come up with $7.5b payable to rights holders. Ninety Million. Paid…

Here’s some context for the chart above. Netflix only has 36m subscribers in the US, no free tier, and massive limitations on available titles of both catalog and new releases. Sirius XM, 26.3m in the US as a non-interactive curated service installed in homes, cars and accessible online. Premium Cable has 56m subscribers in the US paying much more than $10 a month and also with many limitations. Spotify… 3m paid subscribers in the US after four years. Tell us again about this strategy of “waiting for scale.” Three Million Paid… Three…

* 3m Spotify Subs Screen Shot

* 26.3m Sirius XM Subs Screen Shot

* 36m Netflix Subs Screen Shot

* 56m Premium Cable Subs Screen Shot

* $7b Music Business Screen Shot

It’s just math.

Whatever the reason, it’s bullshit. The major labels were right not to compromise with Napster. I was VP of Electronic Music Distribution at Sony Music at the time, dealing with these issues day to day. Understandably, some people may think, what does it matter if the majors were right or not? They lost. But I think its important to understand the various facets and history of these events, if only to provide perspective for issues the industry is still dealing with today. So, at the risk of being unhip, here are Five Reasons Why The Major Labels Didn’t Blow It With Napster.

READ THE FULL POST AT HYPEBOT:

http://www.hypebot.com/hypebot/2015/05/five-reasons-the-major-labels-didnt-blow-it-with-napster.html

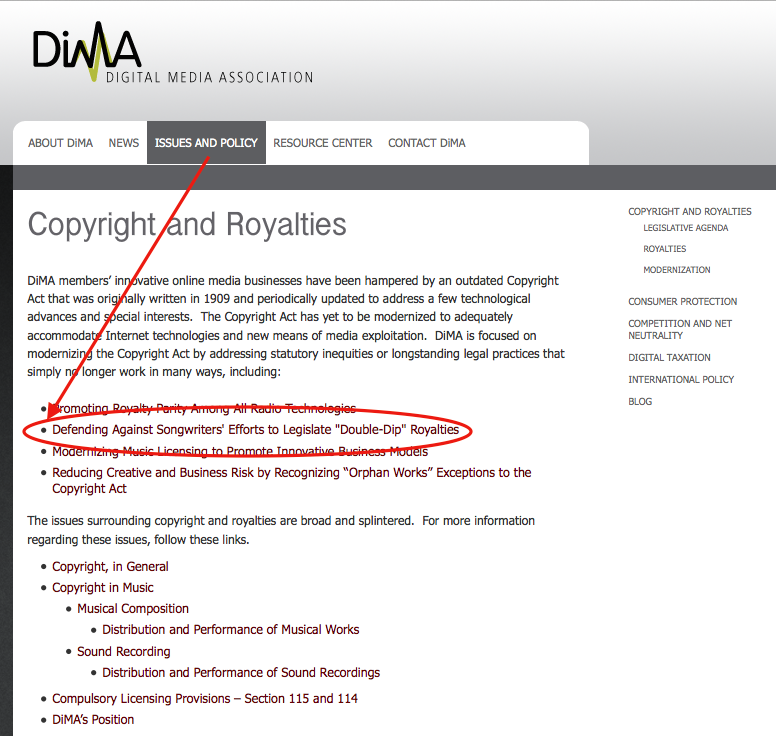

Who is DiMA? Glad you asked, the Digital Media Association. Why do we care? Well, because they are actively working against artists rights. How do we know? Three words… “Defending Against Songwriters”. Yes, DiMA is dedicated to “Defending Against Songwriters” because, you know songwriters are a force that businesses need to defend themselves against.

Wow, really? Seriously? Ok, check it out…

But lets take a look below where current DiMA policy positions are directly in opposition to artists and songwriters rights.

DiMA supports Pandora buying a terrestrial radio station in an effort to lower the royalties Pandora will pay to songwriters.

DiMA is opposed to the Fair Play, Fair Pay Act that would pay performers a terrestrial radio broadcast royalty.

DiMA is opposed to The Songwriter Equity act that would allow songwriters the ability to negotiate fair market rates for their work.

Who would work with DiMA that wasn’t forced to via statutory rates and rate courts?

Please read John Degen’s 5 Seriously Dumb Myths About Copyright the Media Should Stop Repeating at the link below.

There you have it. I hope this quick list has helped my friends and colleagues in the media who may be hurrying to file a story on World Book and Copyright Day. Here’s a final, simple, rule of thumb for writing about copyright.

If you want to understand how a working artist feels about copyright, talk to an actual working artist.

The last time I checked, ivory-tower legal-theory departments and digital-utopian advocacy groups were not the best places to look for actual working artists.

READ THE FULL POST AT MEDIUM:

https://medium.com/@jkdegen/5-seriously-dumb-myths-about-copyright-the-media-should-stop-repeating-a92e934f12a4

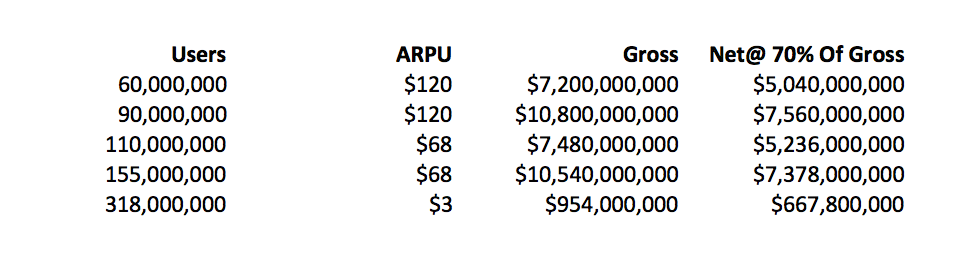

ARPU. Do you know what that is? It’s Average Revenue Per User. Not withstanding the insulting connotation of referring to fans as “users” this is just bad on a number of different levels.

Leaked Sony emails suggest that digital music executives confuse per-capita with ARPU. One of the items we’ve found cruising wikileaks has digital music execs explaining the digital landscape ARPU as follows:

$120 Streaming Subscription

$68 Downloads

$3 Ad-Supported Streaming

We’ll get into the fallacy of the $68 Downloads vs the $120 Streaming Subscriptions in a minute. But first, let’s just look at the fact the industry digital execs actually clocked ad-supported ARPU at $3 per user per year and did it anyway! Seriously? Really? Who thinks going from $68 to $3 is a good idea and then doubles down on trying to get sell in on it? Wow, just wow.

Ok, now back the $68 Downloads ARPU. The question that never seems to be qualified in these ARPU valuations is how many users exactly contribute to the revenue pool to end at up an average of $68 per user? The next question would be how many of those “average” users are paying significantly more than $68? Hell, how many are paying significantly more than $120 per year?

In a basic 80/20 model we would expect that 80% of the revenue would come from 20% of the consumers (er, um… “users”). This means the most valued “users” are now being artificially flattened DOWN to $120 per year.

Streaming Subscription fees as a representative of ARPU doesn’t work, because there are only TWO numbers that can be worked into the average, $120 and zero. So now you have the problem of trying to raise the causal user up to $120 per year while you’ve flattened down your best costumer (er, user). This is the crazy rational behind dropping streaming subscriptions down below $120… But wait… wouldn’t that just also artificially flatten the overall market even lower than the $120 ARPU? Yeah… you bet it would.

It’s truly astounding the lack of ability to use calculators and do simple math. We’ve pointed this out again and again. Even at 90 Million Paid Subscribers at $120 per year, that only generates $7.5b in industry revenue. Ninety Million Paying Subscribers. Just keep saying that over and over until it sinks in.

Subscriptions artificially flatten the market and require extremely high (and largely unrealistic) subscriber numbers because the actual number of “users” consuming music is probably at least double 90 million in the USA. That’s where an ARPU of $68 starts to make sense, somewhere around 110-155 million consumers, but most likely even higher. So, here’s the rub – who really believes that Spotify (or all subscriptions streaming services combined) are going to convert 10s of millions of casual consumers/users into $120 per year ARPU’s? They’re not and that’s why this model is screwed.

For streaming to truly mature the industry needs to embrace tier based, value pricing, so that a truly dynamic and flexible ARPU can be restored. The one size fits all Streaming Subscription ARPU is a lie, and the math shows us why.

“Americans are freedom loving people and nothing says ‘freedom’ like getting away with it.”

From Long, Long Time by Guy Forsyth.

How many times have you heard the expression, “DMCA license”? The expression is completely baseless, yet it has come to be used to describe an online company that uses music, movies, television, books and images that are intentionally used without rights and commercially until the company receives a take down notice. The examples given of companies using the “DMCA license”? Most frequently YouTube, Grooveshark and whatever Michael Robertson is doing at the moment.

If you tell these people that there’s no such thing as a “DMCA license” and that the very expression is internally contradictory, the comeback usually is “Why does YouTube get away with it?” And of course the answer is the same answer to why does YouTube claim to be struggling to break even–Google is willing to…

View original post 1,133 more words

Subscription streaming movie service Netflix announced earlier this week that it has reached 62m users around the world – almost exactly the same number as Spotify.

Big difference is, four times as many of Netflix’s customers pay a subscription each month: 60m of them, or 97% of its total consumer base.

READ THE FULL STORY AT MUSIC BUSINESS WORLDWIDE:

There is a narrative that keeps getting repeated by Spotify apologists and propagandists. It goes something like this, “The problem is not that Spotify pays too little to artists it’s that record labels are not paying the artists their fair share of royalties from Spotify.” Ha! When the gross payable is half a cent or less we think this has a lot more to do with Spotify than labels.

But this idea that labels are the problem pretty much means that Spotify ignores or otherwise feels that any artist not signed to a major label is unimportant in this conversation and that’s too bad.

We don’t know how many artists and small DIY indie labels aggregate to Spotify via Tunecore and CDBaby for example but we suspect it’s literally THOUSANDS of artists that are not signed to major labels (or ANY label). These are artists who are collecting either 100% of their Spotify royalties directly (Tunecore) or collecting those royalties after a 9% dist fee (CDBaby).

When Spotify shifts the blame for low royalties they are ignoring and invalidating all of the artists not signed to major labels, or any label. There are no industry middlemen taking Zoe Keating’s royalties from Spotify. The per stream rate is just incredibly, horribly bad.

There are high profile artists such as Zoe Keating and others who echo the sentiments of artists across all strata’s of the business. The economics of Spotify are just unsustainable from the top down at present rates.

Everyone knows that record labels advance massive amounts of money to develop the careers of those artists signed. These advances are recouped from monies earned in royalties. One can argue about the recoupment mechanics but it doesn’t change the fact that with so little money being generated by Spotify the problem is much greater then the labels.

It’s also interesting that in all the talk of democratization and empowering musicians how little of it appears to be actually happening.

99.9% of Tunecore Artists Make Less Than Minimum Wage…

If the Internet is working for Musicians, Why aren’t more Musicians Working Professionally?

We’ve detailed numerous times how at the top end of the food chain, the Spotify math just doesn’t work and would require more subscribers paying $9.99 a month then any other mature premium subscriber business has achieved to date.

Here’s some context for the chart above. Netflix only has 36m subscribers in the US, no free tier, and massive limitations on available titles of both catalog and new releases. Sirius XM, 26.3m in the US as a non-interactive curated service installed in homes, cars and accessible online. Premium Cable has 56m subscribers in the US paying much more than $10 a month and also with many limitations. Spotify… 3m paid subscribers in the US after four years. Tell us again about this strategy of “waiting for scale.” Three Million Paid… Three…

* 3m Spotify Subs Screen Shot

* 26.3m Sirius XM Subs Screen Shot

* 36m Netflix Subs Screen Shot

* 56m Premium Cable Subs Screen Shot

* $7b Music Business Screen Shot

And, just so everyone is clear, we’re not giving the labels a free pass either. But Spotify’s divisive punt to blame the labels for their own bad business model isn’t fair. We’ve reported on the 18% equity stake the labels took as part of their licensing agreements. That’s an 18% equity stake that we’re pretty sure the artists won’t participate in at the time of an IPO or sale (should there be one).

The larger issue in this conversation however is that if Spotify and on demand streaming services can not generate the same or more revenue then transactional sales, then the model is a net negative for artists. This has nothing to do with labels and everything to do with a flawed business model. Removing the free Ad-Supported tier after a limited time is probably the first, best and most obvious immediate solution but not the only one that should be addressed.

Spotify can not hide behind their bad math by shifting blame to labels when so many artists are getting their royalties from Spotify directly without labels.

FOLLOW THE MONEY.

What do you pay for when you pay for a subscription to an ad supported service like Spotify or Pandora? It stops being ad supported. So who benefits from that? Fans and artists who hate advertising. Artists who get a higher royalty rate.

Who doesn’t benefit?

Well, who do ya think? Here’s a risk factor from Pandora’s SEC filing that gives you a hint:

We rely upon an agreement with DoubleClick, which is owned by Google, for delivering and monitoring our ads. Failure to renew the agreement on favorable terms, or termination of the agreement, could adversely affect our business.

We use DoubleClick’s ad-serving platform to deliver and monitor ads for our service. There can be no assurance that our agreement with DoubleClick, which is owned by Google, will be extended or renewed upon expiration, that we will be able to extend or renew our agreement with DoubleClick on terms…

View original post 587 more words

You must be logged in to post a comment.