Series 3 of The Artist Rights Watch Podcast is here! Nik, David, and Chris are joined by attorney Kevin Casini to talk about the latest with the Copyright Royalty Board and mechanical rates in the Phonorecords IV proceeding and discuss alternatives so songwriters are better represented at the CRB compared to the status quo.

ARW Podcast S3E1: Unfreezing Mechanicals show notes

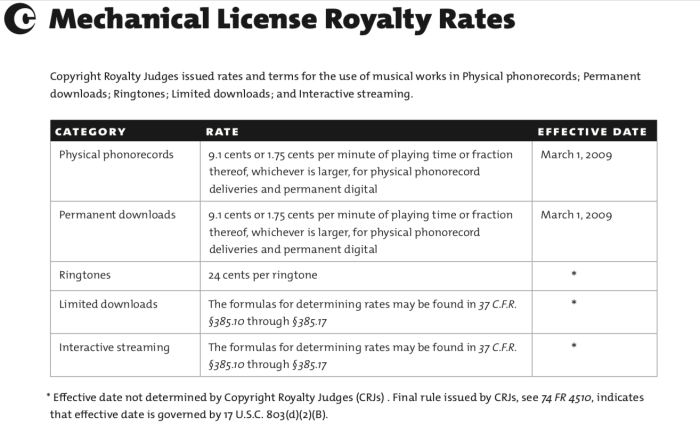

On the this episode of the Artist Rights Watch, Nik, David, and Chris sit down to talk about the recent developments with the CRB and mechanicals with lawyer and advocate, Kevin Casini. The Copyright Royalty Board who herein will more than likely be referred to as the CRB, ‘is a US system of three copyright reality judges who determines rates and terms for copyright statutory licenses and make determinations on distribution of statutory license royalties collected by the US Copyright Office.’ The US mechanical royalties are determined by the CRB and they meet every 5 years to determine the rate. Songwriter groups argued for a higher rate, and the CRB agreed. On March 29, 2022 the CRB agreed to unfreeze the $0.091 mechanical royalty rate which would commence a fight for a new rate in the 2023-2027 period. Over the past few years, there has been numerous criticisms about the constant rule for freezing the mechanical royalty rate. The royalty rate currently is $0.091 which was set back in 2006, and frankly, songwriters are making less money due to economic inflation.

As MTP readers will recall, the National Music Publishers Association and the Nashville Songwriters Association International purported to agree on behalf of a “consensus” that never seemed to materialize to extend the long-frozen 9.1¢ mechanical rate for physical and downloads in the form of a settlement agreement in the Copyright Royalty Board’s Phonorecords IV proceeding. I thought this deal reeked and so did a number of other people, including the Copyright Royalty Board itself which rejected the settlement.

To their great credit, Sony, Universal and Warner stepped up and agreed to offer all the world’s songwriters increased rates of 12¢ plus inflation indexing for the next five years which they didn’t have to do (and was a deal that the CRB hinted that they would find acceptable when they resoundingly rejected the first settlement). Assuming the Copyright Royalty Board accepts the deal—a step you might miss out from the press coverage–this had the effect of a quick end to a process the labels had every right to litigate at the CRB.

The other benefit to the settlement is that it should—if it doesn’t get screwed up again—it should take away a major argument that the digital retailers are using against songwriters in the streaming part of the Phonorecords IV proceeding. That argument is the most obvious negotiating tactic in the world: What’s good for the goose is good for the gander. The services are essentially saying that if the rates should be frozen when the labels are paying the mechanical (which they are on physical and downloads), then the rates should be frozen when the services are paying the mechanical (which the services are on streaming). And no inflation adjustment. Well, no kidding.

In one power move, the labels did something fair for songwriters and incidentally also helped publishers in spite of themselves by taking away a major argument from the digital retailers. Rather than play a schoolyard game of high/low bargaining and stretching out the process for another couple years, the labels cut to the chase and closed. Hopefully the CRB will agree (again, don’t forget that the CRB still has to approve the proposed deal.)

Do we still have bones to pick with the labels? Absolutely. Could the rate have been even more fair? Sure. Might it have been if the publishers had actually done their job and negotiated in the first place? Maybe. Probably. But they didn’t so we’ll never know. However, credit where credit’s due, the labels pulled this one out and saved the publishers’ bacon in spite of themselves.

I do have to note in passing that when you read the press coverage on the filing of the settlement, there’s not one US group with a press release today that actually picked up a pen and filed a comment at the CRB when they were needed and duty called. The awesome UK songwriter group Ivors Academy stepped up and bled with songwriters like Rosanne Cash, George Johnson, Helienne Lindvall, David Lowery and Blake Morgan and all the other commenters who took one for the team when it was unpopular to do so. And as that guy said, he who sheds his blood with me shall be my brother.

You’ll hear a lot of hoorah about how streaming is what’s important from people who are trying to CYA today. Here’s a hot tip: IT’S ALL IMPORTANT IF IT’S YOUR MONEY. Why is that so hard to understand?

Which is why going forward all songwriters and all publishers need to be involved with the rate-setting proceedings at CRB including on streaming. The CRB knows this and acknowledges. I think the labels know this on their side.

The question is whether the publishers do. The announcement of this settlement proposal is both inauspicious and true to form. Remember—they had practically nothing to do with making the deal they celebrate today. But don’t let that stop anyone.

We need fairness at the Copyright Royalty Board. Notice I’m not using the word “transparency” which means whatever the speaker wants it to mean. I’m very specifically talking about a seat at the table not just for songwriters, but for independent labels and publishers as well as the majors. As Ann Richards used to say, if you’re not at the table you are on the menu, and this was a very, very close run thing in Phonorecords IV.

If it weren’t for all the people who commented negatively and resisted the rates that had been bootstrapped in the past and would have been again, I don’t know where songwriters would be today. You gave the Judges the truth, straight from the heart and they responded. So thank you, all of you. And thank you to the readers of MTP and The Trichordist who raised hell right along side. It’s a good day for everyone.

Remember–keep coming back because it works if you work it.

Nice post by Ed Christman in Billboard explaining the continuing crisis on frozen mechanicals. Ed comes up with a rough justice quantification of the impact on songwriter and music publisher revenues in light of controlled compositions clauses in recording contracts that apply to (a) songs written and recorded by artists, or (b) songs by “outside writers” if and only if the artist can get the outside writer to accept the controlled compositions terms and rates.

For those reading along at home, one theory (aside from sheer leverage) that gets used in this context is that the artist/writer can agree on behalf of all co-writers to accept the terms of the license granted by the artist to the label in the controlled compositions clause because they are co-owners of an undivided interest in the song copyright and can grant nonexclusive licenses in the whole subject to a duty to account provided the license is not economic waste or self-dealing. Let’s just leave all that where it lays for now, but that story has never really been properly challenged–particularly the economic waste part given the rate fixing date issue and even the frozen mechanicals crisis itself. We’ll come back to that bit some other time.

The rate fixing date is a key part of the discussion for understanding the impact of unfreezing mechanicals. So what is that rate fixing provision?

Remember, the controlled compositions clause starts with reducing the minimum statutory mechanical rate in the US (and in theory in Canada subject to MLA) in effect at a point in time. That point in time is either commencement of recording (booo!), delivery, release or sale of a unit embodying the song at issue. Remember that the labels only pay mechanical royalties on physical and downloads (the rates at issue in the frozen mechanicals crisis)–streaming services pay for the interactive streaming mechanicals (and there is no mechanical for webcasting, a whole other beef).

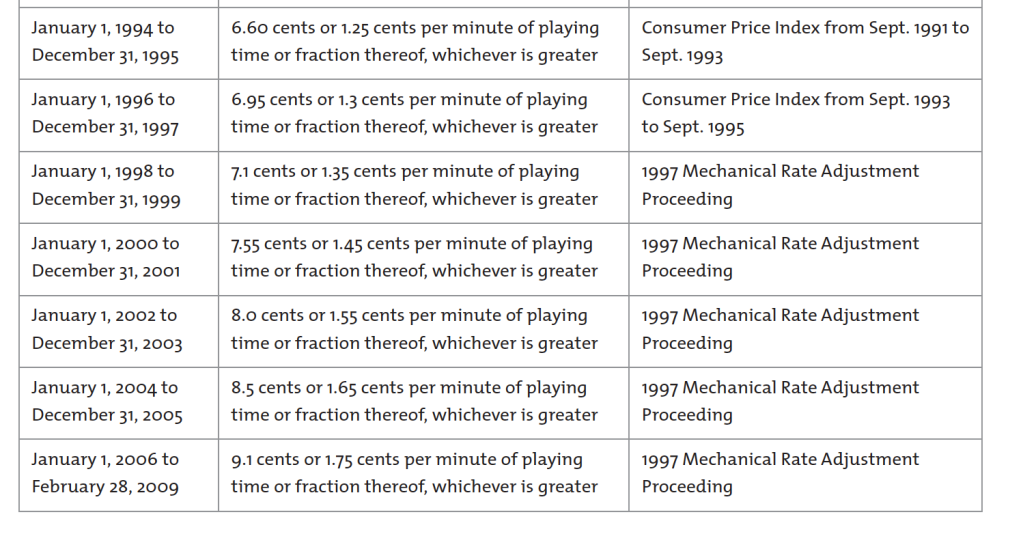

You say, wait–isn’t the mechanical rate 9.1¢? Why does it matter when the record was recorded, delivered, released or sold? Won’t the rates all be the same? And you’d be right if you were asking about a record recorded and released in 2006 or after, or a record recorded and released between 1909 and 1978, like, say some titles by Bob Dylan, The Beatles, Otis Redding or Miles Davis.

But–it wasn’t always this way. The mechanical royalty rate was set at 2¢ by Congress with the first statutory license, i.e., compulsory license, in 1909 and did not change until the 1976 revision of the US Copyright Act effective 1978. The rate then began to incrementally increase over the years until it reached 9.1¢ in 2006, a phased increase that was to compensate for Congress failing to increase the rate for 70 years, aka “the Ice Age”. The Congress really screwed up songwriters’ lives by freezing the rate at 2¢ during the Ice Age and songwriters and their heirs have been paying for it ever since, right up to the 2006-2022 period, aka “the Second Ice Age” or the Return of the Neanderthals.

In an effort to help songwriters shovel out from the Ice Age, The Congress also authorized indexing the minimum rate to inflation from 1988 to 1995. Indexing is again on the mind of the Copyright Royalty Board right now–bearing in mind that an increase in rates due to inflation has nothing to do with the intrinsic value of the song copyrights so there’s no confusion. Indexing simply applies any increase in the consumer price index to the statutory rate and preserves buying power. In a way, it is the opposite of a case about value. Indexing assumes that the value issue was already decided (in this case in 2006) and simply preserves buying power so that the “nominal” rate of 9.1¢ in 2006 can still buy the same amount of goods or services in 2022 (or 2023 in the case of the CRB rate period). Otherwise the “real” rate, i.e., the inflation adjusted rate, is not 9.1¢ it is about 6¢.

Remember–the proposed rate increase to 12¢ by the CRB is not about value, it’s about buying power because it’s solely focused on inflation.

So back to controlled compositions. It is no coincidence that at the same time as the 1978 increases were phased in, the labels established controlled compositions clauses that knocked songwriters back down. They would probably not have gotten away with freezing by contract at 2¢ so they let the rate float up but much more slowly and with several caps. The first cap is the maximum number of songs, usually 10 or 11. The next cap is the infamous 3/4 rate, where the label pays based on 75% of the minimum statutory rate. But the third cap is the rate fixing date and that’s the one we want to focus on in the unfrozen mechanicals context.

In simple form, it looks something like this contract language:

If the copyright law of the United States provides for a minimum compulsory rate: The rate equal to seventy-five percent (75%) of the minimum compulsory license rate applicable to the use of musical compositions on audio Records under the United States copyright law (hereinafter referred to as the “U.S. Minimum Statutory Rate”) at the time of the commencement of the recording of the Master concerned but in no event later than the last date for timely Delivery of such Master (the applicable date is hereinafter referred to as the “Copyright Fixing Date”). (The U.S. Minimum Statutory Rate is $.091 per Composition as of January 1, 2006);

The way that the statutory rate increases come into the controlled compositions clause is because from 1978-2006 the statutory rates increased across albums delivered across album cycles. If you consider that the rates used to increase about every two years and that an album cycle can be two years, it’s likely that LP 1 would have a lower rate than LP2, LP 2 than LP3 and so on right up to 2006.

Also remember that the increases in rates are prospective, meaning that the controlled compositions rate on recordings delivered in the future will, of course, get the higher rate, even if the past rates don’t change which they don’t, at least not yet. Also consider that permanent downloads often are excluded from controlled comp treatment and are paid at full rate, probably on the rate fixing date in the artist’s agreement. Sometimes the download rates “float” or increase in line with increases in the statutory rate, but that’s part of individual negotiations.

If there is an outside songwriter who does not agree to accept the artist’s controlled composition rate (and there are plenty of these) what happens? Typically the label will account to the outside writer at their full minimum statutory rate but will deduct that payment from the maximum aggregate mechanical royalty payable to the artist (i.e., the 10 song cap). There’s some twists and turns to this involving rates on different units “made and distributed”, but for our purposes there is one clear thing to understand:

Because of the rate fixing date which is frozen by contract (the Mini Ice Age) the artist/songwriter will be paying a higher mechanical to the outside writer from a frozen royalty “pool”.

This is why you should always, always demand “protection” for at least one outside song in your contract and then review each album to determine if that needs to be increased. This is particularly true for records made in places like Nashville where the record company will demand you work with “A” list songwriters (assume none of whom will take 3/4 rate) and then try to deduct the difference between the uncontrolled rate and the controlled rate from you (and if it gets big enough, cross it to your record royalties). (Not only will A list writers not take the 3/4 rate, they’re pissed because they can’t charge you double stat like they do double scale for sessions.)

Example: You have a 10 x 3/4 rate cap on mechanicals, the “cap rate”. That’s the 68.25¢ album rate you hear about (10 x .75 x 9.1¢). Say you have 10 songs on your album and you wrote all of them. You get the entire 68.25¢. If you had two outside songs whose writers get 9.1¢ under current rates, you deduct 18.2¢ from the cap rate, and that leaves 50.05¢ as the “controlled pool” or the total mechanical royalty payable to the artist/songwriter (actually all controlled writers, but leave aside that wrinkle).

So you can see, that’s no longer a 75% rate, it’s actually more like a 55% rate.

Now let’s assume that the new rate is 12¢. Same calculation, two outside songs now get 24¢, but the cap rate stays the same because of the rate fixing date. During the Mini Ice Age, i.e., while that cap rate is fixed at 9.1¢ x 10 x .75, the controlled pool now is expressed as 68.25¢ – 24¢ = 44.25¢, or about 48% (44.25 ÷ 91). The artist’s publisher is not going to be wild about that; the outside writer’s publishers will be thrilled.

This will start to true up on the next LP that takes a rate fixing date after the 12¢ rates go into effect. In that situation you’d be increasing both sides of the equation, so the cap rate would increase to 90¢ (10 x .12 x .75). The outside writers still get 12¢ each for two songs (or 24¢) which is deducted from the cap rate to get a controlled pool of 66¢. The true controlled comp rate is then back to about 55%.

These effects will be less pronounced if you have protection for one or more songs (or fractions of songs) or you have a higher cap, say 11 or 12 instead of 10 (with corresponding increases on other configurations). But you see the trend line.

I think this leads to the conclusion that increasing the statutory rate is a huge step forward and we should all be grateful to the Judges. The rate fixing dates for catalog titles (really the entire rate fixing date concept) must also be considered and any new effort to tweak the controlled compositions clause to effectively nullify the Judges’ rate increase will no doubt cause further conflict.

One day Congress will again act to reduce the effects of the controlled compositions clause and especially the rate fixing date, but in the meantime the Judges may well visit the issue to the extent they are able before we see the Return of the Neanderthals.

There are some decades in which nothing happens and some weeks in which decades happen. This was one of those weeks. You no doubt have seen that the Copyright Royalty Judges offered a breath of fresh air in the contentious and labyrinthine Phonorecords III and IV proceedings by refusing to accept the insider “settlement”…but if mechanical royalties have been understated, what does it mean for catalog valuations in the past and in the future? Looking at you, Bob Dylan!

We’ve all heard the talking points from Big Radio’s shillery the National Association of Broadcasters about how it’s perfectly fine for American radio stations to deny recording artists and session musicians fair compensation–because exposure, don’t you know. Big radio delivers huge audiences for music and we should all be grateful and work for free for the ever-more-consolidated broadcasting industry.

The other talking point we don’t hear so much from these characters is that media ownership rules are bad and that greater and greater concentration of influence and wealth to control the public airwaves is good. That’s right, it’s not the corporate airwaves, it’s the public’s airwaves. But you wouldn’t know that by looking, right?

So the latest version of this “bigger is better” guff is happening right now at the Federal Communications Commission that licenses radio stations. The NAB is poormouthing to the FCC about how radio and TV stations have trouble competing with Google and Facebook (in particular) for advertising. Oh, no. Google is grinding them into bits? Say it ain’t so!

We know a little bit about what it’s like to have soulless Silicon Valley oligarchs using their political and financial muscle to get a free pass to jack with your livelihood without repercussions from the guys with badges. If Big Tech is really the problem for Big Radio, I’m sure there would be some support for going after them together. But playing nice with others would require the soulless media oligarchs to stop acting like wankers and make a fair deal for artists and musicians. That is not happening. No, no, the solution to the broadcasters’ Google problem is to relax media ownership rules for even MORE concentrated radio ownership, you see. Plus these monopolists want an antitrust exemption for which they have presented no evidence other than even more shillery.

But see what they did there? MusicFirst certainly did and wrote to the FCC to make sure the FCC did, too (letter is here):

The National Association of Broadcasters, in seeking relaxed broadcast radio ownership rules, is asking the FCC to accept arguments directly contrary to those it makes in opposing the American Music Fairness Act.

In fighting the AMFA, the NAB continues to claim airplay has “promotional value” that eliminates the need for radio broadcasters to pay recording artists for the music the stations use to derive millions of advertising dollars. The promotion argument has never been a valid justification for refusing to pay musicians. Such a rationale could swallow all of copyright, as any use of content can be called “promotional.” But even the NAB’s own arguments before the FCC are showing the flaws with its promotion claim.

For example, the NAB argues in this proceeding that radio broadcasters need increased economies of scale to compensate for the significant audience share broadcast radio has lost. Yet, if radio broadcasters have lost so much audience share that they need government intervention, the promotional value they claim to provide recording artists cannot be adequate compensation.

The NAB also applies the promotion claim inconsistently. In addition to its argument about loss of broadcast radio audience, the NAB alleges here that broadcasters need increased economies of scale because online platforms refuse to fairly compensate broadcasters for content the platforms use to derive advertising revenue. The NAB is similarly arguing that platforms’ inadequate compensation warrants passage of the Journalism Competition and Preservation Act [the antitrust exemption for monopolists].

The musicFIRST Coalition agrees with the NAB that distributors should adequately compensate content providers. But what is good for the goose must be good for the gander. Online distribution of broadcaster content can also be claimed to be promotional. If the NAB finds inadequate the combination of online promotion and the money online platforms do pay broadcasters, the alleged value of broadcast radio promotion combined with the lack of any money the radio broadcasters pay recording artists cannot possibly be adequate.

The shills at the NAB should try being reasonable just once instead of doing their usual blunt force trauma. Here’s the reality: Nobody is buying what they’re selling because it’s just more snake oil.

If you’ve tried to get a vinyl record pressed in the last few years, one thing is very obvious: There is no capacity in the current manufacturing base to accommodate all the orders–unless your name is Adele or Taylor Swift, of course. If that’s your name, as if by magic you get your vinyl orders filled and shipped on time.

Jack White spotted the vinyl trend early on–in 2009–and is filling the gap through his Third Man pressing operations. But Jack is calling on the major labels to please compete with him–rather unusual–because it’s the right thing to do in order to meet the demand for the benefit of the consumer. And the elephant in the room of this discussion is that we don’t really have any idea what the vinyl sales would be because demand is not being met by supply.

Not even close.

When a major label abandons a configuration, it’s not really abandoned. It gets outsourced to an independent and as long as there is manufacturing capacity in the system, that independent still takes orders and fulfills those orders by using that manufacturing capacity. The titles still appear in the sales book, orders get taken and returns accommodated.

Major labels also hand off vinyl manufacturing to their “special markets” divisions. For example, if you have ever tried to get vinyl manufactured in a limited run for venue sales on a major label artist (or former major label artist) you will get put through the bureaucratic torture gauntlet for the privilege of paying top dollar on a product that the label will have nothing to do with selling.

But even so, at some point that manufacturing capacity begins to shrink because the majors are getting out of the configuration and they will eventually get out of the manufacturing business altogether. And that creates a great sucking sound as capacity tanks.

I raised this problem in comments to the Copyright Royalty Board about the frozen mechanicals debacle where the smart people have tried to extend the 2006 songwriter rates on vinyl and CDs without regard to rampant inflation and simply the value of songs to sell millions of units. Why? Because vinyl and CDs don’t matter according to the lobbyists. This is, of course, bunk.

The fact is–and Jack White’s plea illuminates the issue–we don’t know what the sales would be if the capacity increased to meet demand. But we do know that sales would be higher. Probably much higher.

You do see entrepreneurs entering the space using new technology. Gold Rush Vinyl in Austin is a prime example of that phenomenon. The majors need to reconsider how to meet demand and keep the consumer happy. They also need to clean up the sales and distribution channel so that it’s easy for record stores to actually get stock, which, frankly is a joke.

Why anyone wants to substitute away from high margin physical goods to low margin streaming goods with a “rich get richer” financial model is a head scratcher. Although maybe I answered my own question.

But–as Trichordist readers will recall, the major publishers and major labels as well as the Nashville Songwriters Association are trying to convince the Copyright Royalty Board that vinyl and CDs are not important and that songwriters should have their mechanical royalty rates frozen again. You do have to ask if Jack White is even aware that the major publishers and major labels are trying to get the Copyright Royalty Board to extend the 2006 freeze on mechanicals for the resurgent vinyl configuration for another five years.

Vinyl and CDs still account for about 15% of revenue on an industry wide basis–I’ll believe that it’s not significant when Lucian Grange says he doesn’t need 15% of billing. Yeah, that will happen.

The only reason that mechanicals for those configurations aren’t higher is because they have been artificially suppressed by the participants at the Copyright Royalty Board telling the judges that the revenue is low so please freeze the rates again. Kind of circular, yes? The current 2006 rate of 9.1¢ would be adjusted to 13¢ in current dollars just taking into account inflation and ignoring the value of the songs to create a nearly vertical chart like this:

Spotify has one big governance problem that permeates its governance like a putrid miasma in the abattoir: “Dual-class stock” sometimes referred to as “supervoting” stock. If you’ve never heard the term, buckle up. I wrote an extensive post on this subject for the New York Daily News that you may find interesting.

Dual class stock allows the holders of those shares–invariably the founders of the public company when it was a private company–to control all votes and control all board seats. Frequently this is accomplished by giving the founders a special class of stock that provides 10 votes for every share or something along those lines. The intention is to give the founders dead hand control over their startup in a kind of corporate reproductive right so that no one can interfere with their vision as envoys of innovation sent by the Gods of the Transhuman Singularity. You know, because technology.

Google was one of the first Silicon Valley startups to adopt this capitalization structure and it is consistent with the Silicon Valley venture capital investor belief in infitilism and the Peter Pan syndrome so that the little children may guide us. The problem is that supervoting stock is forever, well after the founders are bald and porky despite their at-home beach volleyball courts and warmed bidets.

Spotify, Facebook and Google each have a problem with “dual class” stock capitalizations. Because regulators allow these companies to operate with this structure favoring insiders, the already concentrated streaming music industry is largely controlled by Daniel Ek, Sergey Brin, Larry Page and Mark Zuckerberg. (While Amazon and Apple lack the dual class stock structure, Jeff Bezos has an outsized influence over both streaming and physical carriers. Apple’s influence is far more muted given their refusal to implement payola-driven algorithmic enterprise playlist placement for selection and rotation of music and their concentration on music playback hardware.)

The voting power of Ek, Brin, Page and Zuckerberg in their respective companies makes shareholder votes candidates for the least suspenseful events in commercial history. However, based on market share, Spotify essentially controls the music streaming business. Let’s consider some of the implications for competition of this disfavored capitalization technique.

Commissioner Robert Jackson, formerly of the U.S. Securities and Exchange Commission, summed up the problem:

“[D]ual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms [Snap, Inc. and Google Class B shares] have recently issued shares that give ordinary public investors no vote at all.

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression. But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.” Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.

Spotify is the dominant streaming firm and the voting power of Spotify stockholders is concentrated in two men: Daniel Ek and Martin Lorentzon. Transitively, those two men literally control the music streaming sector through their voting shares, are extending their horizontal reach into the rapidly consolidating podcasting business and aspire soon to enter the audiobooks vertical. Where do they get the money is a question on every artists lips after hearing the Spotify poormouthing and seeing their royalty statements.

The effects of that control may be subtle; for example, Spotify engages in multi-billion dollar stock buybacks and debt offerings, but has yet makes ever more spectacular losses while refusing to exercise pricing power.

So yes, Spotify is starting to look like the kind of Potemkin Village that investment bankers love because they see oodles of the one thing that matters: Fees.

On the political side, let’s see what the company’s campaign contributions tell us:

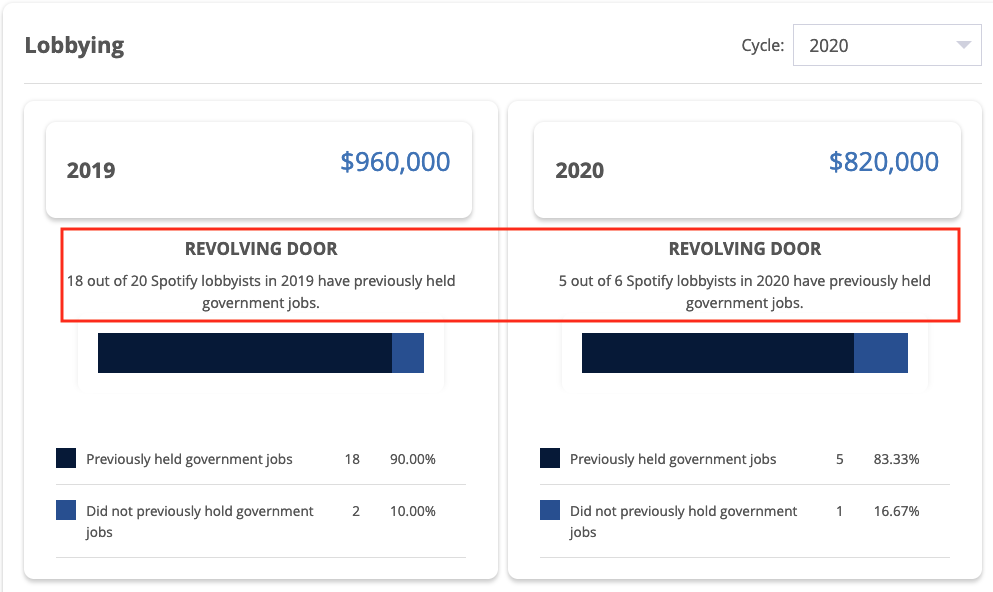

Spotify has also made a habit out of hiring away government regulators like Regan Smith, the former General Counsel and Associate Register of the US Copyright Office who joined Spotify as head of US public policy (a euphemism for bag person) after drafting all of the regulations for the Mechanical Licensing Collective;

Whether this is enough to trip Spotify up on the abuse of political contributions I don’t know, but the revolving door part certainly does call into question Spotify’s ethics.

It does seem that these are the kinds of facts that should be taken into account when determining Spotify’s ESG score. At this point, it looks like Spotify is an ESG fail–which may require divesting by some of the over 600 mutual funds that hold shares.

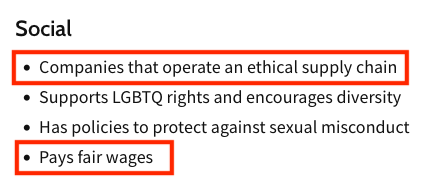

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective scam and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor? I think not.

[This is the first in a series of three short posts examining how Spotify scores as an Environmental, Social and Governance (or “ESG”) investment. “ESG” is a Wall Street acronym often attributed to Larry Fink at Blackrock that designates a company as suitable for socially conscious investing based on its “Environmental, Social and Governance” business practices, that is “ESG”. See the Upright Net Impact data model on Spotify’s sustainability score. As of this writing, the last update of Spotify’s Net Impact score was before the Neil Young scandal and, of course, rocketing energy prices that compound the environmental impact of streaming. These posts first appeared on MusicTechSolutions]

Spotify closes $24 higher than its first day of trading after destroying the incomes of thousands of artists and even more songwriters. pic.twitter.com/HeHXnEXVHh

Spotify has an ESG problem, and a closer look may offer insights into a wider problem in the tech industry as a whole. If a decade of destroying artist and songwriter revenues isn’t enough to get your attention, maybe the Neil Young and Joe Rogan imbroglio will. But a minute’s analysis shows you that Spotify was already an ESG fail well before Neil Young’s ultimatum.

Streaming is an Environmental Fail

I first began posting about streaming as an environmental fail years ago in the YouTube and Google world. Like so many other ways that the BIg Tech PR machine glosses over their dependence on cheap energy right through their supply chain from electric cars to cat videos, YouTube did not want to discuss the company as a climate disaster zone. To hear them tell it, YouTube, and indeed the entire Google megalopolis right down to the Google Street View surveillance team was powered by magic elves running on appropriate golden flywheels with suitable work rules. Or other culturally appropriate spin from Google’s ham handed PR teams.

Mission creepy meets the Sound of Music

Greenpeace first wrote about “dirty data” in 2011–the year Spotify launched in the US. Too bad Spotify ignored the warnings. Harvard Business Review also tells us that 2011 was a demarcation point for environmental issues at Microsoft following that Greenpeace report:

In 2011, Microsoft’s top environmental and sustainability executive, Rob Bernard, asked the company’s risk-assessment team to evaluate the firm’s exposure. It soon concluded that evolving carbon regulations and fluctuating energy costs and availability were significant sources of risk. In response, Microsoft formed a centralized senior energy team to address this newly elevated strategic issue and develop a comprehensive plan to mitigate risk. The team, comprising 14 experts in electricity markets, renewable energy, battery storage, and local generation (or “distributed energy”), was charged by corporate senior leadership with developing and executing the firm’s energy strategy. “Energy has become a C-suite issue,” Bernard says. “The CFO and president are now actively involved in our energy road map.”

If environment is a C-suite issue at Spotify, there’s no real evidence of it in Spotify’s annual report (but then there isn’t at the Mechanical Licensing Collective, either). “Environment” word search reveals that at Spotify, the environment is “economic”, “credit”, and above all “rapidly changing.” Not “dirty”–or “clean” for that matter.

The fact appears to be that Spotify isn’t doing anything special and nobody seems to want to talk about it. But wait, you say–what about the sainted Music Climate Pact? (Increasingly looking like a PR effort worthy of Edward Bernays.) Guess who hasn’t signed up to the MCP? Any streaming service as far as I can tell. There is a “Standard Commitment Letter” that participants are supposed to sign up to but I wasn’t able to read it. Want to guess why?

That’s right. You know who wants to know what you’re up to.

If you haven’t heard much about streaming’s negative effects on the environment, don’t be surprised. It’s not a topic that’s a great conversation starter and very few journalists seem to have any interest in the subject at all. I wonder why.

But if you’re an artist who is concerned about the impact of streaming your music on the environment or an investor trying to see your way through the ESG investment, this should give you a few questions to ask about Spotify’s ESG score. And if that slipped by you, don’t feel bad–Blackrock reportedly holds 3.8 million shares of Spotify that are worth less all the time, so they didn’t catch it either. And Blackrock coined the phrase.

Next: Spotify’s “Social” Fail: Rogan, Royalties and The Uyghurs

If you’ve been pitched to lend your name to an NFT platform or promotion, or if you are an NFT promoter who wants to attract artists to your program, there are some issues that should get addressed. Obviously, discuss all this with your lawyers since this isn’t legal advice, but the following are some issues that you may want to consider before you commit to anything.

As NFTs are priced in cryptocurrencies, a word about that. You should understand that cryptocurrencies use a huge amount of energy due to “mining” (See the Cambridge University bitcoin energy consumption index) and the current spike in the cost of energy is going to have an effect. Also realize that when someone tells you that an crypto enterprise is “green” you have to ask them what they mean exactly–for example, Google tells you that their data centers are “green” because they buy carbon offsets or use hydroelectric power from Oregon or wind farms in Nebraska (just ask Senators Ron Wyden and Ben Sasse), but that doesn’t mean that it doesn’t still take enough electricity to power Cincinnati in order to operate YouTube. There are no magic elves on golden flywheels producing electricity as if by magic. They still plug into the wall like everyone else.

1. What artist rights are being granted and to whom?

2. Does grant of rights match the project summary and are license agreement, smart contract, marketplace/auction TOS and cryptocurrency rules all consistent? Has a subject matter expert been engaged to produce a report stating and certifying that the smart contract code implements the actual deal or needs to be revised?

3. What royalty is paid and to whom and when? Does artist, previous owner or charity participate in resale revenue after initial sale? Are any state or federal relevant tax rules implicated? What have you done to keep NFT revenue as far away from MLC as possible? (Remember that Etherium vehicle Consensys is somehow involved with the MLC.)

4. Are there exploitation or marketing restrictions on the NFT that would prevent the NFT and artist name being used in ways that are offensive to the artist, at least during the artist’s lifetime? Could heirs enforce these rights?

5. Are there any third party payments involved like producer payments, production company overrides, or any third party rights involved, re-recording restrictions. Will any letter of direction be required, e.g., for producers?

6. Are you being asked to clear publishing? If someone is telling you that they have cleared publishing, has the publisher confirmed the license and are individual songwriters actually receiving a share of revenue? The tendency is that the major publishers “settle” these kinds of cases for a lump sum and prospective royalty, which may or may not be received by individual songwriters after multiple commissions being siphoned off the top.

7. When does NFT terminate? (On resale, transfer by owner, term of years)

8. What is the governing law and venue? (And how to enforce)

10. Is artist asked to make representations, warranties and indemnity? Can the artist make such reps and warranties?

11. Is indemnity capped?

12. Are there any active disputes among anyone in the chain on the NFT promoters’ side? (“Disputes” is any disagreements, including, but not limited to, litigation or threatened litigation.) Who will cover artist’s costs of defense?

13. Is there insurance on chain of title, failure to enforce the smart contract, nonpayment, business risk?

14. Can license agreement or smart contract be revised unilaterally?

15. Is the NFT or NFT collection comprised of “generative art” or artwork created by machines, algorithms, artificial intelligence, and related technologies (i.e., potentially not capable of copyright protection)? What are implications for name and likeness rights.

16. What assurances have been given to identify purchasers of NFTs to enforce terms or prosecute breaches for first or subsequent sales?

18. Is NFT or any NFT cash flows implicated in any sanctions placed on persons related to the Russian Federation? Given the strong reaction to Russia’s invasion of Ukraine, consider any implications if China were to invade Taiwan and similar actions were taken against China or China-based companies.

19. Has NFT seller or marketplace obtained legal opinion regarding whether the NFT constitutes a “security” that would require sale by a registered securities broker-dealer or other regulatory oversight?

20. Are any state securities laws, tax laws or regulations, or “doing business” laws implicated or reporting obligations triggered?

Each NFT raises its own questions, so this checklist is just a starting point.

You must be logged in to post a comment.