— MusicTechPolicy.com (@MusicTechPolicy) May 13, 2025

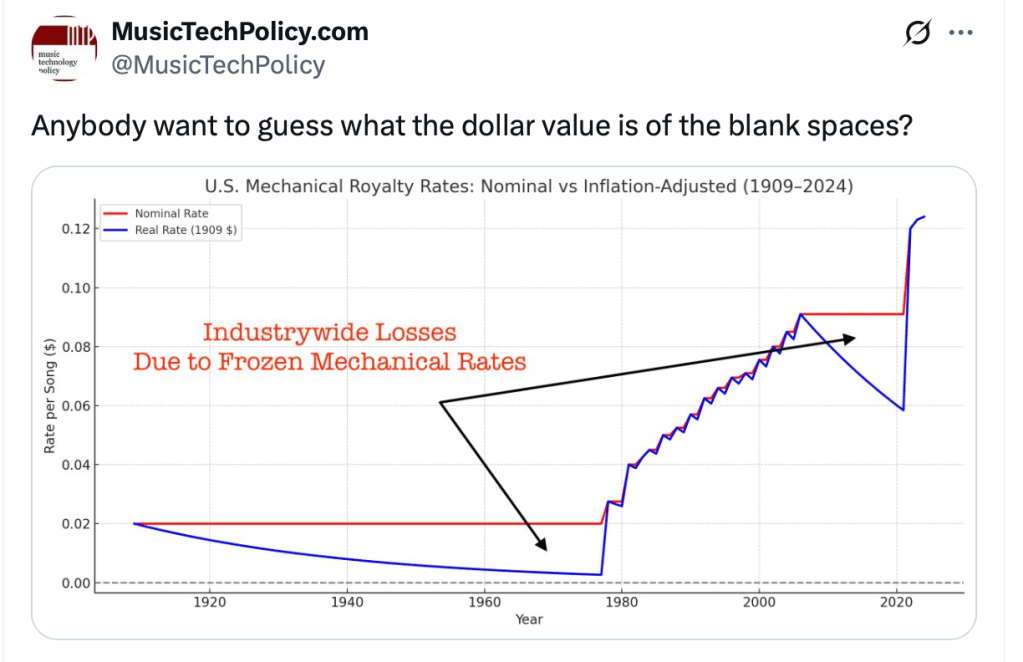

The red line is the actual mechanical rate in pennies (nominal rate) compared to the blue line which is the inflation-adjusted rate (real rate). Notice that during periods without a COLA adjustment like we won for physical and CDs in CRB 4 (aka Phonorecords IV), the blue line is less than the red line.

An important feature of this graph is that the blue line continues the downward slope until it is saved by an increase in rates followed by a cost of living adjustment or stair step increases (some of which were due to a COLA).

As soon as the COLA comes off, the downward slope returns, meaning the buying power of the statutory rate declines. This is to be expected due to inflation–the downward slope will be more pronounced in times of high inflation.

Notice that this places a blank space on the area of the graph between the red and blue lines. That blank space represents lost revenue due to a fixed rate that is not adjusted for inflation. It is theoretically and industrywide loss of revenue.

It would be possible for songwriters to make the same calculation for streaming if the Copyright Office were required to publish the results of the CRB’s streaming mechanical calculation. This would be much easier because there has never been a COLA for streaming mechanicals, although there clearly ought to be.

One place to start making that case might be to calculate the industrywide loss from the failure to adjust for inflation in the rates the government forces us to take.

In a landmark development for recording artists, the Copyright Royalty Board (CRB) has proposed new royalty rates under the “Web VI” proceeding, covering the period 2026 through 2030. These rates govern how much commercial broadcasters must pay for streaming sound recordings under the statutory licenses set forth in Sections 112 and 114 of the U.S. Copyright Act.

The new rates reflect the culmination of years of advocacy by SoundExchange and artist-rights groups and represent another meaningful upward adjustments in royalty rates. The Copyright Royalty Judges have adopted a meaningful schedule of increases—both in per-stream royalties and in the minimum annual fees webcasters must pay—designed to better align statutory streaming compensation with market realities. (Unlike streaming mechanical rates, webcasting royalties are a penny rate per play.)

A Clear Victory in Numbers

Year

Web V Per-Performance Rate

Web VI Per-Performance Rate

% Increase Over Web V

Web V Min. Annual Fee

Web VI Min. Annual Fee / % Increase

2026

$0.0021

$0.0028

+33.33%

$1,000

$1,100 / +10.00%

2027

$0.0021

$0.0029

+38.10%

$1,000

$1,150 / +15.00%

2028

$0.0021

$0.0030

+42.86%

$1,000

$1,200 / +20.00%

2029

$0.0021

$0.0031

+47.62%

$1,000

$1,250 / +25.00%

2030

$0.0021

$0.0032

+52.38%

$1,000

$1,250 / +25.00%

These increases aren’t merely arithmetic; they represent a philosophical shift in how creators are valued in the digital economy.

Structural Adjustments

Beyond the rate hikes, the CRB has adopted operational changes proposed by SoundExchange to royalty reporting and distribution. For example:

– The late fee for audit-based underpayments is reduced from 1.5% to 1.0% per month, capped at 75% of the total underpayment. – Starting in 2027, webcasters using third-party vendors must obtain transmission and usage data or contractually guarantee its delivery. – If a commercial broadcaster fails to file a report of use, SoundExchange may now distribute royalties based on proxy data.

These tweaks aim to close loopholes and increase reliability in royalty tracking—critical steps toward a more transparent system.

The Road Ahead

While the Web VI proposal rule will be final after June 16, 2025, it is already being hailed as a pivotal win by artist advocates. For too long, streaming-era economics have undervalued creators in favor of platforms and intermediaries.

This ruling is a recognition—long overdue and hard-won. When finalized, the Web VI clear and easy to understand rates and terms will not only ensure a greater financial contribution for featured and nonfeatured recording artists and rights holders, but also reassert the foundational principle that creators should be paid fairly when their work fuels billion-dollar platforms.

For artists and musicians navigating a shifting industry, the law is catching up with the market it governs on the side of the creators who drive the business.

Of course, don’t forget that some of these same broadcasters who pay under the statutory license for streaming do not pay anything to artists for over the air broadcast of terrestrial radio for the exact same plays of the exact same records–another reason that Congress must finally pass the American Music Fairness Act. That’s why we support the #IRespectMusic campaign and the MusicFirst Coalition. Ask Congress to support musicians here.

As you probably already know, the statutory mechanical royalty rate for physical or downloads (not streaming) has increased as of January 1, 2025. This means that all floating rate licenses (e.g., not subject to controlled comp rates) should have increased as of January 1, 2025 from 12.4¢ to 12.7¢ due to the Phonorecords IV cost of living adjustment. (And of course should have increased in prior PR IV years in 24.). And of course we have Trichordist readers to thank for helping to persuade the Copyright Royalty Judges to reject the Phonorecords IV frozen mechanical rate settlement that led to the labels agreeing to an increase from 9.1¢ to 12¢ plus a cost of living adjustment on physical and downloads that rose to 12.4¢ in 2024 and now to 12.7¢ in 2025. (But remember there is no cost of living adjustment for streaming mechanicals like Spotify.)

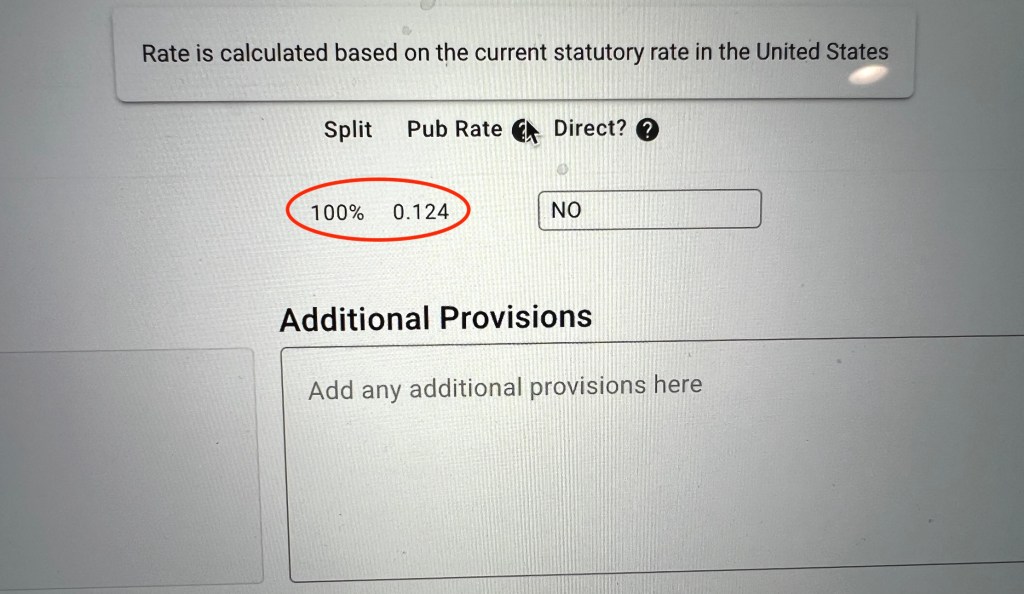

It’s probably just a glitch, but I understand that HFA hasn’t updated the 1/1/25 rates yet for “licensing out” in at least one instance (see screen capture below obtained this week). I’m inclined to believe that the issue is with the database and would not be a one-off, but I could be wrong. That suggests to me that every songwriter and publisher with either a newly issued license since 1/1/25 or a floating rate license in place during PR IV rate period (2023-2027) should probably confirm that the respective COLA escalations have been properly applied as of January 1 of 2024 and 2025. I would imagine that this isn’t an isolated incident, but maybe it is. No reason to let grass grow, however.

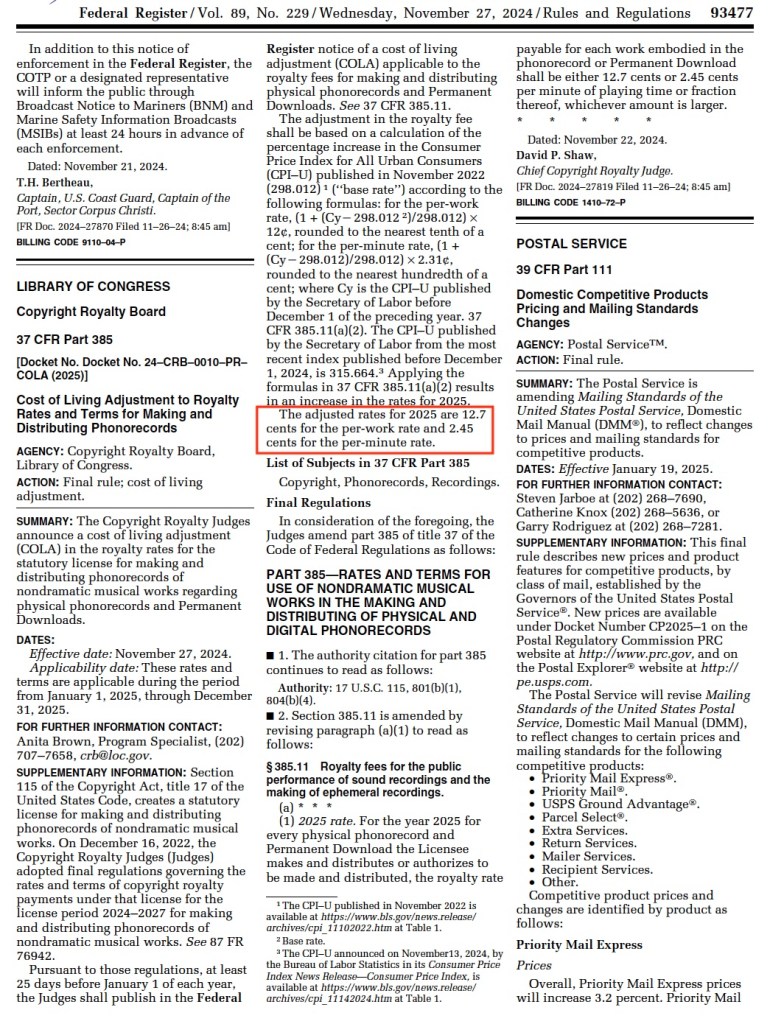

Here’s the Copyright Royalty Board’s timely notice of the new rate effective 1/1/25–which means that the HFA system does not appear to have been updated unless the screen capture reflects a one-off which seems doubtful to me.

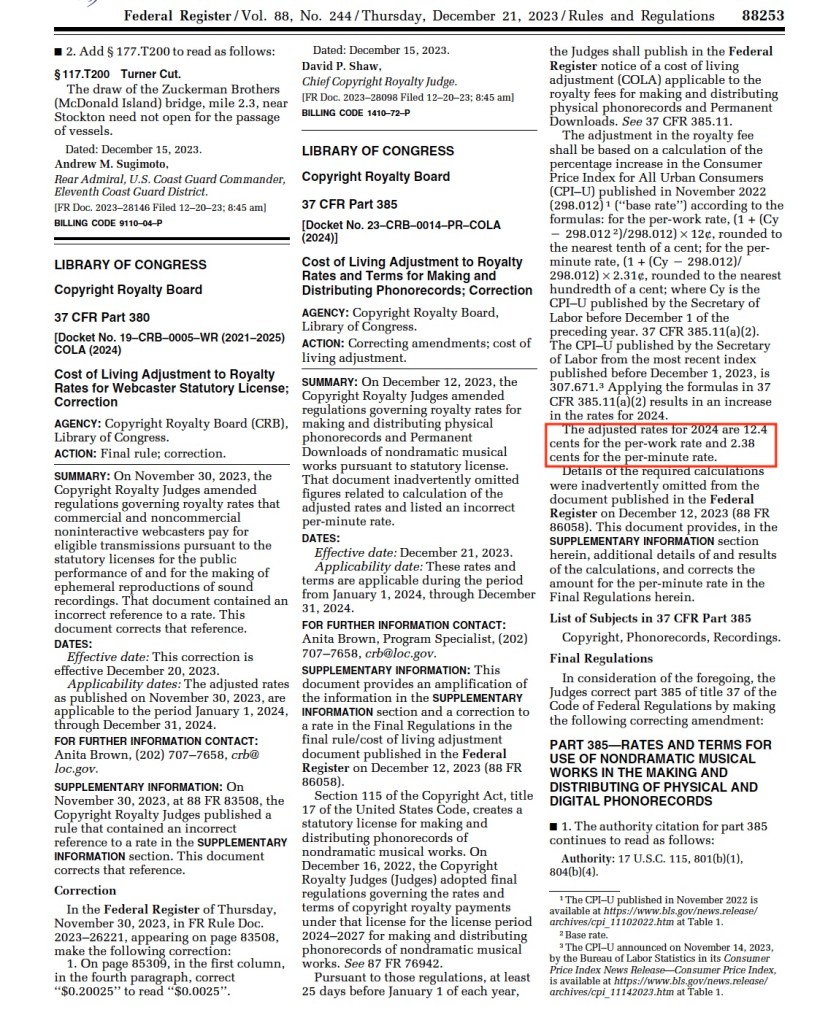

And for reference, this is the rate for 2024 with the COLA adjustment that may also have been misapplied–everyone would have to check to know if it was misapplied to them.

You can check out any time you like, but you can never leave. Hotel California, written by Don Felder, Glenn Frey and Don Henley

There’s no opt-out in either the Hotel California or the compulsory song license. And Amazon’s demand for a royalty refund from songwriters demonstrates once again the madness of the Copyright Royalty Board rate-setting procedures. Whether it creates enough ripples in the booming business around buying out songwriter royalties remains to be seen.

How did we get to this point in the circus act? You may have noticed that sliced bread is in close competition with fire and the wheel for second place behind Greatest Human Accomplishments. Both fire and the wheel are yielding to streaming mechanical royalty rates in the Phonorecords III remand negotiations. Yes, the so-called “headline rates” in Phonorecords III (or “PR III”) are a Nobel-worthy accomplishment. At least according to the press agents.

And yet something curious has happened. I’m told that Amazon, through its agent Music Reports (MRI), has posted what is essentially a demand letter in the MRI user portal. This demand letter instructs publishers who have directly licensed songs to Amazon to pay up because of an overpayment of streaming mechanicals due to the adjustment required by the new-ish Phonorecords III remand rates that finally set the streaming mechanical rates for the industry. Something similar may be happening at the MLC; we’ll come to that below in just a bit.

In a testament to just how whack the Copyright Royalty Board system actually is, the PR III remand concerns royalties paid from 2018 through 2022. That’s right—starting six years ago. This is largely due to the failure of the publishers to obtain a waiver of the PR III decision as a negotiating chip when they gave away the rest of the farm in Title I of the Music Modernization Act (also hailed as a great gift to songwriters). But I’d say it is primarily due to the desire of digital music services like Amazon—including the largest corporations in commercial history—to crush the kitchen tables of songwriters. Because judging by the massive overlawyering in the Copyright Royalty Board, that sure looks like the motive.

And when it comes to the services crushing the little people, money is no object, even if they spend more on litigation than the royalty increase cost them. Evidently the sadistic psychic benefit greatly exceeds the cost.

But Amazon evidently has discovered that even after all the shenanigans with PR III, it appears that they paid too much and now they want it back. That’s right—Amazon shamelessly wants you to cut them a check. Because a market value over $2,000,000,000,000 is just not enough. I wonder which buffoon advised Mr. Bezos that was a good idea.

Here’s what it looks like on MRI:

A few questions come to mind. First, realize what Amazon is saying. They were evidently accounting to publishers at the rates for Phonorecords II during the several years that the PR III rates were on appeal and then re-litigated before the Copyright Royalty Board. The final PR III rates (sometimes called “remand rates”) issued in August of last year (2023) were supposed to be an improvement over the PR II rates don’t you know. At least according to the braying that accompanied the announcement. In fact, the PR III remand rates where it all ended up were themselves supposed to be an improvement, meaning that publishers were to be paid more under PR III than under PR II. Maybe that’s the difference between an increase in the payable rates compared to an increase in the payable royalties.

So if that’s true, and if Amazon paid PR II rates during the lengthy PR III appeal, why is there now an overpayment by Amazon? An overpayment that they now want you to pay back? Wouldn’t you expect to see the true-up on new rates result in publishers receiving a credit for increased rates? Especially if the stream counts and subscriber totals stayed the same on these previously-issued accounting statements? (Not to mention this may be happening at other services, too.)

Some of these PR III statements pre-date and overlap with the MLC’s creation and the “license availability date” for the 2021 blanket license established under Title I of the MMA. That means that if you or your publisher had a direct deal with Amazon during the PR III rate period, there may be overlapping periods when the MLC took over Amazon’s accountings.

It has long been the standard industry practice that overpayments are just debited to your royalty account. Nobody asks you to cut a check. Debiting your account is not much better–you still have to pay them back, and the so-called “overpayment” will still potentially zero out your MLC accounts, too. If you did a royalty buyout that included an assumption that these royalties would be paid, your financier may come up short under either direct license or MLC.

This is particularly true for publishing administrators. If a service were to debit an administrator’s account, that might result in the administrator having to go out of pocket in order to pay some of their publishers for the amount of the demand. If that overpayment is large enough, that administrator may owe royalties to publishers that did not have the benefit of the overpayment. This is pretty elementary math, 2 plus 2 being what it is. You don’t even have to carry the 1.

However, great news! Amazon will give you an interest-free payday loan so you can pay down your new debt over six months. Or before they send it to collection.

Now the MLC—it’s entirely possible that Amazon is pulling the same stunt under the statutory license. However, it appears that MLC is doing what is normally done in these situations and will be debiting and crediting as necessary. If you’re concerned, it would be worth checking and asking for an explanation from the MLC.

Even so, it does not change anything about why there is an overpayment in the first place. If there were ever a situation that cried out for an intensive royalty compliance exam, this is it. It is hard to believe that all this to-ing and fro-ing with your royalty payments across multiple rates in multiple accounting periods hasn’t resulted in mistakes. No crime, it’s complex. That’s why we have audits. At a minimum, Amazon needs to provide publishers with a detailed breakdown of how the repayment was determined along with an explanation of where the rates changed that caused the overpayment.

That’s why Amazon and any other similarly situated service should welcome an extensive audit. In fact, the MLC should just include the true-up (or true-down in Amazon’s case) in their already-noticed audit of Amazon. This episode also raises the question of who else is going to pull the same stunt.

This slice of life demonstrates once again how unworkable the entire Copyright Royalty Board system is for streaming mechanical royalties. The services get to drag out appeals forever, and songwriters pay the consequences. But like the man said, you can never leave. And the Music Modernization Act just got every one locked in even deeper.

[A version of this post first appeared on MusicTechPolicy]

Summary: The fight over frozen mechanicals continues to pay off as songwriters log another cost of living increase for physical/downloads while streaming falls farther behind.

The Copyright Royalty Board adjusted the US statutory mechanical royalty for physical carriers like vinyl, CDs and downloads annually during the current rate period. This is entirely due to the success of public comments by the ad hoc songwriter bargaining group that persuaded the Copyright Royalty Judges to reject the terrible “frozen mechanicals” settlement negotiated with the NMPA, NSAI and RIAA.

As it turned out, once the judges rejected the freeze as unfair, the labels quickly agreed to a fair result that increased the physical/download rate from a 9.1¢ base rate to the 12¢ rate suggested by the Judges which went a long way to making up for the 15 year freeze at 9.1¢. In fact, if it had just been presented to the labels to begin with, a tremendous amount of agita could have been saved all round.

Crucially, not only did the base rate increase to 12¢, the judges also approved a prospective cost of living adjustment determined by a formula using the Consumer Price Index. The end result is that unlike streaming mechanicals paid by the streaming services like Spotify (i.e., not the labels) the value of the increase from 9.1¢ to 12¢ has been protected from inflation during the rate period (2023-2027).

Unfortunately, the streaming services were allowed to reject a cost of living for streaming mechanicals, notwithstanding the Judges’ and the services’ acceptance of an COLA-type adjustment to the multimillion dollar budget of the Mechanical Licensing Collective. That COLA is ased on a government measurement of inflation (the Employment Cost Index) comparable to the CPI-U that is used to increase the services’ financing of salaries and other costs at the Mechanical Licensing Collective. So those who are paid handsomely to collect and pay songwriters get a better deal than the songwriters they supposedly serve.

What is the increase in pennies this year for the physical/download mechanical rate? The Judges determine the inflation-adjusted rate every year during the five year rate period (2023-2027). The calculation is made in December for physical/download with reference to the CPI-U rate announced by the Bureau of Labor Statistics as of December 1, which means the rate published on November 11. The new rate goes into effect on January 1, 2025.

At this point, there does not seem to be any indication that there will be a large spike in inflation between now and November 11, so we can use the September rate (just announced in October) to make an educated guess as to what the 2025 statutory rate increase will be for physical/downloads (rounded down):

So we can safely project that the base rate will increase from 12.4¢ for 2024 to about 12.6¢ in 2025 without firing a shot. If you have a 10 x 3/4 rate controlled compositions clause, that means the U.S. controlled pool on physical will be approximately 94.5¢ instead of the old frozen rate of 68.25¢.

It’s important to note a couple things about the relevance of CPI-U as a metric for protecting royalty rates from the ravages of inflation. First of all, the CPI-U is a statistical smoothing of the specific rates for particular goods and services that it measures and doesn’t reflect the magnitude of changes of some components.

For example, the September CPI-U increased by 0.2% on a seasonally adjusted basis. However, the shelter index and the food index increased at higher rates:

The shelter index rose by 0.2%, and the food index increased by 0.4% Together, these two components contributed over 75% of the monthly increase in the all items index.

Chris Castle said, “These are good benchmarks to keep in mind as we head into a new rate setting period in a year or so when I expect songwriters to demand a COLA for streaming mechanicals. No more poormouthing from the services. If they can give it to MLC, they can give it to the songwriters, too.”

One of the most common questions we get from songwriters about the MLC concerns the gigantic level of “unmatched funds” that have been sitting in the MLC’s accounts since February 2021. Are they really just waiting until The MLC, Inc. gets redesignated and then distributes hundreds of millions on a market share basis like the lobbyists drafted into the MMA?

Not My Monkey

Nobody can believe that the MLC can’t manage to pay out several hundred million dollars of streaming mechanical royalties for over three years so far. (Resulting in the MLC holding $804,555,579 in stocks as of the end of 2022 on its tax return, Part X, line 11.) The proverbial monkey with a dart board could have paid more songwriters in three years. Face it—doesn’t it just sound illegal? In my experience, when something sounds or feels illegal, it probably is.

What’s lacking here is a champion to extract the songwriters’ money. Clearly the largely unelected smart people in charge could have done something about it by now if they wanted to, but they haven’t. It’s looking more and more like nobody cares or at least nobody wants to do anything about it. There is profit in delay.

Or maybe nobody is taking responsibility because there’s nobody to complain to. Or is there? What if such a champion exists? What if there were no more waiting? What if there were someone who could bring the real heat to the situation?

Let’s explore one potentially overlooked angle—a federal agency called the Office of the Inspector General. Who can bring in the OIG? Who has jurisdiction? I think someone does and this is the primary reason why the MLC is different from HFA.

Does The Inspector General Have MLC Jurisdiction?

Who has jurisdiction over the MLC (aside from its severely conflicted board of directors which is not setting the world on fire to pump the hundreds of millions of black box money back into the songwriter economy). The Music Modernization Act says that the mechanical licensing collective operates at the pleasure of the Congress under the oversight of the U.S. Copyright Office and the OIG has oversight of the Copyright Office through its oversight of the Library of Congress.

But, hold on, you say. The MLC, Inc. is a private company and the government typically does not have direct oversight over the operations of a private company.

The key concept there is “operates” and that’s the difference between the statutory concept of a mechanical licensing collective and the actual operational collective which is a real company with real employees and real board members. Kind of like shadows on the wall of a cave for you Plato fans. Or the magic 8 ball.

The MLC, Inc. is all caught up with the government. It exists because the government allows it to, it collects money under the government’s blanket mechanical license, its operating costs are set by the government, and its board members are “inferior officers” of the United States. Even though The MLC, Inc. is technically a private organization, it is at best a quasi-governmental organization, almost like the Tennessee Valley Authority or the Corporation for Public Broadcasting. So it seems to me that The MLC, Inc. is a stand-in for the federal government.

But The MLC, Inc. is not the federal government. When Congress passed the MMA and it charged the Copyright Office with oversight of the MLC. Unfortunately, Congress does not appear to have appropriated funds for the additional oversight work it imposed on the Office.

Neither did Congress empower the Office to charge the customary reasonable fees to cover the oversight work Congress mandated. The Copyright Office has an entire fee schedule for its many services, but not MLC oversight.

Even though the MLC’s operating costs are controlled by the Copyright Royalty Board and paid by the users of the blanket license through an assessment, this assessment money does not cover the transaction cost of having the Copyright Office fulfill an oversight role.

An oversight role may be ill suited to the historical role of the Copyright Office, a pre-New Deal agency with no direct enforcement powers—and no culture of cracking heads about wasteful spending like sending a contingent to Grammy Week.

In fact, there’s an argument that The MLC, Inc. should write a check to the taxpayer to offset the additional costs of MLC oversight. If that hasn’t happened in five years, it’s probably not going to happen.

Where Does the Inspector General Fit In?

Fortunately, the Copyright Office has a deep bench to draw on at the Office of the Inspector General for the Library of Congress, currently Dr. Glenda B. Arrington. That kind of necessary detailed oversight is provided through the OIG’s subpoena power, mutual aid relationships with law enforcement partners as well as its own law enforcement powers as an independent agency of the Department of Homeland Security. Obviously, all of these functions are desirable but none of them are a cultural fit in the Copyright Office or are a realistic resource allocation.

The OIG is better suited to overseeing waste, fraud and abuse at the MLC given that the traditional role of the Copyright Office does not involve confronting the executives of quasi-governmental organizations like the MLC about their operations, nor does it involve parsing through voluminous accounting statements, tracing financial transactions, demanding answers that the MLC does not want to give, and perhaps even making referrals to the Department of Justice to open investigations into potential malfeasance.

Or demanding that the MLC set a payment schedule to pry loose the damn black box money.

One of the key roles of the OIG is to conduct audits. A baseline audit of the MLC, its closely held investment policy and open market trading in hundreds of millions in black box funds might be a good place to start.

It must be said that the first task of the OIG might be to determine whether Congress ever authorized MLC to “invest” the black box funds in the first place. Congress is usually very specific about authorizing an agency to “invest” other people’s money, particularly when the people doing the investing are also tasked with finding the proper owners and returning that money to them, with interest.

None of that customary specificity is present with the MLC.

For example, MLC CEO Kris Ahrens told Congress that the simple requirement that the MLC pay interest on “unmatched” funds in its possession (commonly called “black box”) was the basis on which the MLC was investing hundreds of millions in the open market. This because he assumed the MLC would have to earn enough from trading securities or other investment income to cover their payment obligations. That obligation is mostly to cover the federal short term interest rate that the MLC is required to pay on black box.

The Ghost of Grammy Week

The MLC has taken the requirement that the MLC pay interest on black box and bootstrapped that mandate to justify investment of the black box in the open market. That is quite a bootstrap.

An equally plausible explanation would be that the requirement to pay interest on black box is that the interest is a reasonable cost of the collective to be covered by the administrative assessment. The plain meaning of the statute reflects the intent of the drafters—the interest payment is a penalty to be paid by the MLC for failing to find the owners of the money in the first place, not an excuse to create a relatively secret $800 million hedge fund for the MLC.

I say relatively secret because The MLC, Inc. has been given the opportunity to inform Congress of how much money they made or lost in the black box quasi-hedge fund, who bears the risk of loss and who profits from trading. They have not answered these questions. Perhaps they could answer them to the OIG getting to the bottom of the coverup.

We do not really know the extent of the MLC’s black box holdings, but it presumably would include the hundreds of millions invested under its stewardship in the $1.9 billion Payton Limited Maturity Fund SI (PYLSX). Based on public SEC filings brought to my attention, The MLC, Inc.’s investment in this fund is sufficient to require disclosure by PYLSX as a “Control Person” that owns 25% or more of PYLSX’s $1.9 billion net asset value. PYLSX is required to disclose the MLC as a Control Person in its fundraising materials to the Securities and Exchange Commission (Form N-1A Registration Statement filed February 28, 2023). This might be a good place to start.

Otherwise, the MLC’s investment policy makes no sense. The interest payment is a penalty, and the black box is not a profit center.

But you don’t even have to rely on The MLC, Inc.’s quasi governmental status in order for OIG to exert jurisdiction over the MLC. It is also good to remember that the Presidential Signing Statement for the Music Modernization Act specifically addresses the role of the MLC’s board of directors as “inferior officers” of the United States:

Because the directors [likely both voting and nonvoting] are inferior officers under the Appointments Clause of the Constitution, the Librarian [of Congress] must approve each subsequent selection of a new director. I expect that the Register of Copyrights will work with the collective, once it has been designated, to ensure that the Librarian retains the ultimate authority, as required by the Constitution, to appoint and remove all directors.

The term “inferior officers” refers to those individuals who occupy positions that wield significant authority, but whose work is directed and supervised at some level by others who were appointed by presidential nomination with the advice and consent of the Senate. Therefore, the OIG could likely review the actions of the MLC’s board (voting and nonvoting members) as they would any other inferior offices of the United States in the normal course of the OIG’s activities.

Next Steps for OIG Investigation

How would the OIG at the Library of Congress actually get involved? In theory, no additional legislation is necessary and in fact the public might be able to use the OIG whistleblower hotline to persuade the IG to get involved without any other inputs. The process goes something like this:

Receipt of Allegations: The first step in the OIG investigation process is the receipt of allegations. Allegations of fraud, waste, abuse, and other irregularities concerning LOC programs and operations like the MLC are received from hotline complaints or other communications.

Preliminary Review: Once an allegation is received, it undergoes a preliminary review to determine if OIG investigative attention is warranted. This involves determining whether the allegation is credible and reasonably detailed (such as providing a copy of the MLC Congressional testimony including Questions for the Record). If the Office is actually bringing the OIG into the matter, this step would likely be collapsed into investigative action.

Investigative Activity: If the preliminary review warrants further investigation, the OIG conducts the investigation through a variety of activities. These include record reviews and document analysis, witness and subject interviews, IG and grand jury subpoenas, search warrants, special techniques such as consensual monitoring and undercover operations, and coordination with other law enforcement agencies, such as the FBI, as appropriate. That monitoring might include detailed investigation into the $500,000,000 or more in black box funds, much of which is traded on open market transactions like PYLSX.

Investigative Outputs: Upon completing an investigation, reports and other documents may be written for use by the public, senior decision makers and other stakeholders, including U.S. Attorneys and Copyright Office management. Results of OIG’s administrative investigations, such as employee and program integrity cases, are transmitted to officials for appropriate action.

Monitoring of Results: The OIG monitors the results of those investigations conducted based on OIG referrals to ensure allegations are sufficiently addressed.

So it seems that the Office of the Inspector General is well suited to assisting the Copyright Office by investigating how the MLC is complying with its statutory financial obligations. In particular, the OIG is ideally positioned to investigate how the MLC is handling the black box and its open market investments that it so far has refused to disclose to Members of Congress at a Congressional hearing as well as in answers to Questions for the Record from Chairman Issa.

This post previously appeared on MusicTech.Solutions

One of the hallmarks of mania is the rapid rise and complexity of the rates of fraud. And did you know they’re going up?

The Big Short, screenplay by Charles Randolph and Adam McKay, based on the book by Michael Lewis

We have often said that if screwups were Easter eggs, Spotify CEO Daniel Ek would be the Easter bunny, hop hop hopping from one to the next. That’s is not consistent with his press agent’s pagan iconography, but it sure seems true to many people.

This week was no different. Mr. Ek cashed out hundreds of millions in Spotify stock while screwing songwriters hard with a lawless interpretation of the songwriter compulsory license. That interpretation is so far off the mark that he surely must know exactly what he is doing. It’s yet another manifestation of Spotify’s sudden obsession with finding profits after a decade of “get big fast.”

The Bunny’s Bundle

Let’s look under the hood at the part they don’t tell you much about. Mr. Ek evidently has what’s called a “10b5-1 agreement” in place with Spotify allowing staggered sales of incremental tranches of the common stock. Those sales have to be announced publicly which Spotify complied with (we think). And we’ll say it again for the hundredth time, stock is where the real money is at this stage of Spotify’s evolution, not revenue.

As a founder of Spotify, Mr. Ek holds founders shares plus whatever stock awards he has been granted by the board he controls through his supervoting stock that we’ve discussed with you many times. These 10b5-1 agreements are a common technique for insiders, especially founders, who hold at least 10% of the company’s shares, to cash out and get the real money through selling their stock.

A 10b5-1 agreement establishes predetermined trading instructions for company stock (usually a sale so not trading the shares) consistent with SEC rules under Section 10b5 of the Securities and Exchange Act of 1934 covering when the insider can sell. Why does this exist? The rule was established in 2000 to protect Silicon Valley insiders from insider trading lawsuits. Yep, you caught it–it’s yet another safe harbor for the special people. Presumably Mr. Ek’s personal agreement is similar if not identical to the safe harbor terms because that’s why the terms are there.

As MusicBusinessWorldWide reported, Mr. Ek recently sold $118.8 million in shares of Spotify at roughly the same time that he likely knew Spotify was planning to change the way his company paid songwriters on streaming mechanicals, or as it’s also known “material nonpublic information”.

As Tim Ingham notes in MusicBusinessWorldwide, Mr. Ek has had a few recent sales under his 10b5-1 agreement: “Across these four transactions (today’s included), Ek has cashed out approximately $340.5 million in Spotify shares since last summer.” Rough justice, but I would place a small wager that Ek has cashed out in personal wealth all or close to all of the money that Spotify has paid to songwriters (through their publishers) for the same period. In this sense, he is no different than the usual disproportionately compensated CEOs at say Google or Raytheon.

Stock buybacks artificially increase share price. Now why might Spotify want to juice its own stock price?

Spotify Shoves a “Bundled” Rate on Songwriters

Spotify’s argument (that may have caused a jump in share price) claims that its recent audiobook offering made Spotify subscriptions into a “bundle” for purposes of the statutory mechanical rate. (While likely paying an undiscounted royalty to the books.)

That would be the same bundled rate that was heavily negotiated in the 2021-22 “Phonorecords IV” proceeding at the Copyright Royalty Board at great expense to all concerned, not to mention torturing the Copyright Royalty Judges. These Phonorecords IV rates are in effect for five years, but the next negotiation for new rates is coming soon (called Phonorecords V or PR V for short). We’ll get to the royalty bundle but let’s talk about the cash bundle first.

You Didn’t Build That

Don’t get it wrong, we don’t begrudge Mr. Ek the opportunity to be a billionaire. We don’t at all. But we do begrudge him the opportunity to do it when the government is his “partner” so they can together put a boot on the necks of songwriters. This is how it is with statutory mechanical royalties; he benefits from various other safe harbors, has had his lobbyists rewrite Section 115 to avoid litigation in a potentially unconstitutional reach back safe harbor, and he hired the lawyer at the Copyright Office who largely wrote the rules that he’s currently bending. Yes, we do begrudge him that stuff.

And here’s the other effrontery. When Daniel Ek pulls down $340.5 million as a routine matter, we really don’t want to hear any poor mouthing about how Spotify cannot make a profit because of the royalty payments it makes to artists and songwriters. (Or these days, doesn’t make to some artists.) This is, again, why revenue share calculations are just the wrong way to look at the value conferred by featured and nonfeatured artists and songwriters on the Spotify juggernaut. That’s also the point Chris made in some detail in the paper he co-wrote with Professor Claudio Feijoo for WIPO that came up in Spain, Hungary, France, Uruguay and other countries.

Spotify pays a percentage of revenue on what is essentially a market share basis. Market share royalties allows the population of recordings to increase faster than the artificially suppressed revenue, while excluding songwriters from participating in the increases in market value reflected in the share price. That guarantees royalties will decline over time. Nothing new here, see the economist Thomas Malthus, workhouses and Charles Dickens‘ Oliver Twist.

The market share method forces songwriters to take a share of revenue from someone who purposely suppressed (and effectively subsidized) their subscription pricing for years and years and years. (See Robert Spencer’s Get Big Fast.). It would be a safe bet that the reason they subsidized the subscription price was to boost the share price by telling a growth story to Wall Street bankers (looking at you, Goldman Sachs) and retail traders because the subsidized subscription price increased subscribers.

Just a guess.

The Royalty Bundle

Now about this bundled subscription issue. One of the fundamental points that gets missed in the statutory mechanical licensing scheme is the compulsory license itself. The fact that songwriters have a compulsory license forced on them for one of their primary sources of income is a HUGE concession. We think the music services like Spotify have lost perspective on just how good they’ve got it and how big a concession it is.

The government has forced songwriters to make this concession since 1909. That’s right–for over 100 years. A century.

A decision that seemed reasonable 100 years ago really doesn’t seem reasonable at all today in a networked world. So start there as opposed to the trope that streaming platforms are doing us a favor by paying us at all, Daniel Ek saved the music business, and all the other iconographic claptrap.

Has anyone seen them in the same room at the same time?

The problem with the Spotify move to bundled subscriptions is that it can happen in the middle of a rate period and at least on the surface has the look of a colorable argument to reduce royalty payments. If you asked songwriters what they thought the rule was, to the extent they had focused on it at all after being bombarded with self-congratulatory hoorah, they probably thought that the deal wasn’t “change rates without renegotiating or at least coming back and asking.”

And they wouldn’t be wrong about that, because it is reasonable to ask that any changes get run by your, you know, “partner.” Maybe that’s where it all goes wrong. Because it is probably a big mistake to think of these people as your “partner” if by “partner” you mean someone who treats you ethically and politely, reasonably and in good faith like a true fiduciary.

They are not your partner. Don’t normalize that word.

A Compulsory License is a Rent Seeker’s Presidential Suite

But let’s also point out that what is happening with the bundle pricing is a prime example of the brittleness of the compulsory licensing system which is itself like a motel in the desolate and frozen Cyber Pass with a light blinking “Vacancy: Rent Seekers Wanted” surrounded by the bones of empires lost. Unlike the physical mechanical rate which is a fixed penny rate per transaction, the streaming mechanical is a cross between a Rube Goldberg machine and a self-licking ice cream cone.

The Spotify debacle is just the kind of IED that was bound to explode eventually when you have this level of complexity camouflaging traps for the unwary written into law. And the “written into law” part is what makes the compulsory license process so insidious. When the roadside bomb goes off, it doesn’t just hit the uparmored people before the Copyright Royalty Board–it creams everyone.

David and friends tried to make this point to the Copyright Royalty Judges in Phonorecords IV. They were not confused by the royalty calculations–they understood them all too well. They were worried about fraud hiding in the calculations the same way Michael Burry was worried about fraud in The Big Short. Except there’s no default swaps for songwriters like Burry used to deal with fraud in subprime mortgage bonds.

Here’s how the Judges responded to David, you decide if they are condescending or if the songwriters were prescient knowing what we know now:

While some songwriters or copyright owners may be confused by the royalties or statements of account, the price discriminatory structure and the associated levels of rates in settlement do not appear gratuitous, but rather designed, after negotiations, to establish a structure that may expand the revenues and royalties to the benefit of copyright owners and music services alike, while also protecting copyright owners from potential revenue diminution. This approach and the resulting rate setting formula is not unreasonable. Indeed, when the market itself is complex, it is unsurprising that the regulatory provisions would resemble the complex terms in a commercial agreement negotiated in such a setting.

It must be said that there never has been a “commercial agreement negotiated in such a setting” that wasn’t constrained by the compulsory license. It’s unclear what the Judges even mean. But if what the Judges mean is that the compulsory license approximates what would happen in a free market where the songwriters ran free and good men didn’t die like dogs, the compulsory license is nothing like a free market deal.

If the Judges are going to allow services to change their business model in midstream but essentially keep their music offering the same while offloading the cost of their audiobook royalties onto songwriters through a discount in the statutory rate, then there should be some downside protection. Better yet, they should have to come back and renegotiate or songwriters should get another bite at the apple.

Unfortunately, there are neither, which almost guarantees another acrimonious, scorched earth lawyer fest in PR V coming soon to a charnel house near you.

Eject, Eject!

This is really disappointing because it was so avoidable if for no other reason. It’s a great time for someone…ahem…to step forward and head off the foreseeable collision on the billable time highway. The Judges surely know that the rate calculation is a farce

But the Judges are dealing with people negotiating the statutory license who have made too much money negotiating it to ever give it up willingly although a donnybrook is brewing. This inevitable dust up means other work will suffer at the CRB. It must be said in fairness that the Judges seem to find it hard enough to get to the work they’ve committed to according to a recent SoundExchange filing in a different case (SDARS III remand from 2020).

That’s not uncharitable–I’m merely noting that when dozens of lawyers in the mechanical royalty proceedings engage in what many of us feel are absurd discovery excesses. When there are stupid lawyer tricks at the CRB, they are–frankly–distracting the Judges from doing their job by making them focus on, well, bollocks. We’ll come back to this issue in future. The dozens and hundreds of lawyers putting children through college at the CRB–need to take a breath and realize that judicial resources at the CRB are a zero sum game. This behavior isn’t fair to the Judges and it’s definitely not fair to the real parties in interest–the songwriters.

Tell the Horse to Open Wider

A compulsory license in stagflationary times is an incredibly valuable gift, and when you not only look the gift horse in the mouth but ask that it open wide so you can check the molars, don’t be surprised if one day it kicks you.

Ever wonder who owns the registration data you have slaved to correct and recorrect at your own cost when you “Play Your Part” to “Correct to Collect” at the MLC?

Remember the sainted Music Modernization Act allowed the lobbyists a vehicle to create their mechanical licensing collective in the US that was going to solve all of Big Tech’s problems. The MMA, unsurprisingly, also gave Big Tech a brand new copyright infringement safe harbor arising out of the Spotify class actions. Generations of the children of lawyers and lobbyists will be put through college–thank you songwriters!

One of the few things Congress got right in Title I of the Music Modernization Act is the five-year review of the mechanical licensing collective. Or more precisely, whether the private company previously designated by the Copyright Office to conduct the functions of the Mechanical Licensing Collective (The MLC, Inc.) should have another five years to continue doing whatever it is they do.

Impliedly, and I think a bit unfairly, Congress told the Copyright Office to approve its own decision to appoint the current MLC or admit they made a mistake. This is yet another one of the growing list of oversights in the oversight. Wouldn’t it make more sense for someone not involved in the initial decision to be evaluating the performance of the MLC? Particularly when there are at least tens of millions of dollars changing hands as well as some highly compensated MLC employees, any one of whom makes more than the Copyright Royalty Judges. The MLC’s budget (paid by the services they oversee) was $32,900,000 in 2023 and will be $39,050,000 this year because, you know, the budget is indexed to inflation, just like streaming mechanicals…oh sorry. Not like streaming mechanicals.

Who Owns the Database?

What happens if the Register of Copyright actually fires The MLC, Inc. and designates a new MLC operator? The first question probably should be what is The MLC, Inc.’s plan for a hand off to a successor. But since that doesn’t exist, it instead should be what happens to the vaunted MLC musical works database and the attendant software and accounting systems which seem to be maintained out of the UK for some reason.

I actually raised this ownership question in a comment to the Copyright Office back in 2020. In short, my question was probably more of a statement: ‘‘The musical works database does not belong to the MLC or The MLC and if there is any confusion about that, it should be cleared up right away.”

The Copyright Office had a very clear response:

While the mechanical licensing collective must ‘‘establish and maintain a database containing information relating to musical works,’’ the statute and legislative history emphasize that the database is meant to benefit the music industry overall and is not ‘‘owned’’ by the collective itself….Any use by the Office referring to the public database as ‘‘the MLC’s database’’ or ‘‘its database’’ was meant to refer to the creation and maintenance of the database, not ownership. [85 FR at 58172, text accompanying notes 30 and 31.]

So if the current operator of the MLC is fired, we know from the MMA and the Copyright Office guidance that one thing The MLC, Inc. cannot do is hold the database and its attendant systems hostage, or demand payment, or any other shadiness. These items do not belong to them so they must not assert control over that which they do not own. Neither does the database belong to any contractor if for no other reason than the MLC, Inc. cannot transfer to a contractor something that the MLC, Inc. doesn’t own in the first place.

Another thing that doesn’t belong to The MLC, Inc. is the hundreds of millions of black box money that the MLC, Inc. has failed to distribute in going on four years. I’ve even heard cynics suggest that the market share distribution of black box will occur immediately following The MLC, Inc.’s redesignation and the corresponding renewal of HFA’s back office contract which seems to be worth about $10 million a year all by itself.

What would also have been helpful would be for Congress to have required the Copyright Office to publish evaluation criteria for what they expected the MLC’s operator to actually do as well as performance benchmarks. Like I said, it’s a bit unfair of Congress to put the Copyright Office in the unprecedented position of evaluating such an important role with no usable guidance whatsoever. Surely Congress did not intend for the Copyright Office to have unfettered autonomy in deciding what standards to apply to their review of a quasi-governmental agency like the MLC? Yet Congress seems to have defaulted to the guardrail of the Administrative Procedures Act or some other backstop to sustain checks and balances on the situation.

Thanks to the efforts of the “frozen mechanicals” commenters to the Copyright Royalty Judges and the labels who agreed to the structure, there is now an annual cost of living adjustment (called a “COLA”) for the statutory mechanical royalty paid for songs on physical (like vinyl or CDs) and permanent downloads. Starting this month and going forward, that COLA is made by the Copyright Royalty Judges in December, effective the next January 1.

Remember that the frozen minimum statutory mechanical rate was 9.1¢ since 2006 but increased to 12¢ effective 1/1/23.

The Copyright Royalty Judges announced the new COLA rate yesterday which has increased to a minimum rate of 12.40¢ for recordings of songs with a running time of 5 minutes or less, and a per-minute long-song rate of 2.39¢. Depending on how frequently you get accountings, you could see that COLA rate increase show up on your next statements for sales after 1/1/24.

Remember, the purpose of having a COLA is to preserve the buying power of the government’s royalty because songwriters get one opportunity every five years to negotiate compensation for mechanical royalties. Of course, the COLA rate may get distorted by “controlled compositions” clauses in artist agreements, so check your contracts.

Also remember that the rate paid for physical and downloads is actually paid by the record companies as the “licensee” who agreed to the COLA on royalties they pay.

The rate paid for streaming is paid by the digital music platforms like Spotify, Apple, Google, Amazon, Tidal and others.

There is no COLA adjustment for streaming even though same songs and same time period and even though the MLC gets a guaranteed annual increase in its “administrative assessment”.

2024 rate. For the year 2024 for every physical phonorecord and Permanent Download the Licensee makes and distributes or authorizes to be made and distributed, the royalty rate payable for each work embodied in the phonorecord or Permanent Download shall be either 12.40 cents or 2.39 cents per minute of playing time or fraction thereof, whichever amount is larger.

You must be logged in to post a comment.