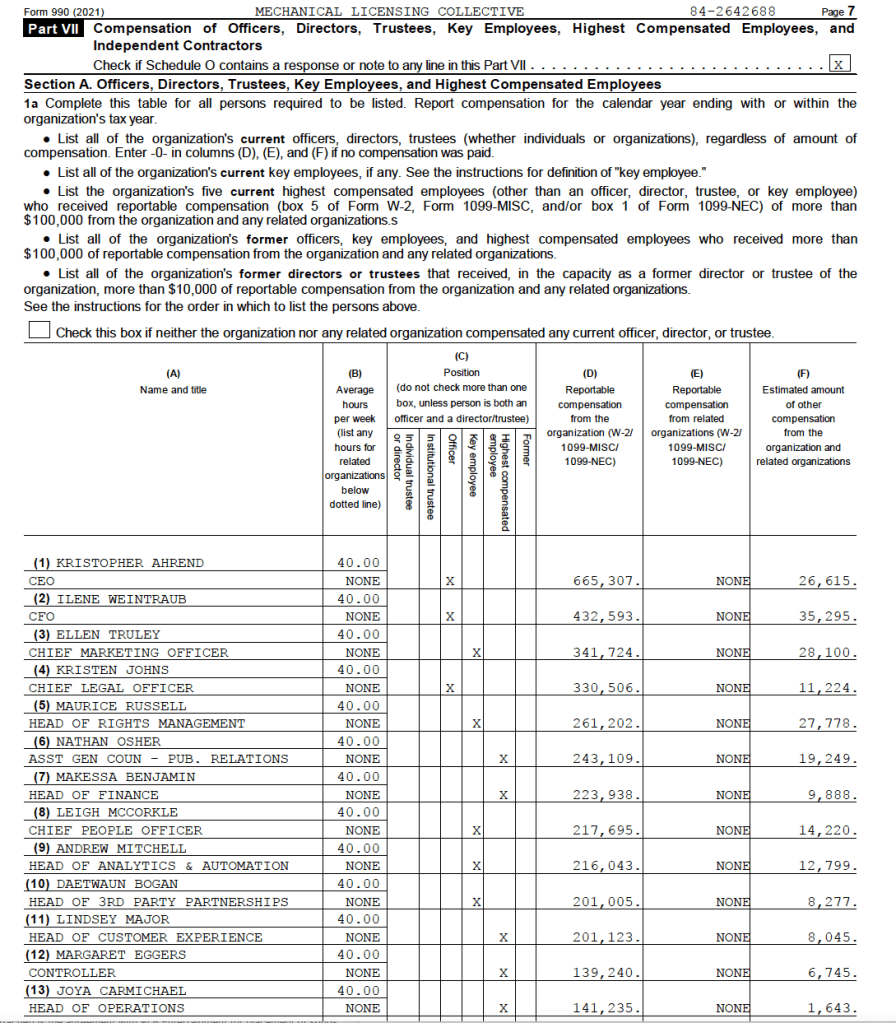

The MLC, Inc. has to disclose its “highly compensated” employees on its nonprofit Form 990 tax return for 2022 (note this probably doesn’t include travel to CES, the Grammys, MIDEM, SXSW, etc., etc.) The Copyright Office will be deciding very soon to keep the party going another five years.

In case you missed it, the MLC, Inc. was handed a five year contract in 2019 to operate the mechanical licensing collective. This contract was worth millions and millons of dollars, but more importantly guaranteed that the Harry Fox Agency would have a job for at least another five years. The salty arrangement was the brainchild of the lobbyists, the controlled opposition and the Copyright Office–and has resulted in The MLC, Inc. sitting on hundreds of millions of other peoples money.

The Copyright Office has posted a notice letting us know that the time has come for the circular admiration society also known as the 5 year review of the MLC and the DLC as required by Title I of the oh so modern Music Modernization Act (yet we keep comeing back to these age-old problems that are not modern at all). This is all conducted by the Copyright Office which in a meaningful way is simply reviewing how well the Copyright Office did with the designation of the MLC, Inc. as much as how well the MLC met expectations.

After suffering through establishing some regulations for the MLC that largely favored the services, the head lawyer at the Copyright Office threw down the pretenses and became employed as a lobbyist for Spotify. Another went to work for the National Association of Broadcasters to screw artists our of a performance right for sound recordings. Can’t wait to congratulate current Copyright Office staff on their employment futures after we get through this important reup for the MLC, Inc. and the lobbyists. I hear the chief butterfly killers have openings for copyright lawyers trained on the public purse.

The comment period in this vitally important review is divided into at least two parts: The special people, i.e., The MLC, Inc. quango and the DLC get to go first, and then the hoi polloi (that’s you and me). You’ll find this language buried at the very bottom of the Reup notice:

Interested members of the public are encouraged to comment on the topics addressed in the designees’ [i.e., the DLC or the MLC’s] submissions or raised by the Office in this notification of inquiry. Commenters may also address any topics relevant to this periodic review of the MLC and DLC designations. Without prejudice to its review of the current designations, the Office hopes that this proceeding will serve as an opportunity for any songwriter, publisher, or DMP who wishes to express concerns, satisfaction, or priorities with respect to the administration of the MMA’s blanket licensing regime to do so, and that any designated MLC or DLC will use that feedback to continually improve its services.

[Editor Charlie sez: a royalty “audit” is a right of the song owner to look inside the books and records of the party paying royalties to confirm that all royalties were paid and that all royalties were paid correctly, usually during a specified period of time. This usually results in the song owner discovering an underpayment that would have gone unpaid without the audit.]

It is commonplace for artists to conduct a royalty examination of their record company, sometimes called an “audit.” Until the Music Modernization Act, the statutory license did not permit songwriters to audit users of the statutory license. The Harry Fox Agency “standard” license for physical records had two principal features that differed from the straight statutory license: quarterly accounting and an audit right. When streaming became popular, the services both refused to comply with the statutory regulations and also refused to allow anyone to audit because the statutory regulations they failed to comply with did not permit an audit. I brought this absurdity to the attention of the Copyright Office in 2011.

After much hoopla, the lobbyists wrote an audit right for copyright owners into the Music Modernization Act. However, rather than permitting copyright owners to audit music users as is long standing common practice on the record side, the lobbyists decided to allow copyright owners to audit theMechanical Licensing Collective. At the expense of the copyright owner, of course, no matter how many mistakes the copyright owner discovered or how big the underpayment. This is consistent with the desire of services to distance themselves from those pesky songwriters by inserting the MLC in between the services and their ultimate vendors, the songwriters and copyright owners. The services can be audited by the MLC (whose salaries are paid by the services), but that hasn’t happened yet to my knowledge.

But the MLC has received what I believe is its first audit notice that was just published by the Copyright Office after receiving it on November 9. First up is Bridgeport Music, Inc. for the period January 1, 2021, through December 31, 2023. January 1, 2021 was the “license availability date” or the date that the MLC began accounting for royalties under the MMA’s blanket license.

Bridgeport’s audit is wise. There are no doubt millions if not billions of streams to be verified. The MLC’s systems are largely untested, compared to other music users such as record companies that have been audited hundreds, if not thousands of times depending on how long they are operating. Competent royalty examiners will look under the hood and find out whether it’s even possible to render reasonably accurate accounting statements given the MLC’s systems. Maybe it’s all fine, but maybe it’s not. The wisdom of Bridgeport’s two year audit window is that two years is long enough to have a chance at a recovery but it’s not so long that you are drowned in data and susceptible to taking shortcuts.

In other words, why wait around?

Auditing the Black Box

A big difference between the audit rules the lobbyists wrote into the MMA and other audits is that the MLC audit is based on payments, not statements. The relevant language in the statute makes this very clear (17 USC §115(d)(3)(L):

A copyright owner entitled to receive payments of royalties for covered activities from the mechanical licensing collective may, individually or with other copyright owners, conduct an audit of the mechanical licensing collective to verify the accuracy of royalty payments by the mechanical licensing collective to such copyright owner…The qualified auditor shall determine the accuracy of royalty payments, including whether an underpayment or overpayment of royalties was made by the mechanical licensing collective to each auditing copyright owner.

Royalty payments would include a share of black box royalties distributed to copyright owners. It seems reasonable that on audit a copyright owner could verify how this share was arrived at and whatever calculations would be necessary to calculate those payments, or maybe the absence of such payments that should have been made. Determining what is not paid that should have been paid is an important part of any royalty verification examination.

Systems Transparency

Information too confidential to be detected cannot be corrected. It is important to remember that copyright owner audits of the MLC will be the first time an independent third party has had a look at the accounting systems and functional technology of The MLC. If those audits reveal functional defects in the MLC’s systems or technology that affects any output of The MLC, i.e., not just the royalties being audited, it seems to me that those defects should be disclosed to the public. Audit settlements should not be used as hush money payments to keep embarrassing revelations from being publicly disclosed.

Unsurprisingly, The MLC lobbied to have broadly confidential treatment of all audits. Realize that there may well be confidential financial information disclosed as part of any audit that both copyright owners and The MLC will want to keep secret. There is no reason to keep secrets about The MLC’s systems. To take an extreme example, if on audit the auditors discovered that The MLC’s systems added 2 plus 2 and got 5, that is a fact that others have a legitimate interest in having disclosed to include the Copyright Office itself that is about to launch a 5 year review of The MLC for redesignation. Indeed, auditors may discover systemic flaws that could arguably require The MLC to recalculate many if not all statements or at least explain why they should not. (Note that a royalty auditor is required to deliver a copy of the auditor’s final report to The MLC for review even before giving it to their client. This puts The MLC on notice of any systemic flaws in The MLC’s systems found by the auditor and gives it the opportunity to correct any factual errors.)

I think that systemic flaws found by an auditor should be disclosed publicly after taking care to redact any confidential financial information. This will allow both the Copyright Office and MLC members to fix any discovered flaws.

The “Qualified Auditor” Typo

It is important to realize that there is no good reason why a C.P.A. must conduct the audit; this is another drafting glitch in the MMA that requires both The MLC’s audited financial statements and royalty compliance examinations be conducted by a C.P.A, defined as a “qualified auditor” (17 USC § 115(e)(25)). It’s easy to understand why audited financials prepared according to GAAP should be opined by a C.P.A. but it is ludicrous that a C.P.A. should be required to conduct a royalty exam for royalties that have nothing to do with GAAP and never have.

To be frank, I doubt seriously whether anyone involved in drafting the MMA had ever personally conducted or managed a royalty verification examination. That assessment is based on the fact that royalty verification examinations are one of the most critical parts of the royalty payment process and is the least discussed subject in the lengthy MMA; at the time, the lobbyists did not represent songwriters and tried very hard to keep songwriters inside the writer room and outside of the drafting room as you can tell from The MLC, Inc.’s board composition; and that the legislative history (at 20) has one tautological statement about copyright owner audits: ”Subparagraph L sets forth the verification and audit process for copyright owners to audit the collective, although parties may agree on alternate procedures.” Well no kidding, smart people. We’ll take some context if you got it.

As Warner Music Group’s Ron Wilcox testified to the Copyright Royalty Judges, “Because royalty audits require extensive technical and industry-specific expertise, in WMG’s experience a CPA certification is not generally a requirement for conducting such audits. To my knowledge, some of the. most experienced and knowledgeable royalty auditors in the music industry are not CPAs.” (Testimony of Ron Wilcox, In re Determination of Royalty Rates and Terms for Ephemeral Recording and Digital Performance of Sound Recordings (Web IV), Copyright Royalty Judges, Docket No. 14-CRB-0001-WR (Oct. 6, 2014) at 15.).

I would add to Ron’s assessment that the need for “extensive technical and industry-specific expertise” has grown exponentially since he made the statement in 2014 due to the complexity and numerosity of streaming. I’m sure Ron would agree if he had a chance to revisit his remarks. But inside the beltway of the Imperial City, it ain’t that way and you can tell by reading their laws handed down by the descendants of Marcus Licinius Crassus. All accountants are CPAs, all accounting is according to GAAP, all the women are strong, all the men are good-looking, and all the children are above average and go to Sidwell Friends. In the words of London jazzman and club owner Ronnie Scott to an unresponsive audience, “And now, back to sleep.”

The “qualified auditor” defined term should be limited to the MLC’s financials and removed from the audit clauses. This was a point I made to Senate staff during the drafting of MMA, but was told that while they, too, agreed it was stupid, it’s what the parties wanted (i.e., what the lobbyists wanted). And you know how that can be. So now we sweep up behind the elephants in the circus of life. But then, I’m just a country lawyer from Texas, what do I know.

If you’re like us, you have an office pool on who will win the eagerly anticipated release of the MLC’s 2022 tax return! “Winning” in this case means who will get the biggest salary and bonus bump–for what, we’re not sure, but don’t that stop anything.

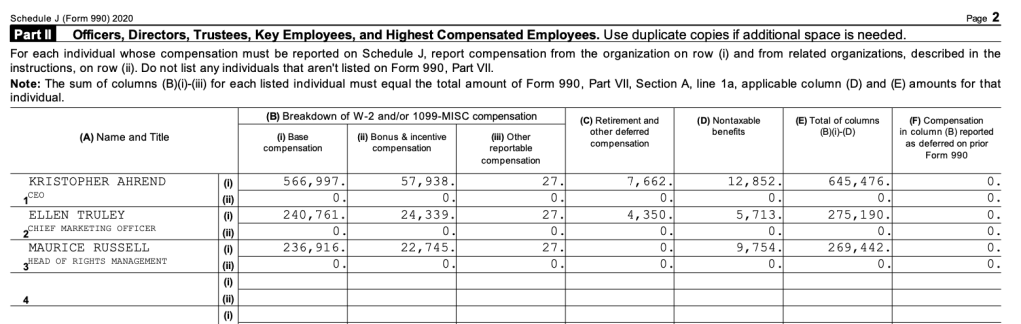

Based on the MLC’s 2020 tax return, these employees were the only ones disclosed:

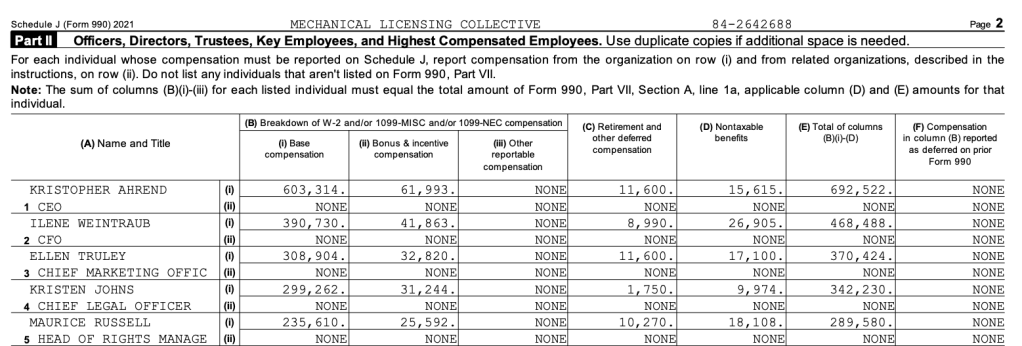

But on the 2021 tax return, the MLC must have exceeded expectations so much that everyone got a raise and they staffed up! Nothing but blue skies on the sunlight uplands!

CEO Kris Ahrend went from a mere $566K a year base with a $57K bonus in 2020 to $603K base and an even bigger bonus in 2021. Ellen Truley also had a fantastic year with her base moving like a rocket from a mere $240K to $308K! During COVID!! And her bonus practically doubled. But for some reason Maurice Russell’s salary actually declined slightly from $236K to $235K, but maybe they pushed it into his bonus which rose from $22K to $25K.

But stay tuned for the 2022 results and maybe bet the trendline going up, because the MLC gets a statutory cost of living adjustment that is not based on performance! Just like streaming royalties they administer!

No wait–the MLC gets the cost of living adjustment not the songwriters, sorry. No, remember that songwriters are told that they will do better if the services do better on revenues. Not on the services’ stock price, but rather on revenues for people who never raise their prices but make millions on selling stock. Except for the physical royalty paid by the labels that agreed to give the songwriters they depend on a higher mechanical rate AND a cost of living bump. But these trillion dollar market cap Big Tech music users don’t ever include the real money in the rising tide that sinks all boats with the trickle down royalty. But we’re told to put it all on red and let it ride.

But we’re glad that the MLC employees are so well compensated and that their salaries are protected in the highest inflation in 40 years with that built-in inflation adjustment.

Congress is considering whether to renew The MLC, Inc.‘s designation as the mechanical licensing collective. If that sentence seems contradictory, remember those are two different things: the mechanical licensing collective is the statutory body that administers the compulsory license under Section 115. The MLC, Inc. is the private company that was “designated” by Congress through its Copyright Office to do the work of the mechanical licensing collective. This is like the form of a body that performs a function (the mechanical licensing collective) and having to animate that form with actual humans (The MLC, Inc.), kind of like Plato’s allegory of the cave, shadows on the wall being what they are.

Congress reviews the work product of The MLC, Inc. every five years (17 USC §115(d)(3)(B)(ii)) to decide if The MLC, Inc. should be allowed to continue another five years. In its recent guidance to The MLC, Inc. about artificial intelligence, the Copyright Office correctly took pains to make that distinction in a footnote (footnote 2 to be precise. Remember–always read the footnotes, it’s often where the action is.). This is why it is important that we be clear that The MLC, Inc. does not “own” the data it collects (and that HFA as its vendor doesn’t own it either, a point I raised to Spotify’s lobbyist several years ago). Although it may be a blessing if Congress fired The MLC, Inc. and the new collective had to start from scratch.

But Congress likely would only re-up The MLC, Inc. if it had already decided to extend the statutory license and all its cumbersome and byzantine procedures, proceedings and prohibitions on the freedom of songwriters to collectively bargain. Not to mention an extraordinarily huge thumbs down on the scales in favor of the music user and against the interest of the songwriters. The compulsory license is so labyrinthine and Kafka-esque it is actually an insult to Byzantium, but that’s another story.

Rather than just deciding about who is going to get the job of administering the revenues for every songwriter in the world, maybe there should be a vote. Particularly because songwriters cannot be members of the mechanical licensing collective as currently operated. Congress did not ask songwriters what they thought when the whole mechanical licensing scheme was established, so how about now?

Before the Congress decides to continue The MLC, Inc. many believe strongly that the body should reconsider the compulsory license itself. It is the compulsory license that is the real issue that plagues songwriters and blocks a free market. The compulsory license really has passed its sell by date and it’s pretty easy to understand why its gone so sour. Eliminating the Section 115 license will have many implications and we should tread carefully, but purposefully.

Party Like it’s 1909

First of all, consider the actual history of the compulsory license. It’s over 100 years old, and it was established at a time, believe it or not, when the goal of Congress was to even the playing field between, music users and copyright owners. They were worried about music users being hard done by because of the anticompetitive efforts of songwriters and copyright owners. As the late Register Marybeth Peters told Congress, when Congress created the exclusive right to control reproduction and distribution in 1909, “…due to concerns about potential monopolistic behavior [by the copyright owners], Congress also created a compulsory license to allow anyone to make and distribute a mechanical reproduction of a nondramatic musical work without the consent of the copyright owner provided that the person adhered to the provisions of the license, most notably paying a statutorily established royalty to the copyright owner.”

Well, that ship has sailed, don’t you think?

This is kind of incredible when you think about it today because the biggest users of the compulsory license are those who torture the bejesus out of songwriters by conducting lawfare at the Copyright Royalty Board–the richest corporations in commercial history that dominate practically every moment of American life. In fact, the statutory license was hardly used at all before these fictional persons arrived on the scene and have been on a decades-long crusade to hack the Copyright Act through lawfare ever since. This is particularly true since about 2007 when Big Tech discovered Section 115. (And they’re about to do it again with AI–first they send the missionaries.)

If the purpose of the statutory scheme was to create a win-win situation that floats all boats, you would have expected to see songwriters profiting like never before, right? If the compulsory was so great, what we really needed was for everyone to use Section 115, right? Actually, the opposite has happened, even with decades of price fixing at 2¢ by the federal government. When hardly anyone used the compulsory license, songwriters prospered. When its use became widespread, songwriters suffered, and suffered badly.

Songwriters have been relegated to the bottom of the pile in compensation, a sure sign of no leverage because whatever leverage songwriters may have is taken–there’s that word again–by the compulsory license. I don’t think Google, a revanchist Microsoft, Apple, Amazon or Spotify need any protection from the anticompetitive efforts of songwriters. Google, Amazon, Apple, Microsoft, Spotify are only worried about “monopolistic behavior” when one of them does it to one of the others. The Five Families would tell you its nothing personal, it’s just business.

Yet these corporate neo-colonialists would have you believe that the first thing that happens when the writing room door closes is that songwriters collude against them. (Sounding very much like the Radio Music Licensing Committee–so similar it makes you wonder, speaking of collusion.)

The Five Year Plan

Merck Mercuriadis makes the good point that there is no time like the present to evolve: “In the United States, we have a position of stability for the next five years – at the highest rates paid to songwriters to date – in the evolution of the streaming economy. We are now working towards improving the songwriters’ share of the streaming revenue ‘pie’ yet further and, eventually, getting to a free market.” The clock is ticking on the next five years, a reference to the rate period set by the Copyright Royalty Board in the Phonorecords IV proceeding. (And that five years is a different clock than the five years clock on the MLC which is itself an example of the unnecessary confusion in the compulsory license.)

What would happen if the compulsory license vanished? Very likely the industry would continue its easily documented history of voluntary catalog licenses. The evidence is readily apparent for how the industry and music users handled services that did not qualify for a compulsory license like YouTube or TikTok. However stupid the deals were doesn’t change the fact that they happened in the absence of a compulsory license. That Invisible Hand thing, dunno could be good. Seems to work out fine for other people.

Let’s also understand that there is a cottage industry complete with very nice offices, pensions and rich salaries that has grown up around the compulsory license (or consent decrees for that matter). A cottage industry where collecting the songwriters’ money results in dozens of jobs paying more in a year than probably 95% of songwriters will make, maybe ever. (The Trichordist published an excerpt from a recent MLC tax return showing the highest compensated MLC employees.) Generations of lawyers and lobbyists have put generations of children through college and law school from legal fees charged in the pursuit of something that has never existed in the contemporary music business–a willing buyer and a willing seller. Those people will not want to abandon the very government policy that puts food on their tables, but both sides are very, very good at manufacturing excuses why the compulsory license really must be continued to further humanity.

The even sadder reality is that as much as we would like to simply terminate the compulsory license, there is a certain legitimacy to being clear-eyed about a transition. (An example is the proposals for transitioning from PRO consent decrees–ASCAP’s consent decree has been around a long time, too.) There would likely need to be a certain grandfathering in of services that were pre or post the elimination of the compulsory, but that’s easily done, albeit not without a last hurrah of legal fees and lobbyist invoices. Register Pallante noted in the well-received 2015 Copyright Office study (Copyright and the Music Marketplace at 5) “The Office thus believes that, rather than eliminating section 115 altogether, section 115 should instead become the basis of a more flexible collective licensing system that will presumptively cover all mechanical uses except to the extent individual music publishers choose to opt out.” An opt out is another acceptable stop along the way to liberation, or even perhaps a destination itself. David Lowery had a very well thought-out idea along these lines in the pre-MLC era that should be revisited.

X Day

However, while there is a certain attractiveness to having a plan that the dreaded “stakeholders” and their legions of lobbyists and lawyers agree with, it is crucially important for Congress to fix a date certain by which the compulsory license will expire. Rain or shine, plan or no plan, it goes away on the X Day, say five years from now as Merck suggests. So wakey, wakey.

That transparency drives a wedge into the process because otherwise millions will be spent in fees for profiting from moral hazard and surely the praetorians protecting the cottage industry wouldn’t want that. If you doubt that asking for a plan before establishing X Day would fail as a plan, just look at the Copyright Royalty Board and in particular the Phonorecords III remand. Years and years, multiple court rulings, and the rates still are not in effect. Perseveration is not perseverance, it’s compulsive repetition when you know the same unacceptable result will occur.

But don’t let people tell you that the sky will fall if Congress liberates songwriters from the government mandate. The sky will not fall and songwriters will have a generational opportunity to organize a collective bargaining unit with the right to say no to a deal.

Who can forget Sally Fields in Norma Rae?

The closest that Congress has come to a meaningful “vote” in the songwriting world is inviting public comments through interventions, rule makings, roundtables and the like–information gathering that is not controlled by the lobbyists. Indeed, it was this very process at the Copyright Royalty Board that resulted in many articulate comments by songwriters and publishers themselves that were clearly quite at odds with what the CRB was being fed by the lobbyists and lawyers. So much so that the Copyright Royalty Judges rejected not only the “Subpart B” settlement reached by the insiders but the very premise of that settlement. Imagine what might happen if the issue of the compulsory license itself was placed upon the table?

Now that songwriters have had a taste of how The MLC, Inc. has been handling their money, maybe this would be a good time to ask them what they think about how things are going. And whether they want to be liberated from the entire sinking ship that is designed to help Big Tech. And you can start by asking how they feel about the $500 million in black box money that is still sitting in the bank account of The MLC, Inc. and has not been paid–with an infuriating lack of transparency. Yet is being “invested” by The MLC, Inc. with less transparency than many banks with smaller net assets.

This “investment” is another result of the compulsory license which has no transparency requirements for such “investments” of other peoples’ money, perhaps “invested” in the very Big Tech companies that fund the The MLC, Inc. That wasn’t a question that was on the minds of Congress in 1909 but it should be today.

Attention Must Be Paid

Let’s face facts. The compulsory license has coexisted in the decimation of songwriting as a profession. That destruction has increased at an increasing rate roughly coincident with the time the Big Tech discovered Section 115 and sent their legions of lawyers to the Copyright Royalty Board to grind down publishers, and very successfully. That success is in large part due to the very mismatch that the compulsory license was designed to prevent back in 1909 except stood on its head waiting for loophole seekers to notice the potential arbitrage opportunity.

The Phonorecords III and IV proceedings at the Copyright Royalty Board tell Congress all they need to know about how the game is played today and how it has changed since 1909, or the 1976 revision of the Copyright Act for that matter. The compulsory license is no longer fit for purpose and songwriters should have a say in whether it is to be continued or abandoned.

We see the Writers Guild striking and SAG-AFTRA taking a strike authorization vote. When was the last time any songwriters voted on their compensation? Maybe never? Voting, hmm. There’s a concept. Now where have I heard that before?

MRA asks a good question. There's nearly half a billion in songwriter "black box" money sitting at the Music Licensing Collective. What do they have it invested in? Unlike foreign songwriter rights societies, the US MLC doesn't have to disclose this. https://t.co/z5Co2VSfv0

Well, another quarter is rolling around and the MLC is still sitting on 100s of millions of dollars of songwriter money as far as I can tell. Billboard says the MLC has “matched”–maybe different than “paid”–$200 million of the $427 million in black box that it was paid by the services in 2021. This doesn’t count the unmatched that the MLC has itself added to that sum. And Congress still haven’t required them to disclose their investment policy, returns on investment or much of anything else.

Compare the MLC to community banks. There are approximately 1,000 community banks with net assets between $250,00,000 to $500,000,000. There are approximately another 1,200 community banks with net assets between $100,000,000 to $250,000,000. It’s admittedly rough justice, but why should one entity holding hundreds of millions of other peoples’ money have virtually no disclosure requirements and be essentially unregulated while another is the opposite?

Remember that the MLC is supposed to pay interest “at the Federal, short-term rate” “for the benefit of copyright owners entitled to payment of such accrued royalties.” Note that the Federal short-term rate is today a lot higher than it was when the lobbyists wrote the Music Modernization Act, currently 4.21% or thereabouts. And through the power of compound interest, that’s a bunch of cash the MLC is supposed to come up with. I wonder where they’ll get it from. Wouldn’t you like to know?

Anyway, let’s talk about interest rates. The “risk free rate” is often thought of as the rate of interest paid on US government bonds. That interest rate is thought of as risk free because it is backed by the full faith and credit of the United States that you hear so much about these days. Want to know where you can find that full faith and credit? Look in the mirror.

When you ask around about what collective management organizations do with their “black box” monies while they are waiting to match money with songwriters or at least copyright owners, you often hear that the money is invested in very safe instruments, like U.S. treasury bonds. This might be particularly true of CMOs that are required to pay interest on black box because that interest has to come from somewhere.

But–and here it is–but, as we have learned from the Silicon Valley Bank collapse and the number of federal government officials in the mumble tank about why these banks are failing and why they are getting bailed out by, you know, the full faith and credit of the United States, “risk free” seems to be a relative concept. When you buy US government bonds, there are a number of different maturity dates available to you, kind of like buying a certificate of deposit. A common maturity date is the 10-year bond and the two-year bond, both of which were recently down sharply.

But–there is a connection between the interest rate that the bond pays, the price of the bond, and the maturity date of that bond. When bond interest rates increase, the face price tends to decrease. So if you paid $100 for a bond with a interest rate of say .08% and that rate then increased to say 4.5%, the face price of that bond will no longer be $100, it will be less. If that increase happens fairly quickly, you can have difficulty finding a buyer. The good news is that when the Federal Reserve raises the interest rate, there is about as much news coverage of the event as it is theoretically possible to have, both before during and after the rate increase, not to mention the Federal Reserve chair testifying to Congress. It’s very public. Closely watched doesn’t really capture that level of attention.

When bond prices decline, holders only “realize” the loss or gain if they sell the bond unless the bond is marked to market so the firm has to disclose the amount of what the loss would be if they sold the bond. Hence the concept of “unrealized losses,” “maturity risk,” or “interest rate risk.” Some think that US banks currently have $620 billion in unrealized losses due to interest rate risk. And don’t forget, these are your betters. These are the smart people. These are the city fellers.

This interest rate risk issue is not limited to banks, however. It is also present anytime that an entity tasked with caring for other people’s money invests that money in treasury bonds, crypto, or whatever. Like the MLC. You don’t have to be Wall Street Bets to end up losing your shirt or something in this environment.

So the point is that the same problem of interest rate risk and unrealized losses could apply to CMOs, such as The MLC, Inc. because of their undisclosed “investment policy” of investing the $424 million of black box they were paid by the services. They don’t disclose what the investment policy is and they don’t disclose their holdings so we don’t really know what has happened, if anything. The money could be perfectly safe.

We knew this would happen. The Copyright Office has empowered the Mechanical Licensing Collective to decide whether a song (or a sound recording) can be copyrighted all under the guise of AI. If the MLC–not the Copyright Office–decides that your song is not capable of being registered for copyright, the MLC can hold your money essentially forever.

Where’s the regulation on this important subject? Did you get a chance to comment on these crucial regulations and precedent?

Ah…no. You didn’t miss any notices in the Federal Register. No, we know this because of this cozy “guidance letter” to MLC CEO Kris Ahrend from the general counsel of the Copyright Office. That’s right, a letter that we just happened to run across. That letter states:

More specifically, the Office advises that a work that appears to lack sufficient human authorship is appropriately treated by The MLC as an “anomal[y],” consistent with its Guidelines for Adjustments, and The MLC should “place [associated] Royalties in Suspense while it researches and analyzes the issue.” Such research could include corresponding with the individual or entity claiming ownership of the work or [could include] inquiring whether the Office has registered the work and whether there are any disclaimers or notes in the registration record.

If The MLC subsequently concludes that the work qualifies for copyright protection and the section 115 license, it should distribute any royalties and interest in suspense to the copyright owner. Alternatively, if The MLC believes that the work does not qualify for copyright protection following its research and analysis, it should notify the individual or entity claiming ownership of the work of its determination and that associated royalties will be subject to an adjustment. This conclusion and adjustment may be challenged by initiating an “Adjustment Dispute” consistent with The MLC’s policies. If legal proceedings are initiated to challenge The MLC’s actions, the disputed royalties and interest should remain suspended until those proceedings are resolved.

So just in one paragraph, the Copyright Office has effectively delegated its role in the U.S. government to a private corporation controlled by the largest music publishers and financed by the largest tech companies in the world (actually the largest corporations in the history of commerce). If the MLC decides that your song “appears to lack sufficient human authorship” The MLC can hold your money while they research the issue.

Note this doesn’t say who makes that decision, it doesn’t say when they have to notify you, it doesn’t say they have to give you an opportunity to be heard, it places no timeline on how long all this may take. “The MLC” (whoever that is) could sit on your money for years without ever telling you they are doing it and also keep invoicing the DSPs for your royalties while they “research and analyze the issue”.

The only time they have to give you notice if they “believe” (whatever that means) “that the work does not qualify for copyright protection” then “it should” (not the mandatory “shall”, but the permissive “should”) notify you of that determination. You can then file an “adjustment dispute” based on the MLC’s own guidelines which you will not be surprised to learn places no disclosure obligations on them, imposes no timeline and cannot be appealed.

Note that this guidance from the Copyright Office pretty expressly contemplates that the MLC may dispute a work that has already been registered for copyright without qualification–which raises the question of what a copyright registration actually means, and where is it written that the MLC has the authority to challenge a conformed Copyright Office registration.

It also places the MLC in a superior position to the Copyright Office because it allows the MLC to initiate a dispute resolution system outside of the Copyright Office channels. Is this written somewhere besides a burning bush on Mount Horeb?

The letter does seem to suggest that you can always sue the MLC or that the MLC could be prosecuted for state law crimes, perhaps, like conversion, but it would help to know who at the MLC is actually responsible.

This also raises the question of why the MLC is invoicing the DSPs in the first place and what happens to the money every step along the path. Because of the idiotic streaming mechanical royalty calculation, it seems inevitable that the royalty pool will be overstated or understated if the MLC is claiming works that are not subject to copyright (like it would for public domain works it invoiced).

Ever wonder what prompts letters like this to get written?

The Mechanical Licensing Collective, Inc. published its tax return for 2021 so you could have a look at the salaries of all those people who can’t manage to pay out the hundreds of millions in black box money to songwriters. Did the Copyright Office approve these nauseatingly rich salaries? We’re not going to point out the disparities in this little list but…. We can’t help but wonder how many songwriters make anything like these salaries?

Suzanne Wilson General Counsel and Associate Register of Copyrights U.S. Copyright Office 101 Independence Avenue S.E. Washington D.C. 20559 Re: Notice of Proposed Rulemaking: Termination Rights and the Music Modernization Act’s Blanket License Docket No. 2022-5 Comment

Dear General Counsel Wilson:

Thank you for the opportunity to make this comment on the docket referenced above.[i]

I am a music lawyer in Austin, Texas and write this comment on my own behalf only and not on behalf of anyone else.

Others will address the substantive termination issues that are well-described and assayed in the Notice, so I will focus on the procedural tension between The Mechanical Licensing Collective, Inc. (“The MLC, Inc.”) currently designated as the mechanical licensing collective (“MLC”), its officers and directors, and the law as described in the Notice.

I argue that the need for this Notice is symptomatic of a larger problem in the relationship between Congress and The MLC, Inc. I hope the Office will consider resolving this tension as it has been authorized to do under the Music Modernization Act[ii] such as through regulations establishing the type of code of conduct that is common for other federal contractors.

This tension is alarming. The Notice states the MLC “does not follow the Office’s rulemaking guidance”[iii] regarding terminations, and that The MLC, Inc. “declin[es] to heed the Office’s warning….”[iv] These disclosures are diametrically at odds with the clear intent of Congress in crafting the MLC’s role.[v]

The disclosures confirm clearly that there are governance and oversight controversies at The MLC, Inc. that in my view need to be conclusively disposed of, and quickly.[vi] These governance issues are symptomatic of what may be much greater problems with the administrative capabilities of The MLC, Inc. that may be metastasizing but have not yet risen to the level of a public inquiry.

The recklessness that gives rise to the Notice also highlights The MLC, Inc.’s general lack of accountability and suggests a conscious disregard for the Copyright Office’s oversight role on a significant matter of law that is not capable of proper resolution through any “business rules.”[vii]

I also note this troubling statement in the Notice:

But, having reviewed the MLC’s policy, the Office is concerned that it conflicts with the MMA, which requires that the MLC’s dispute policies ‘‘shall not affect any legal or equitable rights or remedies available to any copyright owner or songwriter concerning ownership of, and entitlement to royalties for, a musical work.’’[viii]

It seems clear that The MLC, Inc.’s conscious failure to comply with Congressional intent as well as the Office’s guidance is, or ought to be, a decision of some import that surely must have been taken by someone—that is, one or more persons—employed or appointed by the MLC. It seems likely to be a subject that would have been reviewed both by its General Counsel and as part of the millions in outside counsel fees[ix] spent by The MLC, Inc.

The fact that the decision-making process is not readily known is itself of concern and leads one to further consider developing a code of conduct for The MLC, Inc. to assure the Office, the Congress and the public of its administrative capabilities.

Respectfully, I request that you determine how this decision was arrived at and what internal controls The MLC, Inc. has put in place to assure the Congress, the Office and interested parties that these mistakes will not happen again. This should not be an “oh well” moment and should be taken seriously by The MLC, Inc.

If The MLC, Inc. fails to disclose what it is doing by establishing opaque “business rules”, it is essentially creating de facto regulations that have the practical effect of law or regulations made behind closed doors unless the Office or other oversight agency happens to catch them out. The public will never know that the business rule was established, how the “business rule” was arrived at, or have a meaningful opportunity to comment such as in response to this Notice.

For example, do the minutes of The MLC, Inc.’s board of directors or statutory committees reflect a discussion or vote on the adoption of the MLC’s policies on termination treatment? Did such a vote implicate any conflicts of interest? Who determined that there was or was not a conflict of interest in the MLC’s decision to adopt the termination policy, however it was taken? Were there any dissenting votes recorded? Did an officer or director of The MLC, Inc. certify the completeness of the record in these findings in the corporate minute book?

This leads to other concerns under public discussion regarding the hundreds of millions of “black box” monies being held by The MLC, Inc. Given that the public has very little information available to it regarding the results and implications of the MLC’s operational decisions, I respectfully request that you determine what, if any, financial implications have arisen as a result of The MLC, Inc.’s reckless failure to comply with the law and the guidance of the Office in implementing its termination policy. Such determination should likely include any funds[x] that The MLC, Inc. is apparently trading in the market for its own account.[xi] Any curative action required by the Office should, of course, be retroactive in scope which will require considerable before-and-after accounting disclosures.

It must be asked whether the “business rule” established for terminations increases or decreases the enormous black box which was of considerable interest to Chairman Leahy at the recent Copyright Office oversight hearing at which the Register testified.[xii] This is particularly true if the implementation of the business rule results in financial harm to interested parties who rely on The MLC, Inc. to get it right.

The subject of black box came up in the Questions for the Record from Chairman Leahy. The Copyright Office’s response to Chairman Leahy’s inquiry about the hundreds of millions in black box held by the MLC directed the Chairman to the MLC’s annual report for answers.

Respectfully, I find this odd. Chairman Leahy did not ask what the MLC told the world in its annual report; rather he asked, “What can the Copyright Office do to help ensure that the MLC is working to make sure that rightful owners of music works are identified and paid?”[xiii]The question is transitive: We have oversight of you, you have oversight of The MLC, Inc., therefore we have oversight of the MLC.

Surely no one is surprised by this. The question many have is why The MLC, Inc. itself—a quasigovernmental organization operated by inferior officers[xiv] of the United States–is not the subject of an oversight hearing at Senate Judiciary regarding the hundreds of millions it is sitting on. Maybe next time.

It must also be said that the answer to Chairman Leahy goes on:

Notably, the MLC plans to wait to process historical unmatched royalties from the Phonorecords III rate period [2018-2022] until the Copyright Royalty Judges finalize those rates in the ongoing remand proceeding and digital music providers provide adjusted reports of usage and royalty payments. It is the Office’s understanding that the bulk of historical unmatched royalties come from that period.[xv]

Without getting into the timeline of what came when, how is it exactly that The MLC, Inc. took the decision in February 2021—nearly two years ago–to sit on top of hundreds of millions of other peoples’ money that they were somehow investing under their undisclosed “Investment Policy”? Was anyone asked? Who gave the MLC the permission to do this? Do they not hold the black box corpus in trust for songwriters and copyright owners yet to be identified? Does this not compound the already painful series of failures that resulted in the black box in the first place, the delay in accounting to songwriters (or their families) under Phonorecords III remand, and still more delay while legions of lobbyists and lawyers argue over the post-remand true up accountings?

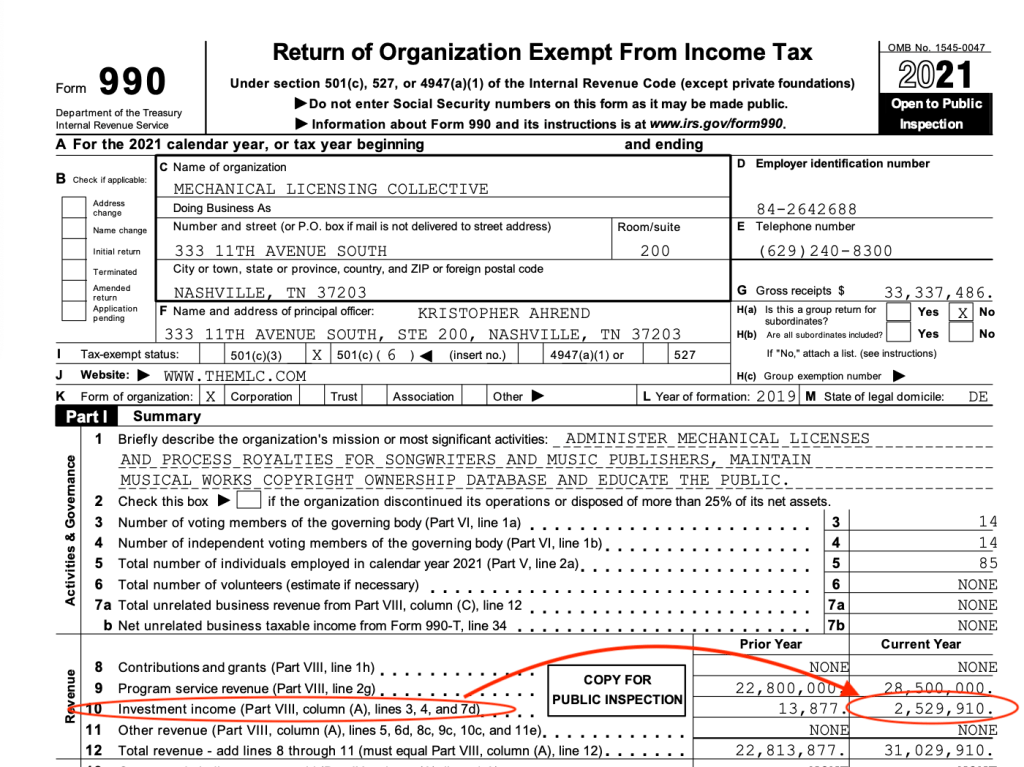

The MLC reported $2,529,910 investment income on its 2021 US Federal tax return 990

Respectfully, there is also, of course, a larger question that the Office may consider answering: If The MLC, Inc. adopts a policy or takes some action outside of the law or its remit, is that policy binding on any future entities designated by the Office as the MLC?

These are all questions that I would expect to have answers that are readily available to the public given that The MLC, Inc. is in a position of public trust administering a compulsory license on behalf of the United States and has been given great privileges under the MMA.[xvi]

Thank you again for the opportunity to comment.

Very truly yours,

Christian L. Castle

CLC/ko

[i] U.S. Copyright Office, Notice of Proposed Rulemaking, Termination Rights and the Music Modernization Act’s Blanket License 87 FR 64405 (Oct. 25, 2022) (Doc. No. 2022-5) (hereafter “Notice”).

[ii]Orrin G. Hatch-Bob Goodlatte Music Modernization Act, Public Law 115–264, 132 Stat. 3676 (2018) (“MMA”) and specifically Title I thereof.

[v]See S. Rep. 115-339 (115th Cong. 2nd Sess. Sept. 17, 2018) at 7 (“Senate Report”). (“The collective is expected to operate in a transparent and accountable manner.”)

[vi] I would hope that this failure will be weighed and measured by the Copyright Office as part of The MLC, Inc.’s quinquennial review as is required under the legislative history. See, e.g., Senate Report at 5 (“[E]vidence of fraud, waste, or abuse, including the failure to follow the relevant regulations adopted by the Copyright Office, over the prior five years should raise serious concerns within the Copyright Office as to whether that same entity has the administrative capabilities necessary to perform the required functions of the collective.”)(emphasis added).

[vii] It must be said that the MLC’s disregard for this particular matter may present a moral hazard (at best) for the publishers represented by at least some of its board members.

[x]See the MLC’s annual report stating that the MLC invests the black box according to its internal “Investment Policy” established by its board of directors but not made public. MLC 2021 Annual Report at p. 4 available at https://www.themlc.com/hubfs/Marketing/23856%20The%20MLC%20AR2021%206-30%20REFRESH%20COMBINED.pdf(“Annual Report”) (“Investment Policy: This policy covers the investment of royalty and assessment funds, respectively, and sets forth The MLC’s goals and objectives in establishing policies to implement The MLC’s investment strategy. The anti-comingling policy required by 17 U.S.C. § 115(d)(3)(D)(ix)(I)(cc) is contained in [The MLC, Inc.’s] Investment Policy. The Investment Policy was approved by the Board in January 2021.”) (emphasis added).

[xi] Realize that every CMO is confronted with the decision about what to do with the royalty float and black box, but not every CMO decides to invest these funds in the market. If they do invest the funds, it is generally the case that any trading profits, dividends or interest goes to offset the CMO’s administrative costs that otherwise would be deducted from collected royalties. However, the MLC, Inc.’s administrative costs are paid by the users of the blanket license (making the United States, I believe, the only country in history or the world that charges for the use of a statutory license). Therefore, the return on the MLC’s investment of the songwriters’ money would not be used for the same purpose as all the world’s CMOs that follow a similar practice. The continuity in ownership for profits derived from The MLC, Inc.’s trading is also unclear; if The MLC, Inc.’s existing designation is not continued but securities are being held or profits generated, what happens?

[xii]Senate Judiciary Committee, Subcommittee on Intellectual Property, Oversight of the U.S. Copyright Office, Responses to Questions for the Record by Shira Perlmutter, Register of Copyrights and Director of the Copyright Office (Sept. 7, 2022), available at https://artistrightswatchdotcom.files.wordpress.com/2022/10/qfr-responses-perlmutter-2022-09-07.pdf. (“Questions for the Record”) (“With respect to the historical, pre-2021, unmatched royalties, which were reported to be about $426 million, the annual report says that the MLC recently started distributing those that it has been able to match. It also says that the MLC has begun making associated usage data for historical unmatched royalties available to copyright owners, which will facilitate further claiming and matching.”)

[xiv] President Donald J. Trump, Statement on Signing the Orrin G. Hatch-Bob Goodlatte Music Modernization Act (October 11, 2018) available athttps://www.govinfo.gov/content/pkg/DCPD-201800692/pdf/DCPD-201800692.pdf (“Because the directors are inferior officers under the Appointments Clause of the Constitution, the Librarian must approve each subsequent selection of a new director.”)

[xvi]See, e.g., Senate Report at 5 (emphasis added). “For the responsibilities described in subparagraphs (J) [distribution of unclaimed royalties] and (K) [dispute resolution] of paragraph (3), the collective is only liable to a party for its actions if the collective is grossly negligent in carrying out the policies and procedures adopted by the Board of Directors pursuant to section 115(d)(11)(D). Since the Register has broad regulatory authority under paragraph (12) of subsection (d), it is expected that such policies and procedures will be thoroughly reviewed by the Register to ensure the fair treatment of interested parties in such proceedings given the high bar in seeking redress.”

In this comment to the Copyright Office, Abby North (independent publisher and Artist Rights Symposium III Moderator) calls on the Copyright Office to stop the MLC quango from unilaterally establishing “business rules” that hurt songwriters and their heirs and protect working families from these arbitrary actions of The MLC. The passing of Jeff Beck reminds us once again that we must take care to protect the heirs of creators.

Re: Termination Rights and the Music Modernization Act’s Blanket License

To the United States Copyright Office:

My name is Abby North. I am a music publishing administrator based in Los Angeles. My views expressed in this letter are solely my own.

With my husband, I am a copyright owner of the classic song “Unchained Melody,” among other copyrights. I also administer musical works and sound recordings on behalf of songwriters, their families and heirs. In many instances, I assist my clients in identifying their termination windows, assist in the research required, and interface with the attorneys who process termination filings.

Abby North, Helienne Lindvall, Erin McAnaly, Melanie Santa Rosa speaking at UGA Artist Rights Symposium III (Nov. 15, 2022 in Athens, GA)

I’m thankful for the opportunity to submit comments in support of the Copyright Office’s proposed rule.

The ability to recapture rights via the United States copyright termination system truly provides composers, songwriters and recording artists and their heirs, a “second bite of the apple.” Many of my clients exercise this right, and in doing so grow their family’s revenue, which, given today’s inflation and very high interest rates, coupled with a depleted stock market, is absolutely necessary.

Allyn Ferguson was a successful composer of film/television scores including “Little Lord Fauntleroy,” “Les Miserables,” “Charlie’s Angels,” and “Barney Miller.” According to Variety in its June 27, 2010 obituary, Ferguson was “among the most prolific composers of TV in the past 40 years.” My company North Music Group administers works controlled by Ferguson’s family.

In addition to his scores, Ferguson wrote songs performed by artists including Johnny Mathis, Count Basie Band and Freddie Hubbard. While the bulk of his film and television scores were created on a work for hire basis, and therefore are not eligible for termination under US copyright law, Ferguson’s commercial compositions and songs were not created as works for hire. Ferguson’s family has been able to exercise its termination rights in various musical works,

thereby increasing its earnings as it now collects the publisher share of United States royalties generated by the terminated works. Individual songwriters and composers and their heirs are not copyright aggregators. Every musical work, and every penny generated is very necessary to these families.

The Music Modernization Act created the blanket digital mechanical license. This move from one-off copyright licenses to a blanket license was a dramatic improvement in US mechanical licensing. However, the suggestion that rights held at the inception of this blanket license might remain, in perpetuity, with the original copyright grantee was frightening. I concur with the Office’s proposed rule and legal analysis of the relevant statutes and authorities.

I appreciate the Office requesting comments on the mechanics of solving the payment issues, because for the independent publishers I speak with and for me personally, many operational questions arise regularly regarding The MLC’s uncharted territories.

As one of The MLC’s statutory goals is to provide transparency to songwriters and copyrightowners, I would ask that the Office require The MLC to notify copyright owners (1) if The MLC’s unilateral termination policy has already been imposed on payments previously paid or that are being held in the historical or current black box, and (2) when the adjusting payment required by the proposed rule had been made.

To be clear, this rule must absolutely be retroactive to inception date of The MLC. Beyond the simple, clarifying amendment to the MMA, I believe there are additional, related issues that must be resolved:

1) What is The MLC’s “business rule” regarding the MLC/HFA Song Code for the terminated work? Prior to the inception of The MLC, the Harry Fox Agency would assign one HFA Song Code fr the work and its pre-termination parties, and a different HFA Song Code for the work with the post-termination parties.

What happens now? Do these multiple HFA Song Codes remain in The MLC’s database? Will there continue to be two separate MLC/HFA Song Codes, particularly given the Harry Fox Agency continues to license physical and download mechanicals on behalf of many publishers? Is it reasonable for the HFA Song Code to be the same as The MLC Song Code, when there is no derivative works exception in Section 115?

2) Which party is entitled to the Unmatched (Black Box) royalties, the related interest fees and to The MLC’s investment proceeds for a terminated work?

Finally, it should be noted that the initial concept proposed by The MLC Board (that the server fixation date should impact termination dates) most likely would have served large publishers, not songwriters.

It is crucial that the Copyright Office exercise vigilant oversight and governance of The MLC’s reporting regarding any payment obligations to copyright owners. Specifically, composers, songwriters and their heirs must have as significant a voice as the largest publishers and copyright aggregators.

Additionally, in the spirit of full transparency, I request full disclosure of board or committee votes, minutes of meetings or other documentation of process. For me and others like me, this would tremendously enhance our understanding of The MLC.

Decisions are being made by The MLC’s board and committee members, while the general MLC member or songwriters have no mechanism to gain information regarding the discussions, the decisions and the implementations thereof. Access to minutes and notes would provide valuable insights to the general membership.

I applaud the Copyright Office for moving swiftly to create this rule and clarify and codify how The MLC must treat copyright terminations. It is important that this rule be dictated by the Office as it is absolutely not The MLC’s job todecide who controls rights and is entitled to collect royalties.

That said, a “business rule” established by The MLC could have the effect of law absent vigilance by the Copyright Office.

On behalf of my family and clients, I wholeheartedly support this proposed regulation, and I truly appreciate the Copyright Office’s consideration of my comments.

You must be logged in to post a comment.