Remember how the physical mechanical increased from 9.1¢ to 12¢? And it applies to each record sold? If a songwriter got a cut and the artist sold 100 records, the songwriter got $12. That’s $12 today, next month, six months from now. You could plan. You could complain about a statement to the record company. If the record company wanted you to write more songs for their artists, they’d listen and might even fix an error on your statement. Remember: On records and downloads, the record companies pay.

But what about streaming? The record companies don’t pay on streaming, Big Tech pays. The biggest corporations in the world pay: Spotify, Amazon, Apple, Google, Pandora, and their dozens of lawyers. Artist Rights Watch posted a series of Tweets that shows excerpts from the proposed regulations to calculate streaming royalties–and remember this is the one that we’re told is the important one, the one that dozens of lawyers spend millions in legal fees to come up with. It reads kind of like a drunk you can smell a block away but who sits down next do you and asks how do they look for three days?

The first think you realize is that unlike the 12¢ rate for physical, there’s no way anyone call tell a songwriter how much they’re going to make today or next year on a per play. They can’t even tell you how much you’re going to make today for a burger next Tuesday. Or Wednesday. Or Thursday. But one thing you definitely know is that the lawyers are going to make bank writing this crap, appealing this crap, renegotiating this crap. This section here is a big part of what the fight is all about, can you believe it? This is what the Big Boys and Girls think is important and you can understand why. It puts more legal fees on the table and you know who eventually pays for the legal fees one way or another? Take a look in the mirror.

And understand this: If you get a royalty statement for streaming royalties, take a look at the per-stream rate! It usually starts three or four or even five zeros to the right of the decimal place. It’s even worse than the recording royalty. And DIMA wants us to fight among ourselves against the record companies after all this?

In case you were wondering what an utter shitshow streaming mechanicals have become thanks to the dozens of lawyers and lobbyists getting rich from making it complicated–compare this to 12¢ a unit. This calculation gets made EVERY MONTH. https://t.co/rLwsCn5jVJpic.twitter.com/vLa8KgqVrc

It’s always been a hard road for musicians to make money from their songs. Nonetheless, selling tons of singles and albums was at least a target and something bands could dream about. Of course, there were many ways the labels could work the sales figures to get their shares out first, and only then the bands might see something. Despite the conflict between the often industrial-strength labels and the upcoming artists, there was at least hope that money was flowing back to the content creators. Now though in the age of streaming music, the connection between making music and making a living is profoundly broken.

This schism is the subject matter for Lightbringer Production’s documentary film “The Way The Music Died” featuring insights from musicians and industry pros, including Mishkin Fitzgerald from Birdeatsbaby. The film probes the spirit of artists determined to keep writing songs in the face of the meager payouts from the giant and ever-growing music stream service Spotify. Find out why this is ripping-out the heart and soul of new music.

Getting discovered in the music business has never been easy. Before the pandemic, artists could at least rely on the industry’s historic mainstay to break through — playing as many gigs as possible and hoping to build a following. But with that path closed for now, artists and their label partners are increasingly dependent on Spotify, the undisputed king of music streaming, and its black box algorithms.

That’s why Spotify’s cynical decision to use this moment to launch a new pay-for-play scheme pressuring vulnerable artists and smaller labels to accept lower royalties in exchange for a boost on the company’s algorithms is so exploitative and unfair. Artists must unite to condemn this thinly disguised royalty cut, which apparently has just been released in “beta” mode and is soon expected to enter the market in full force.

If you’ve tried to get a vinyl record pressed in the last few years, one thing is very obvious: There is no capacity in the current manufacturing base to accommodate all the orders–unless your name is Adele or Taylor Swift, of course. If that’s your name, as if by magic you get your vinyl orders filled and shipped on time.

Jack White spotted the vinyl trend early on–in 2009–and is filling the gap through his Third Man pressing operations. But Jack is calling on the major labels to please compete with him–rather unusual–because it’s the right thing to do in order to meet the demand for the benefit of the consumer. And the elephant in the room of this discussion is that we don’t really have any idea what the vinyl sales would be because demand is not being met by supply.

Not even close.

When a major label abandons a configuration, it’s not really abandoned. It gets outsourced to an independent and as long as there is manufacturing capacity in the system, that independent still takes orders and fulfills those orders by using that manufacturing capacity. The titles still appear in the sales book, orders get taken and returns accommodated.

Major labels also hand off vinyl manufacturing to their “special markets” divisions. For example, if you have ever tried to get vinyl manufactured in a limited run for venue sales on a major label artist (or former major label artist) you will get put through the bureaucratic torture gauntlet for the privilege of paying top dollar on a product that the label will have nothing to do with selling.

But even so, at some point that manufacturing capacity begins to shrink because the majors are getting out of the configuration and they will eventually get out of the manufacturing business altogether. And that creates a great sucking sound as capacity tanks.

I raised this problem in comments to the Copyright Royalty Board about the frozen mechanicals debacle where the smart people have tried to extend the 2006 songwriter rates on vinyl and CDs without regard to rampant inflation and simply the value of songs to sell millions of units. Why? Because vinyl and CDs don’t matter according to the lobbyists. This is, of course, bunk.

The fact is–and Jack White’s plea illuminates the issue–we don’t know what the sales would be if the capacity increased to meet demand. But we do know that sales would be higher. Probably much higher.

You do see entrepreneurs entering the space using new technology. Gold Rush Vinyl in Austin is a prime example of that phenomenon. The majors need to reconsider how to meet demand and keep the consumer happy. They also need to clean up the sales and distribution channel so that it’s easy for record stores to actually get stock, which, frankly is a joke.

Why anyone wants to substitute away from high margin physical goods to low margin streaming goods with a “rich get richer” financial model is a head scratcher. Although maybe I answered my own question.

But–as Trichordist readers will recall, the major publishers and major labels as well as the Nashville Songwriters Association are trying to convince the Copyright Royalty Board that vinyl and CDs are not important and that songwriters should have their mechanical royalty rates frozen again. You do have to ask if Jack White is even aware that the major publishers and major labels are trying to get the Copyright Royalty Board to extend the 2006 freeze on mechanicals for the resurgent vinyl configuration for another five years.

Vinyl and CDs still account for about 15% of revenue on an industry wide basis–I’ll believe that it’s not significant when Lucian Grange says he doesn’t need 15% of billing. Yeah, that will happen.

The only reason that mechanicals for those configurations aren’t higher is because they have been artificially suppressed by the participants at the Copyright Royalty Board telling the judges that the revenue is low so please freeze the rates again. Kind of circular, yes? The current 2006 rate of 9.1¢ would be adjusted to 13¢ in current dollars just taking into account inflation and ignoring the value of the songs to create a nearly vertical chart like this:

As we reported February 9, Spotify is using hundreds of millions of its supernormal stock market riches to acquire naming rights to the Barcelona soccer team. The latest manifestation of Daniel Ek’s monopolist edifice complex was confirmed by Music Business World Wide and Variety among others, as well as Spotify itself. Barcelona’s iconic Camp Nou stadium (largest football stadium in Europe) will now be known as Spotify Camp Nou.

I assume that when Netflix finds out about this, there will be an epilogue to their Edward Bernays-style epic corporate biopic that will ignore the Rogan catastrophe but will include the Barcelona deal with a tight shot on the Spotify Camp Nou and probably a t-shirt vendor.

Let us take one clear message from this navel-gazing naming-rights deal to assuage Daniel Ek’s psyche after a losing bid to acquire the Arsenal football club and join the International League of Oligarchs. That message is that we don’t ever want to hear again about how Spotify “can’t make a profit” or “pays out too much money for music.” Daniel Ek–who controls the company through his super voting stock–has been running that diversion play for way too long and it’s just as much BS spewing from his mouth as it is any of the Silicon Valley oligarchs who whinge about how poor they are when they appear in court.

Let us also agree that anyone who takes a royalty deal from any DSP that does not include an allocation for stock valuation is quite simply a rube who must be laughed at and mocked in the Spotify board room. This stock value allocation doesn’t require a grant of shares, but can include a dollar contribution that tracks share value and should be paid directly to both featured artists, session musicians and vocalists through their collective rights organizations on a nonrecoupment basis.

But don’t let me describe the bullshit, read it yourself directly from Spotify’s “Chief Freemium Business Officer” whatever the hell that means:

Statement of Alex Norström, Chief Freemium Business Officer, Spotify

“We could not be more thrilled to be partnering with FC Barcelona to bring the worlds of Music and Football together. From July, our collaboration will offer a global stage to Artists, Players and Fans at the newly-branded Spotify Camp Nou. We have always used our marketing investment to amplify Artists and this partnership will take this approach to a new scale. We’re excited to create new opportunities to connect with FC Barcelona’s worldwide fanbase.

Spotify’s mission is to unlock the potential of human creativity, supporting artists to make a living off their art and connecting with fans. We believe this partnership creates many opportunities to deliver on this mission in unique, imaginative, and impactful ways.”

Yes, that’s right. Daniel Ek’s edifice complex is all about unlocking the potential of human creativity because it’s all for the artists, don’t you know.

These people continue to embarrass themselves with their insufferable 1999er BS without realizing that any artist whose name shows up on a single Barcelona jersey will extract a considerable additional payment that the artist will keep and the labels won’t save Spotify on that one. Even if they do, there are only certain artists who don’t mind their names appearing on Barcelona jerseys–for a price. The overwhelming majority will not only not want it but are insulted that the “Chief Freemium Business Officer” is so ignorant of their name and likeness rights that he would even remotely float the idea that Spotify had the right to do anything like that level of grift.

If Mr. Freemium is really serious about “supporting artists to make a living off their art”, forego the edifice stroke and just pay that money directly to featured artists, session folk, and songwriters that have made him rich. Until then, he should just say you’re damn right we used the stockholders money to soothe Daniel Ek’s wounded ego because he desperately wants to be accepted by the Party of Davos and the League of Extraordinary Dweebs. Because we’ve already established what kind of people they are, it’s just a question of negotiating the price.

But let’s face it–what the monopolist really wants is a branded Monopoly game.

Spotify has one big governance problem that permeates its governance like a putrid miasma in the abattoir: “Dual-class stock” sometimes referred to as “supervoting” stock. If you’ve never heard the term, buckle up. I wrote an extensive post on this subject for the New York Daily News that you may find interesting.

Dual class stock allows the holders of those shares–invariably the founders of the public company when it was a private company–to control all votes and control all board seats. Frequently this is accomplished by giving the founders a special class of stock that provides 10 votes for every share or something along those lines. The intention is to give the founders dead hand control over their startup in a kind of corporate reproductive right so that no one can interfere with their vision as envoys of innovation sent by the Gods of the Transhuman Singularity. You know, because technology.

Google was one of the first Silicon Valley startups to adopt this capitalization structure and it is consistent with the Silicon Valley venture capital investor belief in infitilism and the Peter Pan syndrome so that the little children may guide us. The problem is that supervoting stock is forever, well after the founders are bald and porky despite their at-home beach volleyball courts and warmed bidets.

Spotify, Facebook and Google each have a problem with “dual class” stock capitalizations. Because regulators allow these companies to operate with this structure favoring insiders, the already concentrated streaming music industry is largely controlled by Daniel Ek, Sergey Brin, Larry Page and Mark Zuckerberg. (While Amazon and Apple lack the dual class stock structure, Jeff Bezos has an outsized influence over both streaming and physical carriers. Apple’s influence is far more muted given their refusal to implement payola-driven algorithmic enterprise playlist placement for selection and rotation of music and their concentration on music playback hardware.)

The voting power of Ek, Brin, Page and Zuckerberg in their respective companies makes shareholder votes candidates for the least suspenseful events in commercial history. However, based on market share, Spotify essentially controls the music streaming business. Let’s consider some of the implications for competition of this disfavored capitalization technique.

Commissioner Robert Jackson, formerly of the U.S. Securities and Exchange Commission, summed up the problem:

“[D]ual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms [Snap, Inc. and Google Class B shares] have recently issued shares that give ordinary public investors no vote at all.

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression. But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.” Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.

Spotify is the dominant streaming firm and the voting power of Spotify stockholders is concentrated in two men: Daniel Ek and Martin Lorentzon. Transitively, those two men literally control the music streaming sector through their voting shares, are extending their horizontal reach into the rapidly consolidating podcasting business and aspire soon to enter the audiobooks vertical. Where do they get the money is a question on every artists lips after hearing the Spotify poormouthing and seeing their royalty statements.

The effects of that control may be subtle; for example, Spotify engages in multi-billion dollar stock buybacks and debt offerings, but has yet makes ever more spectacular losses while refusing to exercise pricing power.

So yes, Spotify is starting to look like the kind of Potemkin Village that investment bankers love because they see oodles of the one thing that matters: Fees.

On the political side, let’s see what the company’s campaign contributions tell us:

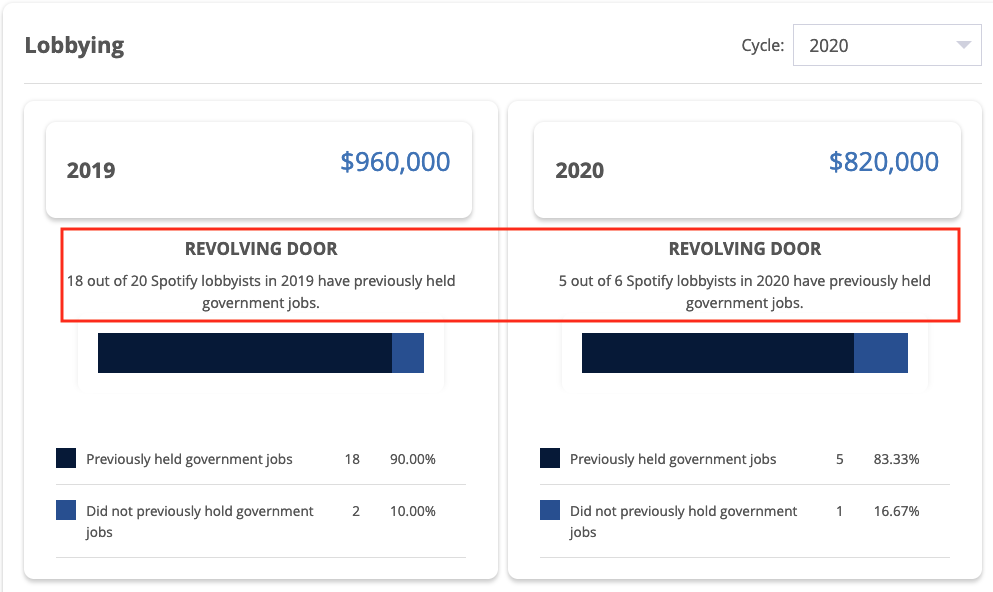

Spotify has also made a habit out of hiring away government regulators like Regan Smith, the former General Counsel and Associate Register of the US Copyright Office who joined Spotify as head of US public policy (a euphemism for bag person) after drafting all of the regulations for the Mechanical Licensing Collective;

Whether this is enough to trip Spotify up on the abuse of political contributions I don’t know, but the revolving door part certainly does call into question Spotify’s ethics.

It does seem that these are the kinds of facts that should be taken into account when determining Spotify’s ESG score. At this point, it looks like Spotify is an ESG fail–which may require divesting by some of the over 600 mutual funds that hold shares.

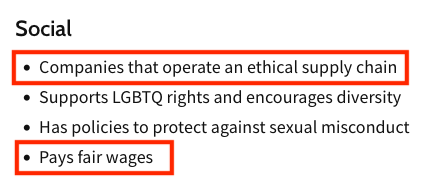

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective scam and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor? I think not.

[This is the first in a series of three short posts examining how Spotify scores as an Environmental, Social and Governance (or “ESG”) investment. “ESG” is a Wall Street acronym often attributed to Larry Fink at Blackrock that designates a company as suitable for socially conscious investing based on its “Environmental, Social and Governance” business practices, that is “ESG”. See the Upright Net Impact data model on Spotify’s sustainability score. As of this writing, the last update of Spotify’s Net Impact score was before the Neil Young scandal and, of course, rocketing energy prices that compound the environmental impact of streaming. These posts first appeared on MusicTechSolutions]

Spotify closes $24 higher than its first day of trading after destroying the incomes of thousands of artists and even more songwriters. pic.twitter.com/HeHXnEXVHh

Spotify has an ESG problem, and a closer look may offer insights into a wider problem in the tech industry as a whole. If a decade of destroying artist and songwriter revenues isn’t enough to get your attention, maybe the Neil Young and Joe Rogan imbroglio will. But a minute’s analysis shows you that Spotify was already an ESG fail well before Neil Young’s ultimatum.

Streaming is an Environmental Fail

I first began posting about streaming as an environmental fail years ago in the YouTube and Google world. Like so many other ways that the BIg Tech PR machine glosses over their dependence on cheap energy right through their supply chain from electric cars to cat videos, YouTube did not want to discuss the company as a climate disaster zone. To hear them tell it, YouTube, and indeed the entire Google megalopolis right down to the Google Street View surveillance team was powered by magic elves running on appropriate golden flywheels with suitable work rules. Or other culturally appropriate spin from Google’s ham handed PR teams.

Mission creepy meets the Sound of Music

Greenpeace first wrote about “dirty data” in 2011–the year Spotify launched in the US. Too bad Spotify ignored the warnings. Harvard Business Review also tells us that 2011 was a demarcation point for environmental issues at Microsoft following that Greenpeace report:

In 2011, Microsoft’s top environmental and sustainability executive, Rob Bernard, asked the company’s risk-assessment team to evaluate the firm’s exposure. It soon concluded that evolving carbon regulations and fluctuating energy costs and availability were significant sources of risk. In response, Microsoft formed a centralized senior energy team to address this newly elevated strategic issue and develop a comprehensive plan to mitigate risk. The team, comprising 14 experts in electricity markets, renewable energy, battery storage, and local generation (or “distributed energy”), was charged by corporate senior leadership with developing and executing the firm’s energy strategy. “Energy has become a C-suite issue,” Bernard says. “The CFO and president are now actively involved in our energy road map.”

If environment is a C-suite issue at Spotify, there’s no real evidence of it in Spotify’s annual report (but then there isn’t at the Mechanical Licensing Collective, either). “Environment” word search reveals that at Spotify, the environment is “economic”, “credit”, and above all “rapidly changing.” Not “dirty”–or “clean” for that matter.

The fact appears to be that Spotify isn’t doing anything special and nobody seems to want to talk about it. But wait, you say–what about the sainted Music Climate Pact? (Increasingly looking like a PR effort worthy of Edward Bernays.) Guess who hasn’t signed up to the MCP? Any streaming service as far as I can tell. There is a “Standard Commitment Letter” that participants are supposed to sign up to but I wasn’t able to read it. Want to guess why?

That’s right. You know who wants to know what you’re up to.

If you haven’t heard much about streaming’s negative effects on the environment, don’t be surprised. It’s not a topic that’s a great conversation starter and very few journalists seem to have any interest in the subject at all. I wonder why.

But if you’re an artist who is concerned about the impact of streaming your music on the environment or an investor trying to see your way through the ESG investment, this should give you a few questions to ask about Spotify’s ESG score. And if that slipped by you, don’t feel bad–Blackrock reportedly holds 3.8 million shares of Spotify that are worth less all the time, so they didn’t catch it either. And Blackrock coined the phrase.

Next: Spotify’s “Social” Fail: Rogan, Royalties and The Uyghurs

Remember the $424 million in historical unmatched royalties (also referred to as black box royalties) delivered to the Mechanical Licensing Collective (MLC) by the streaming services last February that songwriters are waiting to receive?

As a refresher, the Music Modernization Act (MMA) required the streaming services to estimate these “historical” black box royalties going back years, and then pay whatever they came up with to the MLC by February 15, 2021. Why did the services pay this “historical” black box? Because songwriters gave them a safe harbor in the MMA to enjoy a limitation of liability from statutory damages for the services’ prior acts of copyright infringement—services like Spotify, which was being sued into oblivion.

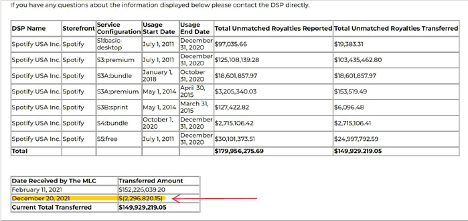

Now here’s the jawdropper. What if I told you that Spotify inexplicably reduced its portion of these historical unmatched royalties by nearly $2.3 million?

According to the MLC, on December 20, 2021 Spotify decreased its transfer of historical unmatched royalties by $2,296,820.15. You can find this information by visiting the MLC’s website here: https://www.themlc.com/spotify-usa-inc-spotify. You may wonder why this occurred. Unfortunately, I cannot provide you with any concrete answers, but I do think it is a more than fair question to raise.

Following the February 2021 data dump and transfer of the historical unmatched royalties to the MLC, the streaming services were given until June (in accordance with the regs) to provide the MLC with their second sets of data. According to the MLC’s Interim Annual Report (https://themlc.com/sites/default/files/2021-12/The%20MLC%20Interim%20AR21%20Hi-res%20FINAL.pdf) “[t]his second set of data contained information regarding works for which DSPs had previously paid some, but not all, of the relevant rightsholders for a given work.” The streaming services then had the right over the summer to amend or adjust the royalties and data provided to the MLC.

It is interesting to compare the historical unmatched royalties transferred by each streaming service in February 2021 with the final transfer amounts reported in summer 2021 — and I invite all of you to do the same (https://www.themlc.com/historical-unmatched-royalties ). What you will quickly realize is that the final transfer amounts for every service—other than Spotify, the Harry Fox Agency’s client, either reflected the same totals from the February dump, or, resulted in a higher amount transferred (like in the cases of Amazon, Apple and Google). At least so far.

You may be thinking, how do we know if this nearly $2.3 million reduction is accurate? Frankly, we do not know, and we forced to trust that Spotify is telling the truth. Regrettably, the MMA negotiators did not get (and may not have asked for) an audit right for songwriters or for the MLC with respect to these historical unmatched royalties. (Although it must be said that publishers with direct deals very likely had the right to audit, and possibly those who licensed to Spotify through Spotify’s licensing agent, the Harry Fox Agency, which was simultaneously acting as a licensors’ publishing administrator may have had an audit right. Have a pretzel and the conflicts make more sense).

I recognize I have the benefit of hindsight here — notwithstanding, I find it unfathomable that the MMA dealmakers did not secure an audit right in connection with what was sure to be hundreds of millions of dollars in unmatched royalties.

It is theoretically possible that Spotify overpaid its amount in historical unmatched royalties back in February 2021. Notwithstanding, and feel free to call me a cynic — how am I to believe that for once Spotify actually made an overpayment in royalties?

How can I trust a company which amassed its billions in wealth by stealing musicians’ works, and has continued to supplement its wealth by fighting for the lowest mechanical royalty rates for songwriters ever?

How can I trust a company that when faced with reasonable requests about paying musicians fairly, responded with a straight up gaslighting campaign? (see “Loud & Clear” campaign: https://loudandclear.byspotify.com/ )

Remember, this is the company whose executive literally told an independent artist the following in a public forum:

In sum, how can I trust a company that has proven time and time again from its inception that it has never cared about songwriters and artists? Ultimately, I cannot — which makes it utterly difficult for me to trust that Spotify incorrectly overpaid nearly $2.3 million in historical unmatched royalties to the MLC. Granted, if Spotify made misrepresentations here, it could lose its limitation of liability for those past infringements–after years of litigation. But, without the MLC having the right to audit the historical unmatched amounts, determining whether Spotify’s total transfer is correct is essentially futile.

Awesome.

So, if you happen to contact Spotify this week about removing your catalog or canceling your subscription, consider also asking them to provide evidence that they overpaid the MLC $2,296,820.15 in historical unmatched royalties last February. Maybe if we’re lucky, we’ll get another Loud & Clear gaslighting campaign to post about!

SECOND REOPENING PERIOD COMMENTS OF HELIENNE LINDVALL, DAVID LOWERY AND BLAKE MORGAN

Helienne Lindvall, David Lowery and Blake Morgan (collectively, the “Writers”) thank the Judges for the opportunity and respectfully submit the following comments responding to the Copyright Royalty Judges’ notice (“Second Notice”) soliciting comments on additional materials (“Reply”) received by the Judges[1] from the National Music Publishers Association, Nashville Songwriters Association International, Sony Music Entertainment, UMG Recordings, Inc. and Warner Music Group Corp. (collectively, the “Majors”)[2] regarding the so-called [frozen] “Subpart B” statutory rates and terms[3] relating to the making and distribution of physical or digital phonorecords of nondramatic musical works in the docket referenced above (“Proceeding”).

The Writers previously submitted comments[4] (“Prior Comment”) responding to the Judges’ notice[5] (“First Notice”) soliciting comments on the Major’s proposed purported settlement (the “Proposed Settlement”)[6] of the Subpart B rates. The Writers along with attorney Gwendolyn Seale[7] attempted to submit additional comments in response to the Majors’ filing but were not able to timely file that response.[8] The Writers appreciate the Judges’ decision to reopen the comment period in order to afford the public, and those that would be bound by the rates and terms set by the Proposed Settlement,[9] an opportunity to comment on those additional materials filed by the Majors and to further participate in the rulemaking.[10]

I. SUMMARY As a general comment on the record to date in Phonorecords IV, the Writers are mystified by the histrionics that have become associated with this Proceeding both on the record and in the press. A voluntary negotiation is just a deal, often made by people who are paid to always be closing. The Writers believe that Congress intended that voluntary negotiation produce a fair result on a reasonable timetable.

While not directly at issue in the reopened comment period, what is clearly the case is that the settlement of the Subpart B rates has unnecessarily become a major gating item for the streaming side of this Proceeding, geese and ganders being what they are. Despite the extensive voluntary negotiation period for the Subpart B rates by the Majors, the Judges—and, frankly, songwriters around the world–are presented instead with a cornucopia of chaos across the board; the cherry on top is the frozen mechanicals crisis. However, in this season of hope the Writers are confident that the Judges will lead us all out of this daunting situation.

The Writers are not interested in the personalities, the arm-waving or the finger-pointing. They are interested in the results, particularly because neither they nor anyone they authorized had input into the negotiation that produced either the Proposed Settlement or the impasse.

There is at least one easy way to fix this and recognize the intrinsic value of songs: Raise the statutory rate proposal for Subpart B configurations in at least some relation to the streaming rate increase. A song is no less valuable because of the medium in which it is exploited.[11]

As the Writers will argue, just like the voluntary agreement on Subpart B that led to this impasse was reached by the Majors, those same parties can go back to the drawing board to reach an appropriate conclusion with a higher Subpart B rate.

Neither the public nor the songwriters are well served (and frankly neither are the Judges) by thrashing about and waiving arms. This may serve well the people who are paid by the hour but it hasn’t served people who are paid by the song. At all. “Victory” without winning may pass for success in Washington, but it does not in the writer room or at a songwriter’s kitchen table.

The Proposed Settlement is a crystallization of everything that is wrong with the licensing and payment practices that have arisen under the compulsory license regime where no is yes, more is less and the Kool-Aid whispers “Drink Me.”

While the Writers will focus in this comment on the frozen mechanicals issue that has become emblematic of the current crisis, it must be said that the decade-plus MOU [black box] agreements are a backward looking and inequitable insider arrangement that permits a mindset of sloppiness and a “kick the can down the road” mentality that debilitates the entire music publishing business.[12] It’s no accident that the Mechanical Licensing Collective—run by largely the same cast of characters under a jaw-dropping Congressional governance mandate—has been sitting on $424,000,000 of other peoples’ money for nine months during a pandemic with no visible compliance with another Congressional mandate of paying songwriters correctly in Title I of the Music Modernization Act.[13]

The MLC and the sequence of MOUs are both descended from the same ancestors a generation ago. Each have essentially the same business model and each are somehow inexplicably viewed as a “win” for the songwriters. The irony of splicing the genetic code of the ancien régime MOU [black box insider settlements] to the future is not lost on anyone. If the failure to match money and songs in the MOU process is still a problem after fifteen years as well as the much-trumpeted Title I of the Music Modernization Act, it’s not the horse’s fault. It’s the rider’s.

It would be a real pity for the CRB to perpetuate this unfairness by adopting the Proposed Settlement. With respect, it is bad law, bad policy, and a failure to even try to bend the arc of the moral universe. Conversely, rejecting the Proposed Settlement would provide the kind of steely oversight tragically lacking in the current regime. Please let the future have a vote, just once.

The Writers object to the Proposed Settlement for the following reasons and respectfully suggest constructive alternatives. The gravamen of our objection is that (1) the Subpart B rates have already been frozen since 2006 and extending the freeze another five years is unjust; (2) no evidence has been publicly produced in the Proceeding that justifies or even explains extending the proposed freeze aside from the connection to the memorandum of understanding in the MOU4 late fee waiver (“MOU”), a document that the Majors only recently disclosed in their Reply; (3) very large numbers of songwriters and copyright owners of various domiciles around the world and national origins are unlikely to even know this Proceeding is happening and there still is no evidence that the unrepresented have appointed any of the participants to act on their behalf or were asked to consent to the purported settlement before the fact even if they were members of these organizations aside from the respective board of directors; (4) physical sales are still a vital part of songwriter revenue (which the Writers documented in the Prior Comment[14]); and (5) there are many just alternatives available to the Judges without applying an unjust settlement to the world’s songwriters who are strangers to the Proposed Settlement and in particular the MOU component (as the MOU will likely require membership in the NMPA to benefit consistent with prior MOUs).

[2] NMPA, NSAI, Sony Music Entertainment, UMG Recordings, Inc. and Warner Music Group Comments in Further Support of the Settlement of Statutory Royalty Rates and Terms for Subpart B Configurations, Determination of Royalty Rates and Terms for Making and Distributing Phonorecords (Phonorecords IV), Copyright Royalty Board (Aug. 10, 2021).

[3] 37 C.F.R. §385.11(a).

[4] Comments of Helienne Lindvall, David Lowery and Blake Morgan, Determination of Rates and Terms for Making and Distributing Phonorecords (Phonorecords IV) (July 26, 2021) available at https://app.crb.gov/document/download/25533.

[10] As with the Writers prior submission in response to the First Notice, the Writers focus in this comment almost entirely on the Subpart B rates applicable to physical carriers under 37 C.F.R. §385.11(a).

[11] The Judges no doubt will be told many stories about how Subpart B configurations are not meaningful sales compared to streaming so rates deserve to be frozen. This is a novel copyright argument without a statutory basis. The theory is also not based on accurate facts as the Writers discuss extensively in the Prior Comment at paragraph 5 and will not repeat here.

[12] There is a growing backlash to decades of delaying definitive action on song metadata and songwriter payments such as Credits Due campaign of the Ivors Academy and Abba’s Björn Ulvaeus. See generally Chris Cooke, PPL Backs Björn Ulvaeus’s Credits Due Campaign, Complete Music Update (Oct. 4, 2021) available at https://completemusicupdate.com/article/ppl-backs-bjorn-ulvaeuss-credits-due-campaign/

[13] See, e.g., H. Rep. 115-651 (115th Cong. 2nd Sess. April 25, 2018) at 5; S. Rep. 115-339 (115th Cong. 2nd Sess. Sept. 17, 2018) at 5 (“The Committee welcomes the creation of a new musical works database that is mandated by the legislation….Music metadata has more often been seen as a competitive advantage for the party that controls the database, rather than as a resource for building an industry on.” (emphasis added)).

You must be logged in to post a comment.