The freeze is back.

The first settlement in the Phonorecords V mechanical royalty proceeding is now on file (see below). A settlement is supposed to result from a “voluntary negotiation,” so the document raises a simple question: when exactly did the negotiation happen?

The parties describe “conversations” with other participants. Maybe there were conversations. But conversations are not the same thing as negotiation. A proposal presented as essentially a finished product, with little or no opportunity to influence its terms, is notification—not negotiation.

The Parties have had settlement conversations regarding the so-called Subpart B rates and terms with the other copyright owner Participants in the Proceeding (Songwriters Guild of America, World Collections, Inc., Eight Mile Music Companies, and George Johnson), who declined to join this settlement.

That distinction is crucial because this settlement would establish the statutory mechanical royalty rate for physical records and permanent downloads starting in 2028 through 2032. Those rates affect every songwriter, including those ex-US songwriters whose songs are exploited in the US. According to sources overseas, ex-US songwriter groups were not consulted, although it is customary for NMPA and NSAI to not engage with them even though they are a significant group (other than major mostly English language songwriters who are represented in the US by major publishers).

This means that it is likely that an alternative proposal or several alternative proposals will come to the Copyright Royalty Board in coming days from those who were not included in the NMPA’s settlement. As the settlement itself anticipates, whatever deal the Judges end up adopting will be published as a tentative ruling allowing public comment, but that’s down the line. Watch this space or the CRB website for Phonorecords V for more on deadlines, etc., if you want to comment.

To our knowledge, this is also the first time we’ve seen multiple competing settlements in a CRB phonorecords proceeding. Multiple settlements are common in webcasting and other CRB cases because different categories of music users—commercial broadcasters, NPR, college radio, religious broadcasters, and others—often negotiate different deals tailored to their own services. Mechanical royalty proceedings have traditionally been different. Everyone is negotiating one statutory rate that applies across the board divided into two broad categories by music user: labels (who pay for physical and downloads), and digital services like Spotify, Apple, Google, Amazon, and Meta (who pay for streaming mechanicals and control the global streaming market and some of which largely control AI models so lead the charge on AI theft for training).

The settlement itself also leaves some obvious questions unanswered.

Artificial intelligence is rapidly changing every aspect of music licensing, yet AI is not mentioned at all in the settlement. If downloads or streaming services increasingly contain AI-generated tracks that may not even qualify for copyright protection, should those recordings receive statutory licenses or royalties at all? The Copyright Office has repeatedly stated that works lacking sufficient human authorship cannot be registered for copyright to enjoy the protections of the Copyright Act, and the statutory license is part of the Copyright Act. If that principle eventually affects downloads or streaming (which we think it does right now), it is difficult to imagine that it will never influence the economics of physical or download mechanical royalties as well. That issue received no attention in the NMPA’s settlement.

Then there is another provision that deserves far more discussion.

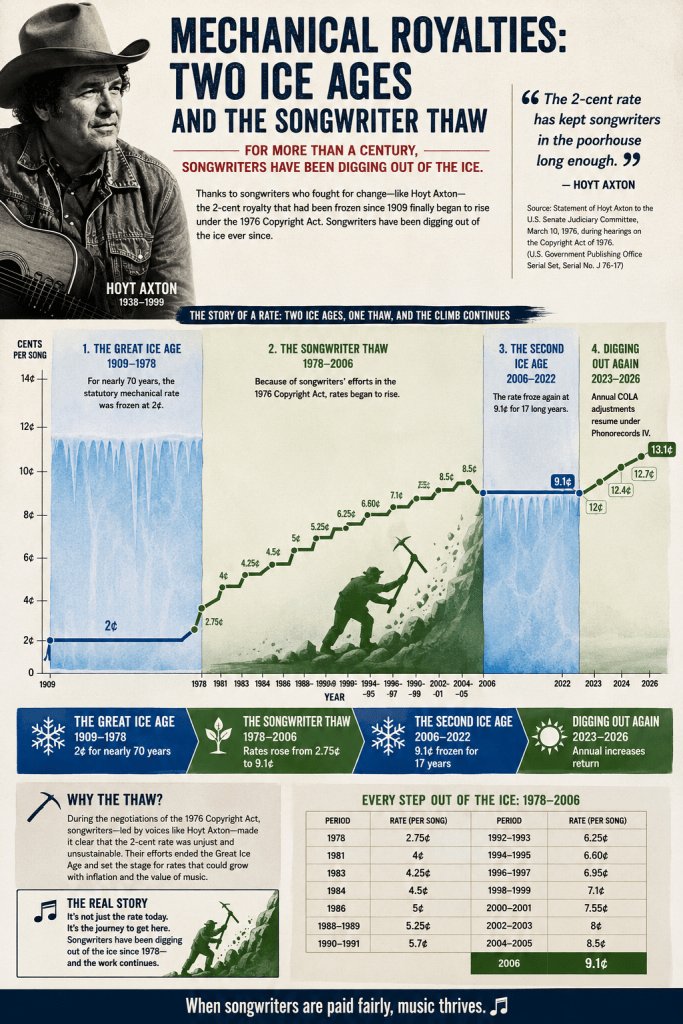

The settlement continues the existing CPI adjustment mechanism that songwriter’s fought for in the last rate setting that increased the mechanical rate from the frozen 9.1¢ proposed by the NMPA and major labels to 12¢ plus a “Cost of Living Adjustment” (or “COLA”) thanks to the Judges rejection of the extended freeze. In other words, they did the opposite of what we recently suggested in Don’t Freeze Mechanicals Again.

Adopting a 12¢ base rate makes no sense—that’s the same rate as the Judges took as the base rate for the first year of the five year rate period starting in 2023 and then applied the COLA to that rate in subsequent years. Of course, that 12¢ rate has been eroded by inflation every year and is now worth about 10¢ without the COLA, but songwriters negotiated and received that COLA which sustained the value of the rate. That’s how we got from 12¢ in 2023 to the current 13.1¢ rate in 2026 that will probably increase again for 2027 (our guess is somewhere in the 13.4¢ to 13.6¢ range). Why wouldn’t you just take that highest rate achieved during the last year of the Phonorecords IV period (2027) and start applying the COLA to that in the first year of the Phonorecords V period (2028)? Rather than go back to the arbitrary 12¢ reference rate? Huh?

On its first glance, adopting a COLA for the new rates sounds reasonable because it protects songwriters against inflation. But the formula contains no floor preventing the statutory rate from declining if cumulative CPI were ever to fall.

Deflation may be unlikely. That’s not the concern. But the COLA could still cause rates to decline. All that has to happen is that inflation doesn’t rise at the same rate or greater from one year to the next and then the COLA-adjusted statutory rate will decline.

The point is that, for what may be the first time in the history of the statutory rate and certainly since the modern Copyright Act took effect in 1978, songwriters are being asked to accept a statutory mechanical royalty structure under which the minimum statutory rate could actually move backward, and very likely will decline.

A simple solution exists. The regulation could easily provide that each year’s rate is the greater of (1) the COLA-adjusted calculation or (2) the prior year’s rate. That would preserve the existing inflation formula while ensuring the statutory royalty never declines.

Why wasn’t that included? Or better yet, why wasn’t an actual value based increase included since we are still digging out of two prior freezes of the statutory rate one from 1909-1978 when the rate froze at 2¢ and the other from 2006-2022 when the rate froze at 9.1¢.

That’s a fair question.

So is another one.

If we’re going to lock in the statutory mechanical royalty through 2032, shouldn’t there have been a meaningful discussion—not just among the settling parties, but across the songwriting community—about AI, future valuation, whether there should be a statutory minimum for streaming and whether the statutory minimum itself should ever be permitted to decrease?

Those conversations are coming. The only question is whether they should have happened before the settlement was filed instead of afterward. We had hoped for a longer table with more voices. Whether that happens remains to be seen.

You must be logged in to post a comment.