Here we go again. To see previous years, click [here].

This data set is isolated to the calendar year 2018 and represents a mid-sized indie label with an approximately 250+ album catalog now generating almost 1b streams annually. 2018 is the year we saw streaming truly mature as the dominant source of recorded music revenues.

In parsing the data provided we find that digital revenues are 86% of all recorded music revenues globally (RIAA Reports Digital Revenues as 90% of Total). Streaming is 80% (or more) of Digital Music Revenues. Downloads are about 20% of digital music revenues for the year, however if we isolate Q4, it would appear download revenues could be less than 15% of digital revenues. The transition from downloads to streaming is well beyond the tipping point and we wonder how long the major services (Apple, Amazon, Google) will continue to support the format.

As we dig down into the physical revenues much of the gross is eroded by manufacturing, shipping and inventory costs of both CDs and Vinyl. In short, the recorded music business is now the streaming music business. Whatever charm there is to vinyl, it is at best still a truly niche business in terms of meaningful net revenues.

Every year there are surprises in the data and this year is no exception. As always we present this data as a single sample, but one we feel is fairly representative of the state of the business. As such, we welcome comments from others with access to similar data to report on their findings. Some of the percentages may vary dependent upon the genre of music and the size of the label or artist. However, we generally don’t find trends that are completely contradictory to our sample where it matters most, in reporting on stream rates and relative marketshare.

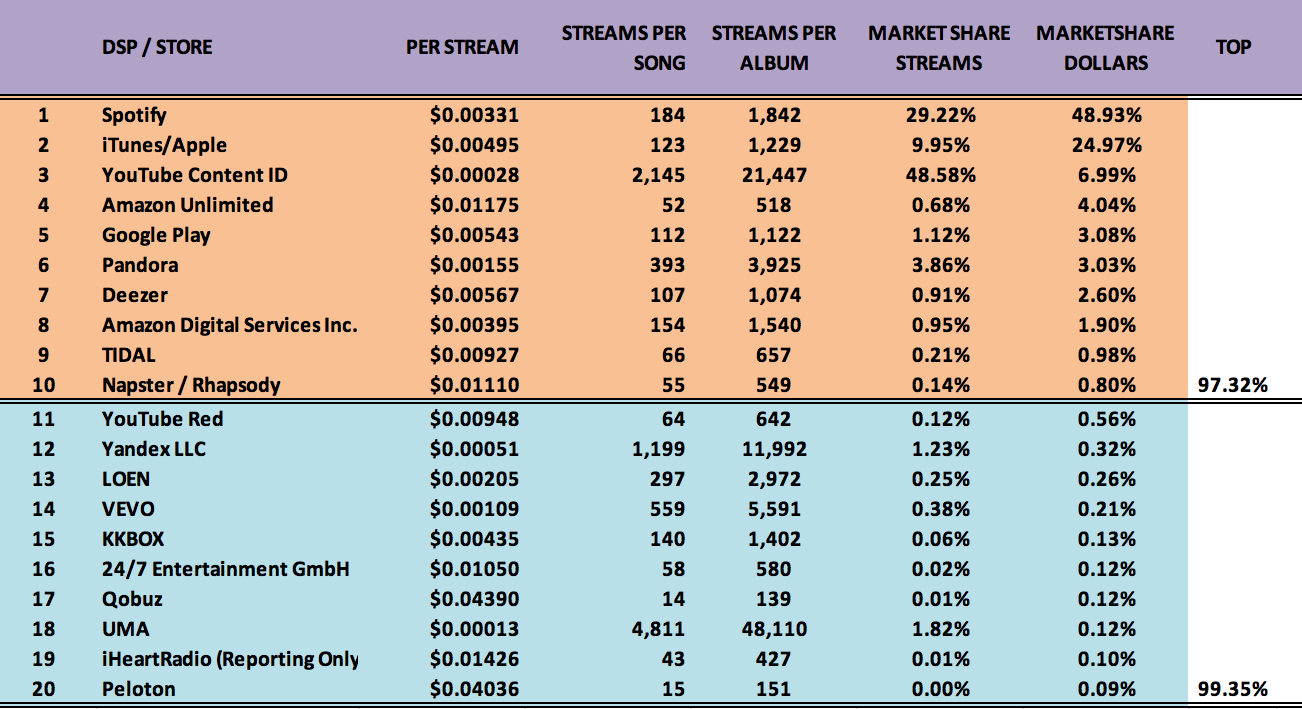

We’ve also simplified the chart this year. Just one chart, and only the Top 20 streamers which represent 99.35% of all streaming dollars. The Top 10 streamers account for over 97% of all music streaming revenues. The Top 5 account for over 88% of all streaming dollars. What we see below is a maturing marketplace with a small number of dominant players. Anyone who thought the digital revolution would remove so called “gate keepers” are painfully wrong.

If you want to compare these numbers against the RIAA’s official report for the first half of 2018, click [here]. That data is for the USA and only through June of 2018. It’s hard to get “apples to apples” reporting, so everything should be taken as different perspectives on the overall business. If you are an artist or label, see how your own data compares.

The biggest takeaway by far is that YouTube’s Content ID, (in our first truly comprehensive data set) shows a whopping 48% of all streams generate only 7% of revenue. Read that again. This is your value gap. Nearly 50% of all recorded music streams only generate 7% of revenue.

The Spotify per stream rate drops again from .00397 to .00331 a decrease of 16%. Apple Music gains almost 3% for an total global marketshare of about just under 25% of all revenue.

Apple’s per stream rate drops from .00783 to .00495 a decrease of 36%. We need to state again, that 2018 saw a massive shift of revenues from downloads to streaming and no doubt this expansion of scale, combined with more aggressive bundling (free trials) as well as launching into more territories was bound to bring down the overall net per stream.

Apple Music still lead in the sweet spot with about 10% of overall streams generating 25% of all revenue (despite the per stream rate drop). Spotify by comparison has nearly triple the marketshare in streams than Apple Music but generates less than double the revenues on that volume.

The biggest takeaway by far is that YouTube’s Content ID, (in our first truly comprehensive data set) shows a whopping 48% of all streams and only 7% of revenue. Read that again. This is your value gap. Nearly 50% of all recorded music streams only generate 7% of revenue. Apple Music and Spotify combined account for just short of 40% of all streams and 74% of all revenue.

We don’t know how the powers that be at the major labels can continue to allow for this gross inequity. It will be interesting to see how YouTube Red numbers evolve over this year. YouTube Red, the newly rebranded version of the disastrous “Music Key” is off to a slow start in a competitive subscription music marketplace. One has to ask, what incentive is there really for Google/YouTube with the Red subscription service when they already benefit from service 48% of all streams while paying only 7% of the overall revenue?

In looking at the per stream rates for song and album, you might want to read this article by Billboard on the current calculation of how many streams equal and album for the purposes of charting. We don’t know if YouTube Content ID streams count towards charting, but they absolutely should not. The report states that, “The Billboard 200 will now include two tiers of on-demand audio streams. TIER 1: paid subscription audio streams (equating 1,250 streams to 1 album unit) and TIER 2: ad-supported audio streams (equating 3,750 streams to 1 album unit).”

In the coming year Amazon’s Unlimited Music service shows promise. We also wonder about Google Play. The payouts on Google Play are fair, but when bundled into the YouTube ecosystem is largely inconsequential in terms of both streams served and revenue. As smart home assistants grow there could be a larger market segment for paying subscribers to have streaming music catalogs available and on demand.

These numbers are from one set of confidentially supplied data for global sales. If you have access to other data sources that you can share, we’d love to see it.

- HOW WE CALCULATED THE STREAMS PER SONG / ALBUM RATE:

- As streaming services only pay master royalties (to labels) and not publishing, the publishing has to be deducted from the master share to arrive at the comparable cost per song/album.

- $.99 Song is $.70 wholesale after 30% fee. Deduct 1 full stat mechanical at $.091 = $.609 per song.

- Multiply the above by 10x’s and you get the album equivalent of $6.09 per album

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

[royalties][streaming royalties][music royalties][royalty rates]

You must be logged in to post a comment.