We’ve been hearing an alarming narrative that “record labels are making more money than ever from streaming, but they’re just not paying musicians”. To be clear, we certainly have our issues with major labels, however we also need facts and to be truthful.

The truth is, that a decade after losing half of it’s revenues due to piracy as reported by CNN (click here), record labels are now only getting back up to half of what the peak business was in 1999. Half of where we were in 1999, twenty years later. Let that sink in. As unpopular as he was twenty years ago, Lars Ulrich was right.

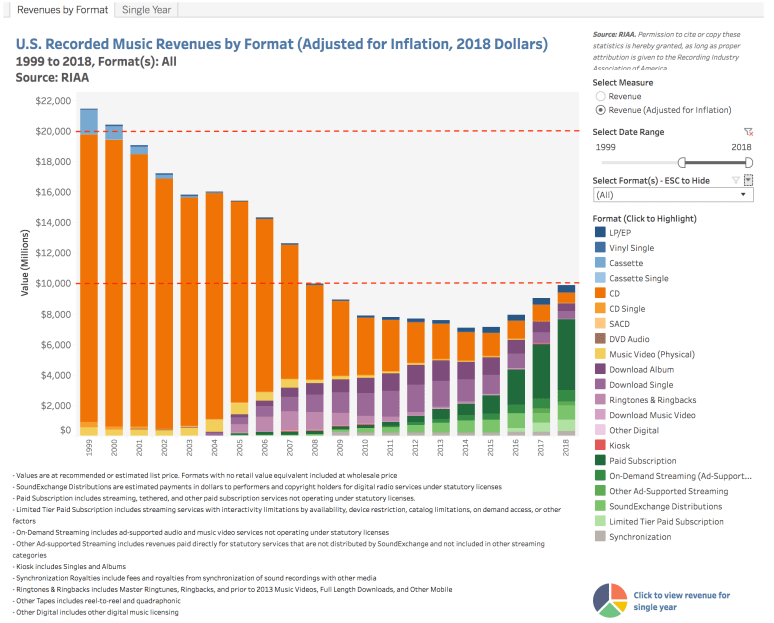

Twenty years later, and we’re still only half of where we were in 1999.

There are only three numbers that matter when looking at the record industry post-piracy and here they are:

1999 : $14.6b = $22.01 in 2018 Dollars

2009 : $6.3b = $7.37 in 2018 Dollars

2018 : $9.8b = $9.8b in 2018 Dollars

This is clearly illustrated in the chart below provided by the RIAA, the trade group responsible for tracking these figures. At their lowest point in 2014, revenues from record sales were less than one third of their peak.

What this chart also shows is a decade long loss of $10b or more annually, which is over $100b in lost revenues to labels and artists. That’s $100b in lost revenues to labels and artists in just the past decade.

If we track total lost revenue to labels and artists since the launch of Napster in 1999 it totals just under $200 Billion Dollars in the USA alone.

The fundamental problem remains the same. There’s a hole in our bucket and all that revenue falling out though the bottom leads more or less to advertising funded piracy and YouTube. Many have suggested that YouTube is effectively the largest ad supported piracy platform. As we reported earlier this year in our updated Streaming Price Bible, the YouTube Value Gap is very, very real.

In future posts we’ll offer solutions and suggestions that should be under consideration at every major label. Not the least of which is transitioning subscription streaming models to incorporate a per stream transactional baseline, or a minimum wholesale price per stream.

In streaming, consumption does not grow revenues. More consumption and more streams do not generate more money. Revenue can only be generated by charging more for subscriptions, generating more advertising revenue (ad supported only, obviously) and expanding into more markets (gaining new subscribers). But eventually, everything flattens.

So the biggest question remains. What happens to overall revenues as streaming matures and cannibalizes the remaining revenue sources into purely niche markets. Digital Downloads will account for less than 10% of recorded music revenues by the end of the year, if not already. The CD market continues drop, and vinyl also declined slightly from 2017 (4.4%) to 2018 (4.3%).

Will streaming compensate for the lost revenues in other formats and continue to grow revenues towards a true recovery? It’s possible, but there will have to be some changes to address the economics presented to consumers despite what Goldman Sachs says. For the year of 2018 the industry reported $9.8b in revenues. To make that $37.2b by 2030 the industry needs to add nearly $3b a year for the next 10 years!

We don’t know what else they’ve got in that crystal ball that can predict revenues over a decade into the future but even by their bullish estimate of $37.2b in 2030, that is only $28b in 2019 dollars. Right now we’re still about $20b short.

You must be logged in to post a comment.