It’s been just over two years since Maria Schneider sued YouTube for copyright infringement. But the court has now cleared a path for her to actually proceed with her main case by dismissing–emphatically–YouTube’s motion to dismiss for failure to state a claim.

Schneider sued YouTube in 2020 on behalf of a proposed class of small copyright owners, arguing the platform only protects large copyright owners from infringement while allowing pirated content from others in order to draw in users. The group said major companies have access to YouTube’s advanced Content ID software to scan for and automatically block infringing content, while individual creators are left “out in the cold.”

But that’s not the critical part. Maria’s lawsuit alleges that YouTube YouTube removed copyright management information (CMI) in violation of 17 U.S.C. § 1202(b)–potentially intentionally.

The amended complaint states that YouTube knew that files containing audio and/or video works routinely contain CMI, that CMI is valuable for protecting copyright holders, and that the distribution of works with missing CMI on YouTube has induced, enabled, facilitated, and concealed copyright infringement. The plausible inference from these and similar allegations is that YouTube removed the CMI from plaintiffs’ works with knowledge that doing so carried a “substantial risk” of inducing infringement.

One could see how anyone who intentionally removes one brick from the complex wall that protects big infringers like YouTube from truly massive liability for copyright infringement would be in a whole heap of trouble for inducing infringement (which gets you into Grokster land).

Personally, it’s my view that this is exactly what YouTube and Google do on a massive scale and that they should pay the class damages that will dwarf all the fines these people have already paid for everything from violations of the Controlled Substance Act to competition law violations. Truly Carl Sagan level damages…billions and billions.

We’re lucky Maria’s on the side of the angels. Fight on.

If enough non-partner artists screen grab the new ads over their @Youtube videos and politely Twitter mention the advertiser (they probably aren't even aware) maybe it will have an effect. It's not as if @Google don't have enough money already. #notagoodlook@thetrichordisthttps://t.co/bpCms2qF9D

By now you are probably aware of the campaign to get brands to stop advertising on Facebook because of the prevalence of hate speech. The campaign has been endorsed by a number of civil rights organizations including The NAACP and Anti-Defamation League. The campaign owes much of it’s success to Sleeping Giants (twitter handle @slpng_giants) a largely anonymous social media activist group. Sleeping Giants was the force behind successful advertiser boycotts of Breitbart and Fox News. Facebook is now their biggest trophy.

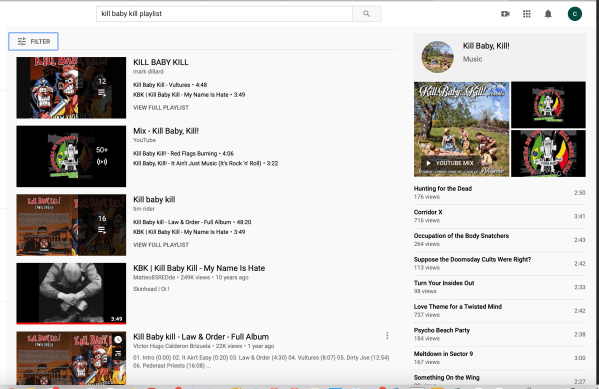

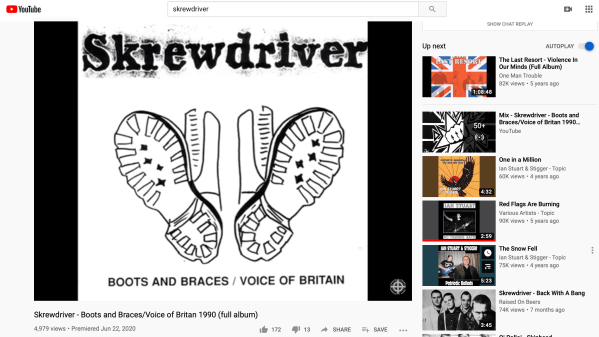

Over the last decade, my fellow bloggers at the Trichordist have documented the prevalence of white nationalist and neo-nazi music on YouTube. Here are just a few examples:

YouTube advertisers have periodically reacted to these reports by pulling advertising. But YouTube continues to be loaded with hate rock. You can verify this yourself by checking the Southern Poverty Law Center list of white nationalist bands and then searching on YouTube. Here are some screenshots from my most recent search.

Fortress, Kill Baby Kill, The Bully Boys, Skrewdriver, Final War, etc. The gang is ALL there! And not all these videos were “user-generated content.” Many of these were official uploads by music distributors like CD Baby (Bully Boys). And of course, many of these videos were monetized by YouTube.

So if advertisers are concerned that their ads will end up next to hate speech shouldn’t the #StopHateForProfit boycott also include YouTube? Then again maybe some advertisers just don’t care? (See below).

A performance metric one hears from the digerati is the term “conversion rate.” “Conversion rate” for a streaming service usually means the rate at which users of an ad-supported free service are “converted” to paying users. That motivation is usually because they are so fed up with the advertising they are willing to pay. (This was one of the many failed pitches from Spotify before people stopped trying to justify hanging on until the IPO riches flowed in.)

YouTube, of course, has never been too terribly interested in anything that moves users away from advertising. That resistance (and potential internal competition between the massive ad sales team and the ever changing YouTube managers), may explain the many failed efforts at launching a YouTube subscription service by a company that knows more about user behavior than anyone in history. They just couldn’t seem to get it right for the longest time. You don’t suppose that YouTube’s apparent lack of interest in getting large numbers of users to substitute away from free to subscription was because YouTube made a lot more money from the ads than they ever would from the subscriptions?

One of the ways that YouTube (and Google) makes money from advertising is by taking money that is not theirs to take (sometimes called “monetizing” content). The civil law calls that act a claim of “conversion” and the criminal law calls it the crime of “theft”. Conversion and theft are two sides of the same coin and often one implies the other, albeit with different burdens of proof.

YouTube’s Content ID tool is a way for copyright owners to block or permit advertising on user-generated content that includes their copyrights, often music. Users of Content ID will tell you that it works just well enough that Google can say it is an effective tool, but even with Content ID music still gets through (and is often monetized by YouTube) for a variety of reasons. This requires time consuming and costly manual searches. Companies like AdRev make it a bit easier, but are essentially third party Content ID users. These companies are compensated with a commission on infringing works they find on YouTube that they convert–there’s that word again–from infringing to monetized, which means that YouTube now splits the advertising revenue with the copyright owners who in turn split their share with an AdRev.

But see what happened there? If you have Content ID, you can block on the upload some of the time, or you can do a search. If you don’t have Content ID (see Maria Schneider’s class action) then you can’t block on the upload only chase the infringements manually. But quite rightly from an economic perspective, companies like AdRev are not that interested in doing that work on a rev share basis if there’s no rev share when you block.

Here’s the point–you have a property right in your copyright. You have a property right to license that copyright. Any revenue derived from exploitations of that copyright is your money. YouTube uses its monopoly power to impose a deal to monetize your copyright (under duress, of course, due to whack a mole DMCA). That deal involves a revenue share. (Let’s just assume you decide to take the King’s shilling and accept Google’s deal under duress which you shouldn’t have to do and which may not even be enforceable.)

The question is, when should that revenue share attach–when they start exploiting your copyright in violation of your property rights or when you catch them doing it. And if (1) you catch them violating your property rights and (2) agree to monetize, when should they pay you your agreed upon share of the revenue from monetizing? Should they pay retroactively to the first exploitation? Or only prospectively after you catch them?

The correct answer is they should pay retroactively. But they don’t. They just keep the money. For millions of infringements. And they get away with it because of their monopoly power, which leaves one choice most artists won’t make, which is to sue them like Maria has.

Remember–Content ID operates largely like any other fingerprinting tool. (Psychoacoustic fingerprinting is old technology–remember Jonesy in “The Hunt for Red October”? That’s fingerprinting. A “fingerprint” is simply a mathematical rendering of the waveform of an audio file.)

There is a reference databases of recordings that are “known knowns” (which is why it is important to be included in the Content ID database as Maria Schneider correctly points out in her class action.) The fingerprinting tool encounters a new file, takes a fingerprint, then looks for a match in the reference database and reports a result that triggers an action. Typically, fingerprinting tools are binary: match or no match. What happens after the tool finds a match is entirely in the control of the operator. (So while the tool could have a match rate of 90%, the operator could report a random number of matches or a fixed number of matches, like one every ten, or one every 1000. That means 90% accuracy could turn into a much lesser percentage of reported matches. It’s important to know how many matches trigger an action.)

Having had some experience with audio fingerprints, I think you will find that once a fingerprint is in the reference database, the recognition tool (Content ID in this case) will spot the reference fingerprint a very, very high percentage of the time. The fingerprinting tool I’m most aware of caught matches over 90% of the time. I can’t imagine that a tool developed by the biggest technology company in commercial history would do less–unless they wanted it to. Remember, this is not taking into account re-records unless the re-record is itself in the database, or pitch bends. This is an exact match which is very common use of Content ID. (See Maria’s class action complaint, and Kerry Muzzey has a great description of this in his recent Senate testimony.)

If Content ID is actually missing matches to known knowns on the upload (assuming exact matching is possible), I find it very odd that Content ID is missing much. Maybe it’s not, but one way to find out is to force Google to reveal the inner workings through discovery in the class action case.

But if Content ID does miss exact matches, it would be interesting to know what percentage of those misses end up being monetized, and of those, what percentage end up getting caught later by a subsequent use of Content ID or a manual investigative process. This will give an idea of the scale of the retroactive payment issue.

As Maria rightly points out, it is virtually impossible for an artist or film maker without Content ID to catch YouTube monetizing infringing works. But I think the analysis has to go a step further–even if you have Content ID, at the moment you catch YouTube monetizing illegal versions, you are in no different position than the artist who lacks access to the Content ID tool.

Both have the same problem–YouTube is profiting from illegal copies. If when you catch them you then elect to monetize, YouTube will pay you going forward, i.e., prospectively. But I do not believe they will pay you retroactivelyfor the illegal use. (There is a rumor that some music publishers do get paid retroactively under some settlement, but that needs to be confirmed.)

That means that YouTube is directly profiting from piracy for the retroactive views which could total into the hundreds of millions per day given the massive number of daily views on YouTube. If you elect to monetize due to YouTube’s monopoly power, you are essentially releasing them from liability under duress. Ifyou catch them.

So YouTube takes your property, monetizes it, and refuses to pay you for how much they made before you caught them if you ever do catch them. They dare you to sue them because you would be taking on the biggest company in commercial history that controls 90% of the access to information in the world and routinely defies governments. Not everyone has the spine of Maria Schneider.

Failing to license at all or failing to pay retroactively means that YouTube profits from piracy by converting your property to their own. And as Maria rightly points out, Google scrapes user data through non-display uses in the background even if YouTube is not monetizing overtly which they then use to compile user profiles in “millions of buckets” (which dribbled out before Judge Koh in the Gmail litigation (In Re: Google, Inc. Gmail Litigation, Case No. 13-MD-02430-LHK, (U.S.D.C. N.D. California, San Jose Division, Sept. 26, 2013)).

In either case, the value of the amount converted or stolen should rightly include the value of these user profiles scraped in the background, as well as the advertising revenue.

And don’t forget that Google is controlled by Larry Page, Sergei Brin, and Eric Schmidt through their “supervoting” shares of stock. It’s hard to believe that this YouTube policy was created without their blessing.

The simplest move for Google would be to simply pay both retroactively and (if the copyright owner elects to monetize) prospectively. Otherwise, it seems like a huge number of crimes are going on in a very planned and organized way dreamed up by YouTube and Google employees. “Dreamed up” is also called a conspiracy, and if there’s an actual conspiracy it’s not a theory (which came up in an interesting trade secret misappropriation RICO case against Google they managed to wriggle out of, at least for the moment).

The law has another word for organized theft at scale–we sometimes call it “racketeering.”

Google and YouTube have managed to create a scam that has gone both largely undetected and largely unpunished for a decade–illicit activity that can be both seen and quantified through the sale of advertising and is also unseen and unquantified through data scraping in the background. (I leave it to you to speculate which is more valuable.)

Google has also faced down civil RICO claims for racketeering through the theft of intellectual property. The last reported RICO case against Google offers a checklist for how to make a civil RICO claim stick against the Leviathan of Mountain View. I like the YouTube case a lot better than the inventor’s case they beat back.

But most of the time Google just keeps the money when they get caught. A prime example is YouTube’s standard practice of refusing to pay a revenue share retroactively after you catch them infringing your work using Content ID. That unjust enrichment creates an incentive to sharply limit the number of artists or songwriters who get access to Content ID in the first place. I think this is why Google massively overreacted to Mississippi Attorney General Jim Hood’s Civil Investigate Demand and subpoena that they never did respond to. Maybe they were covering up the same crimes that got them prosecuted in Rhode Island and they did not want to go through that again.

And therein lies the rub and our topic today: If Google never gets caught, Google quietly keeps all the money. For our world, this happens because they’ve artificially limited the tools that independent creators can use to catch the massive infringements. And even if the majors and a handful of independents get the Content ID tool, YouTube still has the incentive to make Content ID just good enough that they can say it works, but not so good as to actually stop the infringement before it starts.

The majors using Content ID have to employ still other means to catch them, sometimes manually, at great cost. In fact, you have to wonder if net-net the total costs of administering the YouTube deals actually exceeds the minimum guarantee and royalty payable. Those tools are simply beyond the reach of the creators, even the few who YouTube grants access to Content ID.

And of course, any user of Content ID (big or small) has to sign up to the take-it or leave-it shakedown deal that limits what you can do about it when you catch them. Which is just another form of the protection rackets.

This criminal enterprise comes in two flavors (at least): Ad sales for illegal products (like the drugs, counterfeit tickets and the like), and selling legitimate advertising around content that Google knows or should have known was illegal (like YouTube’s monetization of infringing works). And, of course, Google scrapes data in the background on all these criminal activities to its great–and secret–profit.

As we saw with the drugs case, Google knew exactly what it was doing, and I’m not willing to believe their rudderless ad sales teams don’t also know exactly what they are doing (remember Google’s ad sales team gave credit terms to infringers, and the drugs sting operation also shows that they brainstormed many criminal dodges to deceive Google’s own best practices team).

What little evidence we can lay hands on in the open source demonstrates that Google must know very well that it engages in criminal behavior–why else was Eric Schmidt advised by then-counsel David Drummond to refuse to answer Senator John Cornyn’s questions regarding the drugs case when Schmidt testified before a 2011 Senate Antitrust Subcommittee hearing? (Also known as “taking the Fifth.”) After engaging in a weak attempt at misdirection. Did they think this question wouldn’t come up so didn’t prepare for it? I doubt that very much. (If they cooked up this story without the lawyers, this might well have been a conspiracy. Attorneys take note: Crime/fraud execution?)

Eric Schmidt Takes the Fifth on drugs case to Senator John Cornyn: ” I have been advised — unfortunately, I’m not allowed to go into any of the details and I apologize, Senator”

Now that the U.S. Senate is investigating the effectiveness of the safe harbors under DMCA, this would be a good time for the Department of Justice to investigate Google’s business practices and potential criminal activities. Smells like RICO to me.

My name is Kerry Muzzey, and I am a film and television and modern classical composer.

I am one of the very few independent artists who has access to YouTube’s Content ID system; and most of my experience with notice and takedown has been on YouTube. Content ID has become a core piece of my licensing business: it is the x-ray that reveals the theft of my music to me. This is why I am also nervous about speaking out today – because I fear retaliation by YouTube and Google. I am concerned that they may take Content ID away from me for raising my concerns publicly. The technology behind Content ID is nothing short of brilliant, and I don’t want to lose access to it.

Growing up, my mom always said: “You’re not allowed to complain unless you’re gonna do something about it.” Senators, my being here today is my “doing something about it.” Today, I have the most unique opportunity I have ever had in my lifetime. I have the opportunity to ask Members of my United States Senate to fix a broken law.

Let’s also not forget the way Google is governed (as is Facebook, Spotify and many others). Larry Page, Sergei Brin and Eric Schmidt hold a special class of “supervoting” shares, what SEC Commissioner Robert Jackson has called “corporate royalty”.

These insiders get 10 votes for every one share they own of a special class of supervoting stock. This means that the insiders control over 60% of the voting stock and win all shareholder votes—including votes to appoint the board of directors.

Supervoting shares give insiders absolute control of Google–one of the most successful public companies in commercial history. Because they control every aspect of Google’s operations, Google truly is their “alter ego.” One purpose of Google’s lobbying spend must be to keep the corporate royalty out of prison.

These supervoting Google Class B shares are not available to the public. The public can buy two classes of stock: GOOGL shares are Class A (one vote per share) and GOOG shares are Class C (no votes per share). (GOOG shares were issued in a dividend to GOOGL holders.) GOOGL shares typically trade slightly higher than GOOG which may demonstrate that the market has priced in a lack of meaningful voting rights in GOOGL.

It should not be surprising that Google shareholder meetings are a one-way communication event. The supervoting corporate royalty tell the other shareholders how things are going to be and vote down any move by GOOGL holders to change the status quo—like converting supervoting shares into one share one vote. As Floyd Norris reported in his New York Times “Economix” column, “Rarely has a shareholder vote been less suspenseful.”

So Google’s profit from evil is not an accident. If Congress wants to fix the DMCA, let’s fix all of it. And as U.S. Attorney Peter Neronha discovered ten years ago, that requires a grand jury.

This data set is isolated to the calendar year 2019 and represents a mid-sized indie label with an approximately 350+ album catalog now generating over 1.5b streams annually. Streaming is now a fully mature format, and it is also the number one source of revenue for recorded music. Streaming in all configurations now accounts for 64% of all recorded music revenues. Head on over to the RIAA US sales database [here] to check out the numbers. Pro Tip: Remember to adjust for inflation!

We are keeping a simplified chart again this year. We’ve extended to the top 30 streamers which represent 99.87% of all streaming dollars. The Top 10 streamers account for over 93% of all music streaming revenues (down from 97% last year). The Top 5 account for over 83% of all streaming dollars (down from 88% last year). The drop in overall revenues in the Top 5 and Top 10 are the result of YouTube’s Content ID pulling down the overall revenues / per stream.

The biggest takeaway by far is that YouTube’s Content ID, shows a whopping 51% of all streams generate only 6.4% of revenue. Read that again. This is your value gap. Over 50% of all music streams generate less than 7% of revenue.

This is the first time we have not seen the Spotify per stream rate drop since the service launched a decade ago. The Spotify per stream rate has stabilized moving up just slightly to .00348 from .00331. In other words Spotify is paying out about $3,300 – $3,500 per million plays. We’re working with a very large sample that has aggregated all streams and revenue against both subscription and ad supported revenues for a single per stream average. This overall average is helpful for anyone who wants to calculate gross revenues by simply looking at the numbers on Spotify itself. For those who may not know, there is a simple “trick” to see the streams of any song on Spotify. On the desk top app, go to the album view and hover your mouse/cursor over the ||||||| at the far right side of any song, just to the right of the song length. Once there the plays for the song will materialize just below the song length.

Using our average, the song above has earned between $4,026 – $4,270.78 (gross before distribution fees) on Spotify at 1,220,224 plays.

Apple Music is again the best value per stream accounting for nearly 25% of all streaming revenue on only 6% of consumption. Spotify generates the most overall revenue of any streamer (no surprise) at 44% of all streaming revenue on 22% of consumption. As stated before, and which can not be overstated enough, You Tube’s Content ID is the major issue limiting growth contributing only 6% of revenues on over half of all streams, at 51% of total consumption. That’s a staggering statistic.

Apple’s per stream rate also stabilizes this year hitting a per stream rate of .0675 which is much closer to where it was two years ago at .00783. Our numbers from 2018 showed a dramatic drop in Apple’s rate at .00495 which we attribute to an expansion into new territories and a large number of 90 day free accounts that had not matured to fully paid subscribers.

In looking at the per stream rates for song and album equivalents, you might want to read this article by Billboard (as of 2018) on the current calculation of how many streams equal an album for the purposes of charting. The report states that, “The Billboard 200 will now include two tiers of on-demand audio streams. TIER 1: paid subscription audio streams (equating 1,250 streams to 1 album unit) and TIER 2: ad-supported audio streams (equating 3,750 streams to 1 album unit).” Our numbers suggest however it would be more fair to average all revenues, against all streams (including content ID), and that actually lands at about 3,516 streams per album across the board.

These numbers are from one set of confidentially supplied data for global sales. If you have access to other data sources that you can share, we’d love to see it.

HOW WE CALCULATED THE STREAMS PER SONG / ALBUM RATE:

As streaming services only pay master royalties (to labels) and not publishing, the publishing has to be deducted from the master share to arrive at the comparable cost per song/album.

$.99 Song is $.70 wholesale after 30% fee. Deduct 1 full stat mechanical at $.091 = $.609 per song.

Multiply the above by 10x’s and you get the album equivalent of $6.09 per album

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

Sometimes we just have to look at a little bit of history to put things into perspective. It’s hard for us to believe that there is even a debate about The Value Gap for recorded music. Check this out as reported by AOL News in 2010.

Google had an internal meeting on competing with YouTube, and its executives were highly critical of YouTube: “A large part of their traffic is pirated content.” YouTube is a “rogue enabler of content theft.” “YouTube’s business model is completely sustained by pirated content.” “… it’s a video Grokster.” “I can’t believe you’re recommending buying YouTube . . . they’re 80% illegal pirated content.”

In the end, it’s the DMCA that protected Google and it’s the DMCA that needs to be fixed. It’s that type of fix that the EU’s Article 13 sought to address. It would be nice to address those issues here, in the USA, where Google and YouTube are based.

We’ve been hearing an alarming narrative that “record labels are making more money than ever from streaming, but they’re just not paying musicians”. To be clear, we certainly have our issues with major labels, however we also need facts and to be truthful.

The truth is, that a decade after losing half of it’s revenues due to piracy as reported by CNN (click here), record labels are now only getting back up to half of what the peak business was in 1999. Half of where we were in 1999, twenty years later. Let that sink in. As unpopular as he was twenty years ago, Lars Ulrich was right.

Twenty years later, and we’re still only half of where we were in 1999.

There are only three numbers that matter when looking at the record industry post-piracy and here they are:

1999 : $14.6b = $22.01 in 2018 Dollars 2009 : $6.3b = $7.37 in 2018 Dollars 2018 : $9.8b = $9.8b in 2018 Dollars

This is clearly illustrated in the chart below provided by the RIAA, the trade group responsible for tracking these figures. At their lowest point in 2014, revenues from record sales were less than one third of their peak.

What this chart also shows is a decade long loss of $10b or more annually, which is over $100b in lost revenues to labels and artists. That’s $100b in lost revenues to labels and artists in just the past decade.

If we track total lost revenue to labels and artists since the launch of Napster in 1999 it totals just under $200 Billion Dollars in the USA alone.

The fundamental problem remains the same. There’s a hole in our bucket and all that revenue falling out though the bottom leads more or less to advertising funded piracy and YouTube. Many have suggested that YouTube is effectively the largest ad supported piracy platform. As we reported earlier this year in our updated Streaming Price Bible, the YouTube Value Gap is very, very real.

In future posts we’ll offer solutions and suggestions that should be under consideration at every major label. Not the least of which is transitioning subscription streaming models to incorporate a per stream transactional baseline, or a minimum wholesale price per stream.

In streaming, consumption does not grow revenues. More consumption and more streams do not generate more money. Revenue can only be generated by charging more for subscriptions, generating more advertising revenue (ad supported only, obviously) and expanding into more markets (gaining new subscribers). But eventually, everything flattens.

So the biggest question remains. What happens to overall revenues as streaming matures and cannibalizes the remaining revenue sources into purely niche markets. Digital Downloads will account for less than 10% of recorded music revenues by the end of the year, if not already. The CD market continues drop, and vinyl also declined slightly from 2017 (4.4%) to 2018 (4.3%).

Will streaming compensate for the lost revenues in other formats and continue to grow revenues towards a true recovery? It’s possible, but there will have to be some changes to address the economics presented to consumers despite what Goldman Sachs says. For the year of 2018 the industry reported $9.8b in revenues. To make that $37.2b by 2030 the industry needs to add nearly $3b a year for the next 10 years!

We don’t know what else they’ve got in that crystal ball that can predict revenues over a decade into the future but even by their bullish estimate of $37.2b in 2030, that is only $28b in 2019 dollars. Right now we’re still about $20b short.

Here we go again. To see previous years, click [here].

This data set is isolated to the calendar year 2018 and represents a mid-sized indie label with an approximately 250+ album catalog now generating almost 1b streams annually. 2018 is the year we saw streaming truly mature as the dominant source of recorded music revenues.

In parsing the data provided we find that digital revenues are 86% of all recorded music revenues globally (RIAA Reports Digital Revenues as 90% of Total). Streaming is 80% (or more) of Digital Music Revenues. Downloads are about 20% of digital music revenues for the year, however if we isolate Q4, it would appear download revenues could be less than 15% of digital revenues. The transition from downloads to streaming is well beyond the tipping point and we wonder how long the major services (Apple, Amazon, Google) will continue to support the format.

As we dig down into the physical revenues much of the gross is eroded by manufacturing, shipping and inventory costs of both CDs and Vinyl. In short, the recorded music business is now the streaming music business. Whatever charm there is to vinyl, it is at best still a truly niche business in terms of meaningful net revenues.

Every year there are surprises in the data and this year is no exception. As always we present this data as a single sample, but one we feel is fairly representative of the state of the business. As such, we welcome comments from others with access to similar data to report on their findings. Some of the percentages may vary dependent upon the genre of music and the size of the label or artist. However, we generally don’t find trends that are completely contradictory to our sample where it matters most, in reporting on stream rates and relative marketshare.

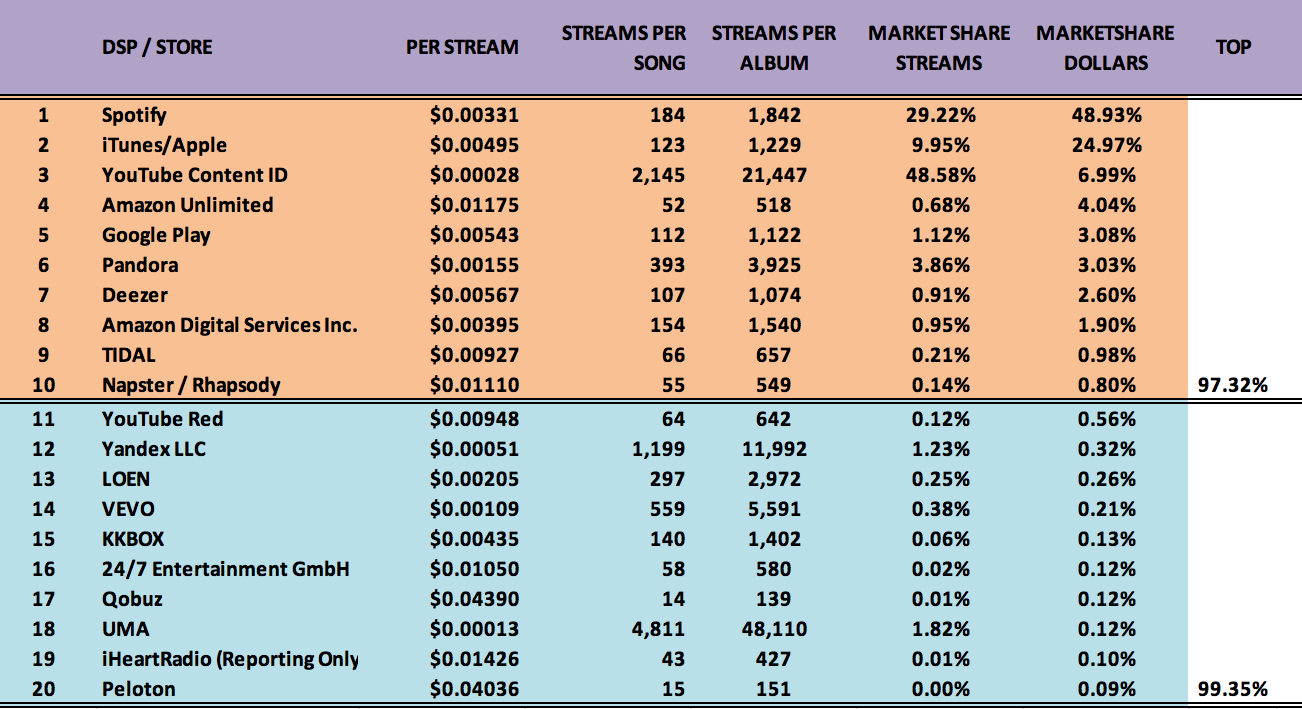

We’ve also simplified the chart this year. Just one chart, and only the Top 20 streamers which represent 99.35% of all streaming dollars. The Top 10 streamers account for over 97% of all music streaming revenues. The Top 5 account for over 88% of all streaming dollars. What we see below is a maturing marketplace with a small number of dominant players. Anyone who thought the digital revolution would remove so called “gate keepers” are painfully wrong.

If you want to compare these numbers against the RIAA’s official report for the first half of 2018, click [here]. That data is for the USA and only through June of 2018. It’s hard to get “apples to apples” reporting, so everything should be taken as different perspectives on the overall business. If you are an artist or label, see how your own data compares.

The biggest takeaway by far is that YouTube’s Content ID, (in our first truly comprehensive data set) shows a whopping 48% of all streams generate only 7% of revenue. Read that again. This is your value gap. Nearly 50% of all recorded music streams only generate 7% of revenue.

The Spotify per stream rate drops again from .00397 to .00331 a decrease of 16%. Apple Music gains almost 3% for an total global marketshare of about just under 25% of all revenue.

Apple’s per stream rate drops from .00783 to .00495 a decrease of 36%. We need to state again, that 2018 saw a massive shift of revenues from downloads to streaming and no doubt this expansion of scale, combined with more aggressive bundling (free trials) as well as launching into more territories was bound to bring down the overall net per stream.

Apple Music still lead in the sweet spot with about 10% of overall streams generating 25% of all revenue (despite the per stream rate drop). Spotify by comparison has nearly triple the marketshare in streams than Apple Music but generates less than double the revenues on that volume.

The biggest takeaway by far is that YouTube’s Content ID, (in our first truly comprehensive data set) shows a whopping 48% of all streams and only 7% of revenue. Read that again. This is your value gap. Nearly 50% of all recorded music streams only generate 7% of revenue. Apple Music and Spotify combined account for just short of 40% of all streams and 74% of all revenue.

We don’t know how the powers that be at the major labels can continue to allow for this gross inequity. It will be interesting to see how YouTube Red numbers evolve over this year. YouTube Red, the newly rebranded version of the disastrous “Music Key” is off to a slow start in a competitive subscription music marketplace. One has to ask, what incentive is there really for Google/YouTube with the Red subscription service when they already benefit from service 48% of all streams while paying only 7% of the overall revenue?

In looking at the per stream rates for song and album, you might want to read this article by Billboard on the current calculation of how many streams equal and album for the purposes of charting. We don’t know if YouTube Content ID streams count towards charting, but they absolutely should not. The report states that, “The Billboard 200 will now include two tiers of on-demand audio streams. TIER 1: paid subscription audio streams (equating 1,250 streams to 1 album unit) and TIER 2: ad-supported audio streams (equating 3,750 streams to 1 album unit).”

In the coming year Amazon’s Unlimited Music service shows promise. We also wonder about Google Play. The payouts on Google Play are fair, but when bundled into the YouTube ecosystem is largely inconsequential in terms of both streams served and revenue. As smart home assistants grow there could be a larger market segment for paying subscribers to have streaming music catalogs available and on demand.

These numbers are from one set of confidentially supplied data for global sales. If you have access to other data sources that you can share, we’d love to see it.

HOW WE CALCULATED THE STREAMS PER SONG / ALBUM RATE:

As streaming services only pay master royalties (to labels) and not publishing, the publishing has to be deducted from the master share to arrive at the comparable cost per song/album.

$.99 Song is $.70 wholesale after 30% fee. Deduct 1 full stat mechanical at $.091 = $.609 per song.

Multiply the above by 10x’s and you get the album equivalent of $6.09 per album

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

“[A]s you begin to act in harmony with nature the Law garottes & strangles you – so don’t play the blessed liberal middleclass martyr – accept the fact that you’re a criminal & be prepared to act like one.”

Hakim Bey from “T.A.Z.: The Temporary Autonomous Zone, Ontological Anarchy, Poetic Terrorism”

YouTube’s CEO Susan Wojcicki is frantically wheeling around Europe this week in a despairing effort to establish a US-style safe harbor in Europe and undermine Article 13, the Copyright Directive for a Digital Single Market.

Let’s understand that the very concept of a safe harbor for YouTube has its roots deep in the pirate utopias of Internet culture–a fact that may get overlooked if you aren’t a student of the Silicon Valley groundwater.

The Value Gap really owes its origins to the anarchist Peter Lamborn Wilson who wrote the seminal text on pirate utopias under the nom de plume“Hakim Bey” entitled “The Temporary Autonomous Zone, Ontological Anarchy, Poetic Terrorism” (1991) or, as it is known perhaps affectionately in hacker circles, simply “TAZ.” I for one am not quite sure what makes “poetic terrorism” different from unpoetic terrorism, utopian terrorism, anarchic terrorism, or just plain old terrorism, but it may explain why YouTube just can’t bring itself to block terrorist videos before they find an audience.

But the TAZ helps illuminate my own more truncated term for the Value Gap–the alibi. An alibi for a pirate utopia where the pirates run cults called Google and enrich themselves from the prizes they go a-raiding.

In the early days of online piracy there was a fascination with locating servers in some legal meta-dimension that would be outside of the reach of any law enforcement agency. Sealand, for example, captured the imagination of many proto-pirates, but Sealand is a little to clever to put themselves in a position requiring evacuation by the Royal Navy before the shelling begins. So Sealand was ruled out.

Instead, Google–largely through YouTube–created its own pirate utopia through manipulation of the DMCA safe harbor, one of the worst bills ever passed by the U.S. Congress–and that’s saying something. Google busily set about establishing legal precedents that would shore up the moat around their precious TAZ. None of Google’s attacks on government should be surprising–anarchy is in their DNA. As former Obama White House aide and Internet savant Susan Crawford tells us:

I was brought up and trained in the Internet Age by people who really believed that nation states were on the verge of crumbling…and we could geek around it. We could avoid it. These people were irrelevant.

And “these people” were stupid enough to give a safe harbor to protect the TAZ. Because here’s the truth–the safe harbor that has made Google one of the richest companies in the world while they hoover up the world’s culture actually is the quintessential temporary autonomous zone. It only exists in a changeable statute and the judicial interpretations of that statute, whether the DMCA or the Copyright Directive. And like HAL in 2001: A Space Odyssey, they’re not going to allow that disconnection without a fight.

But YouTube’s CEO Susan Wojcicki will not be singing “A Bicycle Built for Two” as she flails about in the disconnect of YouTube. Her basic argument is that “imposing copyright liability is destructive of value” for “open platforms” like YouTube. “Open platforms” bear a striking resemblance to the TAZ, yes? Ms. Wojcicki , of course, purveys a counterintuitive fantasy because unauthorized uses for which copyright liability accrues is what destroys the value of the infringed work. What Ms. Wojcicki is harping about is how copyright infringement destroys value for YouTubeand its multinational corporate parent, Google. This is what happens when stock options invade a pirate utopia.

Not only has she got it wrong, but what she is actually whingeing about is the threat posed to her YouTube pirate utopia by the Copyright Directive and the united creative community. And as HAL might say, the YouTube mission is too important for me to allow you artists to jeopardize it.

You must be logged in to post a comment.