I have it on good authority from someone close to the talks not authorized to speak on the record that Universal is taking the lead on solving the now un-frozen mechanicals crisis. This obviously needs to be confirmed and may not be final, but I think it’s well worth posting about.

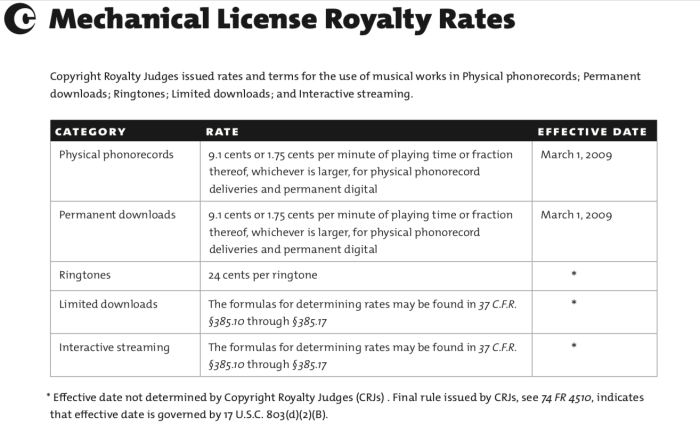

Recall that the crisis pertains to the so-called “Subpart B” mechanical royalties paid by record companies for permanent downloads, vinyl and compact discs. The mechanical rate has been frozen at 9.1¢ since 2008 and the Copyright Royalty Judges recently rejected a settlement among the NMPA, NSAI, Sony, Universal and Warner to extend the freeze in the Phonorecords IV proceeding. Having rejected the proposed settlement, the next step could be knock down, drop dead, drag out litigation that would, in my view, be totally unnecessary. Or the next step could be the labels and publishers submitting a new proposed settlement and asking for the Judges’ approval.

Also recall that the Judges hinted at a potential deal they would like to see in their rejection of the proposed settlement that would essentially uplift the current 9.1¢ rate by an inflation factor since the rate was set in 2008, bringing the minimum statutory rate for all “Subpart B” configurations to 12¢ that would be further uplifted by an annual cost of living adjustment based on the Consumer Price Index (CPI-U in this case).

We’ve written about this topic so much that you’re probably sick of hearing about it–but if this source turns out to be correct, it’s a real step in the right direction by Universal taking a leadership role that will no doubt be controversial.

As I understand it, Universal may propose a minimum statutory rate of 10¢ for permanent downloads and 12¢ for both vinyl and CD configurations. All three rates would be adjusted annually by the Consumer Price Index (in a similar way that the Judges just indexed the webcasting royalty in Webcasting V applicable to sound recordings). This rate would apply to all songs–not just to George Johnson–as one would expect.

There’s no way to know at this point today whether all the participants in the Phonorecords IV proceeding will accept these terms, including George Johnson who has held out for a much higher minimum statutory rate. Some may scratch their head over why the download rate is less, but my suspicion is that it’s because Apple and Amazon have been inflexible on increasing the wholesale price and I could understand why a label would give themselves some headroom on downloads going into what will surely be highly inflationary times but at the same time agreeing a cost of living adjustment. (When the dust settles, it may be worth a discussion in the artist rights community about whether to campaign against Apple and Amazon.)

I do think it’s commendable if Universal is taking the first step toward bringing fairness to a process that has been unfair for many years. We’ll see what happens, but it looks like it could be light at the end of the tunnel. Watch this space.

Getting discovered in the music business has never been easy. Before the pandemic, artists could at least rely on the industry’s historic mainstay to break through — playing as many gigs as possible and hoping to build a following. But with that path closed for now, artists and their label partners are increasingly dependent on Spotify, the undisputed king of music streaming, and its black box algorithms.

That’s why Spotify’s cynical decision to use this moment to launch a new pay-for-play scheme pressuring vulnerable artists and smaller labels to accept lower royalties in exchange for a boost on the company’s algorithms is so exploitative and unfair. Artists must unite to condemn this thinly disguised royalty cut, which apparently has just been released in “beta” mode and is soon expected to enter the market in full force.

Great reporting on the frozen mechanicals debacle at the Copyright Royalty Board by Tim Ingham in Music Business Worldwide. It’s in-depth and really covers all the issue in this must-read explainer!

Nice post by Ed Christman in Billboard explaining the continuing crisis on frozen mechanicals. Ed comes up with a rough justice quantification of the impact on songwriter and music publisher revenues in light of controlled compositions clauses in recording contracts that apply to (a) songs written and recorded by artists, or (b) songs by “outside writers” if and only if the artist can get the outside writer to accept the controlled compositions terms and rates.

For those reading along at home, one theory (aside from sheer leverage) that gets used in this context is that the artist/writer can agree on behalf of all co-writers to accept the terms of the license granted by the artist to the label in the controlled compositions clause because they are co-owners of an undivided interest in the song copyright and can grant nonexclusive licenses in the whole subject to a duty to account provided the license is not economic waste or self-dealing. Let’s just leave all that where it lays for now, but that story has never really been properly challenged–particularly the economic waste part given the rate fixing date issue and even the frozen mechanicals crisis itself. We’ll come back to that bit some other time.

The rate fixing date is a key part of the discussion for understanding the impact of unfreezing mechanicals. So what is that rate fixing provision?

Remember, the controlled compositions clause starts with reducing the minimum statutory mechanical rate in the US (and in theory in Canada subject to MLA) in effect at a point in time. That point in time is either commencement of recording (booo!), delivery, release or sale of a unit embodying the song at issue. Remember that the labels only pay mechanical royalties on physical and downloads (the rates at issue in the frozen mechanicals crisis)–streaming services pay for the interactive streaming mechanicals (and there is no mechanical for webcasting, a whole other beef).

You say, wait–isn’t the mechanical rate 9.1¢? Why does it matter when the record was recorded, delivered, released or sold? Won’t the rates all be the same? And you’d be right if you were asking about a record recorded and released in 2006 or after, or a record recorded and released between 1909 and 1978, like, say some titles by Bob Dylan, The Beatles, Otis Redding or Miles Davis.

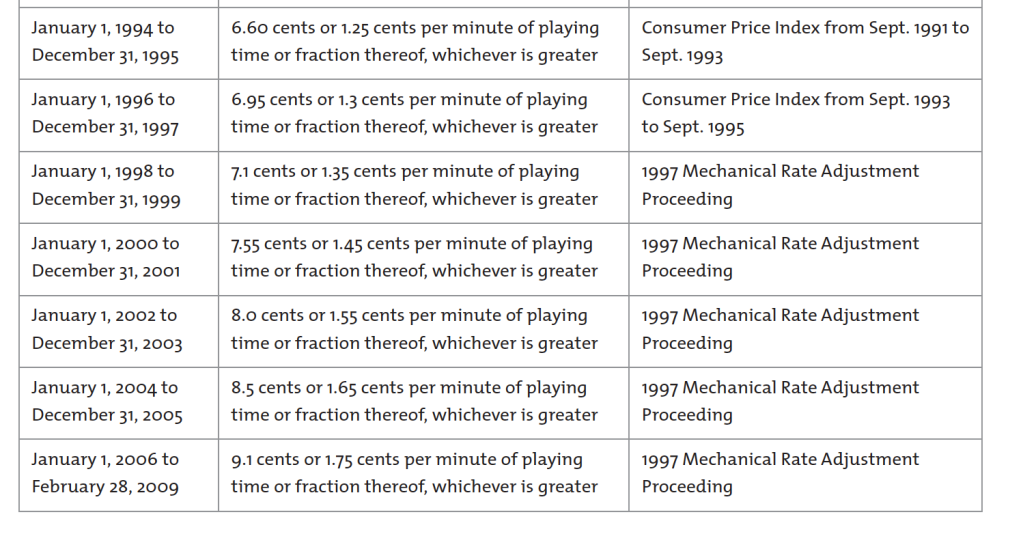

But–it wasn’t always this way. The mechanical royalty rate was set at 2¢ by Congress with the first statutory license, i.e., compulsory license, in 1909 and did not change until the 1976 revision of the US Copyright Act effective 1978. The rate then began to incrementally increase over the years until it reached 9.1¢ in 2006, a phased increase that was to compensate for Congress failing to increase the rate for 70 years, aka “the Ice Age”. The Congress really screwed up songwriters’ lives by freezing the rate at 2¢ during the Ice Age and songwriters and their heirs have been paying for it ever since, right up to the 2006-2022 period, aka “the Second Ice Age” or the Return of the Neanderthals.

In an effort to help songwriters shovel out from the Ice Age, The Congress also authorized indexing the minimum rate to inflation from 1988 to 1995. Indexing is again on the mind of the Copyright Royalty Board right now–bearing in mind that an increase in rates due to inflation has nothing to do with the intrinsic value of the song copyrights so there’s no confusion. Indexing simply applies any increase in the consumer price index to the statutory rate and preserves buying power. In a way, it is the opposite of a case about value. Indexing assumes that the value issue was already decided (in this case in 2006) and simply preserves buying power so that the “nominal” rate of 9.1¢ in 2006 can still buy the same amount of goods or services in 2022 (or 2023 in the case of the CRB rate period). Otherwise the “real” rate, i.e., the inflation adjusted rate, is not 9.1¢ it is about 6¢.

Remember–the proposed rate increase to 12¢ by the CRB is not about value, it’s about buying power because it’s solely focused on inflation.

So back to controlled compositions. It is no coincidence that at the same time as the 1978 increases were phased in, the labels established controlled compositions clauses that knocked songwriters back down. They would probably not have gotten away with freezing by contract at 2¢ so they let the rate float up but much more slowly and with several caps. The first cap is the maximum number of songs, usually 10 or 11. The next cap is the infamous 3/4 rate, where the label pays based on 75% of the minimum statutory rate. But the third cap is the rate fixing date and that’s the one we want to focus on in the unfrozen mechanicals context.

In simple form, it looks something like this contract language:

If the copyright law of the United States provides for a minimum compulsory rate: The rate equal to seventy-five percent (75%) of the minimum compulsory license rate applicable to the use of musical compositions on audio Records under the United States copyright law (hereinafter referred to as the “U.S. Minimum Statutory Rate”) at the time of the commencement of the recording of the Master concerned but in no event later than the last date for timely Delivery of such Master (the applicable date is hereinafter referred to as the “Copyright Fixing Date”). (The U.S. Minimum Statutory Rate is $.091 per Composition as of January 1, 2006);

The way that the statutory rate increases come into the controlled compositions clause is because from 1978-2006 the statutory rates increased across albums delivered across album cycles. If you consider that the rates used to increase about every two years and that an album cycle can be two years, it’s likely that LP 1 would have a lower rate than LP2, LP 2 than LP3 and so on right up to 2006.

Also remember that the increases in rates are prospective, meaning that the controlled compositions rate on recordings delivered in the future will, of course, get the higher rate, even if the past rates don’t change which they don’t, at least not yet. Also consider that permanent downloads often are excluded from controlled comp treatment and are paid at full rate, probably on the rate fixing date in the artist’s agreement. Sometimes the download rates “float” or increase in line with increases in the statutory rate, but that’s part of individual negotiations.

If there is an outside songwriter who does not agree to accept the artist’s controlled composition rate (and there are plenty of these) what happens? Typically the label will account to the outside writer at their full minimum statutory rate but will deduct that payment from the maximum aggregate mechanical royalty payable to the artist (i.e., the 10 song cap). There’s some twists and turns to this involving rates on different units “made and distributed”, but for our purposes there is one clear thing to understand:

Because of the rate fixing date which is frozen by contract (the Mini Ice Age) the artist/songwriter will be paying a higher mechanical to the outside writer from a frozen royalty “pool”.

This is why you should always, always demand “protection” for at least one outside song in your contract and then review each album to determine if that needs to be increased. This is particularly true for records made in places like Nashville where the record company will demand you work with “A” list songwriters (assume none of whom will take 3/4 rate) and then try to deduct the difference between the uncontrolled rate and the controlled rate from you (and if it gets big enough, cross it to your record royalties). (Not only will A list writers not take the 3/4 rate, they’re pissed because they can’t charge you double stat like they do double scale for sessions.)

Example: You have a 10 x 3/4 rate cap on mechanicals, the “cap rate”. That’s the 68.25¢ album rate you hear about (10 x .75 x 9.1¢). Say you have 10 songs on your album and you wrote all of them. You get the entire 68.25¢. If you had two outside songs whose writers get 9.1¢ under current rates, you deduct 18.2¢ from the cap rate, and that leaves 50.05¢ as the “controlled pool” or the total mechanical royalty payable to the artist/songwriter (actually all controlled writers, but leave aside that wrinkle).

So you can see, that’s no longer a 75% rate, it’s actually more like a 55% rate.

Now let’s assume that the new rate is 12¢. Same calculation, two outside songs now get 24¢, but the cap rate stays the same because of the rate fixing date. During the Mini Ice Age, i.e., while that cap rate is fixed at 9.1¢ x 10 x .75, the controlled pool now is expressed as 68.25¢ – 24¢ = 44.25¢, or about 48% (44.25 ÷ 91). The artist’s publisher is not going to be wild about that; the outside writer’s publishers will be thrilled.

This will start to true up on the next LP that takes a rate fixing date after the 12¢ rates go into effect. In that situation you’d be increasing both sides of the equation, so the cap rate would increase to 90¢ (10 x .12 x .75). The outside writers still get 12¢ each for two songs (or 24¢) which is deducted from the cap rate to get a controlled pool of 66¢. The true controlled comp rate is then back to about 55%.

These effects will be less pronounced if you have protection for one or more songs (or fractions of songs) or you have a higher cap, say 11 or 12 instead of 10 (with corresponding increases on other configurations). But you see the trend line.

I think this leads to the conclusion that increasing the statutory rate is a huge step forward and we should all be grateful to the Judges. The rate fixing dates for catalog titles (really the entire rate fixing date concept) must also be considered and any new effort to tweak the controlled compositions clause to effectively nullify the Judges’ rate increase will no doubt cause further conflict.

One day Congress will again act to reduce the effects of the controlled compositions clause and especially the rate fixing date, but in the meantime the Judges may well visit the issue to the extent they are able before we see the Return of the Neanderthals.

There are some decades in which nothing happens and some weeks in which decades happen. This was one of those weeks. You no doubt have seen that the Copyright Royalty Judges offered a breath of fresh air in the contentious and labyrinthine Phonorecords III and IV proceedings by refusing to accept the insider “settlement”…but if mechanical royalties have been understated, what does it mean for catalog valuations in the past and in the future? Looking at you, Bob Dylan!

“The law, in its majestic equality, forbids rich and poor alike to sleep under bridges, to beg in the streets, and to steal their bread.”

Anatole France

It’s hard to believe, but the major labels have filed an “emergency motion” at the Copyright Royalty Board asking the Judges to “clarify” their historic rejection of the insider deal to extend the freeze on physical mechanical royalties for songwriters that many have criticized as being flat out corrupt (and the Judges certainly hinted at it, smoke and fire being what they are). I don’t know about that, but what they seem to really mean is for the Judges to limit the rejection to George Johnson because he’s the only songwriter in the Phonorecords IV proceeding–like that will help them–but screw every other songwriter in the world, and indie label, too, for that matter.

Look, everyone is entitled to a hail mary, but the labels are essentially asking the Judges to say “just kidding” about their rejection of the insider deal. I must say that it’s kind of hard to follow the pretzel logic in places, but one point was very, very clear and it is this:

Nor would there be any basis for the Judges to reject the Settlement as to non-participants [that would be every songwriter except George]. Non-participants take a calculated risk when they choose to sit out a proceeding. Specifically, they decide that to save the expense and burden of participating in a proceeding, they will live with the outcome of the proceeding whatever it is. In particular, just as a dissatisfied non-participant [that would be you and me] cannot seek appellate review of the outcome of a rate proceeding, non-participants may not object to any settlement reached by those who are prepared to undertake the expense and burden of participation. [Well judging by the uniformly negative public comments lots of people including me did not get that memo.] Thus, while Congress has authorized the Judges to decline to adopt a settlement as to an objecting participant, it expressly did not authorize the Judges to decline a settlement as to non-participants who, by definition, have chosen to allow the participants to reach an agreement on their behalf. In so doing, Congress reasonably chose to promote participation in proceedings while also giving settlements broad effect.

Guys, guys, guys…there are a lot of ways you could have said this, but why on Earth you chose this one is beyond me. By definition, non-participants have chosen to allow the participants to reach an agreement on their behalf? Really? Really? By whose definition? I’m sorry, but that just does not pass the laugh test.

And are they really saying that the preferred outcome–promoted by Congress, no less–is to have every songwriter and independent label in the world crammed into the Copyright Royalty Board’s hearing room? Do they really want a line out the door and around several blocks? Because if that’s really what they want, maybe that could be arranged in Phonorecords V. But we also may see real scorched earth litigation ensue here if the Judges refuse to reverse themselves instead of making lemonade out of lemons.

Actually, Congress did not charge the well-heeled major label and publisher participants to look out for the interests of nonparticipants. (Almost sounds like…gasp…a fiduciary duty, don’t it?) You know who Congress does charge with that obligation as true blue fiduciaries?

The Judges. That’s their job. And the Judges showed up for work, rejected the insider deal, and did their job just as they are supposed to in order to preserve equal justice under law.

[If you want to tell the Copyright Royalty Board what you think, try crb@loc.gov]

It was a big week for songwriters last week! The Copyright Royalty Judges rejected the frozen mechanicals settlement put forward by the majors in the current rate-setting proceeding at the Copyright Royalty Board thanks in part to the best audience in the world–that would be you! All that hammering on the issue paid off.

We also acknowledge the hard work of all the commenters who spoke straight from the heart and of course songwriter George Johnson who has been fighting the good fight in the Copyright Royalty Board all by himself for years now. We’re also very grateful to the Judges for a well-thought out ruling and a thorough vetting of the issues, George’s many filings and the songwriter public comments.

The question we’ve heard a lot in recent days is where do we go from here? Clearly the answer is “Up” but how far up is the question. We need to be mindful of the economic impact that increased rates will have on independent labels in particular, but at the same time acknowledge that all record companies have gotten the benefit of frozen rates for 16 years and that songwriters have taken it in the shorts for a long, long time.

The Judges seem to be hinting at a deal in their ruling (remembering this is the rate for physical and downloads only (called “Subpart B rates”) and not for Spotify-type streaming which is not affected by these rate changes). Here’s the relevant quote from the ruling:

Commenters advocated application of an inflation adjustment beginning, at a minimum, in 2006. See, e.g. [Songwriters Guild of America] Comments at 4; [Monica] Corton Comments at 4; [Kevin] Casini Comments at 4. According to the proponents of a cost of living adjustment (COLA) applied to the 2006 rates, that adjustment would yield a 2021 royalty rate of $ 0.12 (an upward 31.9% inflation adjustment over the sixteen-year period). See, e.g., SGA Comments at 4. SGA conceded that the COLA extrapolation cannot be considered dispositive on the issue of new rate-setting, but they contended that it does “starkly demonstrate the outrageous unfairness that has been imposed on the music creator community over a period of more than an entire century.”

Step one, then, could be to increase the minimum statutory rate to 12¢ (or 13¢ depending on how you do the math) with customary adjustments for the “long song” formula for songs over 5 minutes.

That increase in the rate would be significant and probably the biggest rate increase ever on a percentage basis for the statutory rate. Will that satisfy everyone? Probably not, but it’s a step forward.

But–and this is a big but–that’s not the end of the story. We do not want to be right back in the same position in a few years time. One way to avoid this is to increase the new rate for inflation every 12 months (called “indexing”) the same way that the webcasting rates are indexed for sound recordings.

The Judges also hint at indexing as a potential solution to avoid just another rate freeze:

[George Johnson] has long advocated inclusion of an inflation index in royalty rates set by the Judges, including the…rates at issue here. In support of his advocacy, GEO has filed 27 pleadings, including motions seeking imposition of an inflation index on section 115 rates and periodic notices of U.S. inflation rates. His plea is bolstered by the many commenters who, almost unanimously, included this suggestion.

So the way this would work is that starting in 2023, the current 9.1¢ rate would be increased to 12¢. After 12 months, the rate would be increased by the Consumer Price Index (the CPI-U rate) for each 12 month period until 2027 when new rates would get decided by the CRB in the next rate proceeding (Phonorecords V). Example: If the CPI is 10%, then the minimum statutory rate would increase to 13.2¢ for the next 12 months. If the CPI in the second year was also 10%, then the 13.2¢ rate would be increased to 14.52¢ and so on until the last year of the period (2027). (Of course we can’t tell today what the CPI will be in 2023.)

Given the Judge’s rejection of the frozen rates, it is very doubtful that there will ever be another freeze, but we have to stay alert and vocal. When the new rates come up, we all have to pay attention.

It’s important to remember that “indexing” to inflation just preserves buying power. Meaning that 12¢ today is what 9.1¢ was worth in 2006. Would it be the fair thing to index all the way back to 1909? Sure, but while the Judges hint at going back further (the “at a minimum” reference), the Judges may not be inclined to go further back than 2006 when the current freeze started, but we’ll see what happens.

We’d be very interested in hearing from you with any questions you have or other ideas for solutions. Obviously, this post is just sharing ideas with our audience and isn’t a formal statement by any particular person or group. There may be a number of proposals coming out and we’ll of course post them on Trichordist.

It must also be said that George Johnson has yet to weigh in on the situation and may very well have a different idea. There’s also some twists and turns to sort out, such as the black box “MOU” (the fourth of its name) but especially the controlled compositions rates that the Judges discussed in some detail (as Judge Barnett said, “The disparity between the static rate and the dynamic market is even more stark when considering the “controlled composition clause.””).

In any event, feel free to comment and we welcome the discussion.

The upshot of the Judges’ ruling rejecting the extension of the frozen rates is that both George Johnson as a participant and a host of commenters brought up many valid points about problems with the settlement. I suppose the next step will be for the Judges to either set rates themselves and let the parties react to them or ask the parties to resubmit a new proposal in line with the Judge’s ruling.

Either way, the settlement is rejected and we have to thank the Judges who listened thoughtfully, George Johnson who toils alone representing himself (and the independent songwriter’s view) as an actual participant in the proceeding, and all the songwriters, independent publishers, lawyers and songwriter groups who took the time to comment. And of course a huge thank you to all the Trichordist readers who supported fairness and justice and all the heartfelt comments against frozen mechanicals.

The wheels of justice turn slowly, but they do turn. Don’t forget it–the price of liberty is eternal vigilance.

Here is the Judges conclusion:

Rightsholders are free to choose their representation in these proceedings. Admittedly, individual songwriters and self-publishers have traditionally chosen not to expend the resources necessary to participate in these proceedings at the same level as trade organizations and major technology companies. Nonetheless, the outcomes of these proceedings can have a significant impact on the lives of the individual rightsholders. In this proceeding, the Judges received lengthy comments from SGA, which claims to represent thousands of songwriters. For SGA’s comments to have independent influence, however, SGA would have needed to join the proceeding as a participant. Nonetheless, with regard to the present proposed settlement, the comments of non-participants cumulatively served to amplify those of the objecting participant.

Pursuant to section 801(b)(7)(A)(ii), based on the totality of the present record—including the Judges’ application of the law to that record, as well as GEO’s objections, which, as noted supra, are consistent with the non-participant comments—the Judges find that the proposed settlement does not provide a reasonable basis for setting statutory rates and terms. Furthermore, the Judges find a paucity of evidence regarding the terms, conditions, and effects of the MOU. Based on the record, the Judges also find they are unable to determine the value of consideration offered and accepted by each side in the MOU. These unknown factors, as highlighted in the record comments, provide the Judges with additional cause to conclude that the proposed settlement does not provide a reasonable basis for setting statutory rates and terms.

We’ve all heard the talking points from Big Radio’s shillery the National Association of Broadcasters about how it’s perfectly fine for American radio stations to deny recording artists and session musicians fair compensation–because exposure, don’t you know. Big radio delivers huge audiences for music and we should all be grateful and work for free for the ever-more-consolidated broadcasting industry.

The other talking point we don’t hear so much from these characters is that media ownership rules are bad and that greater and greater concentration of influence and wealth to control the public airwaves is good. That’s right, it’s not the corporate airwaves, it’s the public’s airwaves. But you wouldn’t know that by looking, right?

So the latest version of this “bigger is better” guff is happening right now at the Federal Communications Commission that licenses radio stations. The NAB is poormouthing to the FCC about how radio and TV stations have trouble competing with Google and Facebook (in particular) for advertising. Oh, no. Google is grinding them into bits? Say it ain’t so!

We know a little bit about what it’s like to have soulless Silicon Valley oligarchs using their political and financial muscle to get a free pass to jack with your livelihood without repercussions from the guys with badges. If Big Tech is really the problem for Big Radio, I’m sure there would be some support for going after them together. But playing nice with others would require the soulless media oligarchs to stop acting like wankers and make a fair deal for artists and musicians. That is not happening. No, no, the solution to the broadcasters’ Google problem is to relax media ownership rules for even MORE concentrated radio ownership, you see. Plus these monopolists want an antitrust exemption for which they have presented no evidence other than even more shillery.

But see what they did there? MusicFirst certainly did and wrote to the FCC to make sure the FCC did, too (letter is here):

The National Association of Broadcasters, in seeking relaxed broadcast radio ownership rules, is asking the FCC to accept arguments directly contrary to those it makes in opposing the American Music Fairness Act.

In fighting the AMFA, the NAB continues to claim airplay has “promotional value” that eliminates the need for radio broadcasters to pay recording artists for the music the stations use to derive millions of advertising dollars. The promotion argument has never been a valid justification for refusing to pay musicians. Such a rationale could swallow all of copyright, as any use of content can be called “promotional.” But even the NAB’s own arguments before the FCC are showing the flaws with its promotion claim.

For example, the NAB argues in this proceeding that radio broadcasters need increased economies of scale to compensate for the significant audience share broadcast radio has lost. Yet, if radio broadcasters have lost so much audience share that they need government intervention, the promotional value they claim to provide recording artists cannot be adequate compensation.

The NAB also applies the promotion claim inconsistently. In addition to its argument about loss of broadcast radio audience, the NAB alleges here that broadcasters need increased economies of scale because online platforms refuse to fairly compensate broadcasters for content the platforms use to derive advertising revenue. The NAB is similarly arguing that platforms’ inadequate compensation warrants passage of the Journalism Competition and Preservation Act [the antitrust exemption for monopolists].

The musicFIRST Coalition agrees with the NAB that distributors should adequately compensate content providers. But what is good for the goose must be good for the gander. Online distribution of broadcaster content can also be claimed to be promotional. If the NAB finds inadequate the combination of online promotion and the money online platforms do pay broadcasters, the alleged value of broadcast radio promotion combined with the lack of any money the radio broadcasters pay recording artists cannot possibly be adequate.

The shills at the NAB should try being reasonable just once instead of doing their usual blunt force trauma. Here’s the reality: Nobody is buying what they’re selling because it’s just more snake oil.

If you’ve tried to get a vinyl record pressed in the last few years, one thing is very obvious: There is no capacity in the current manufacturing base to accommodate all the orders–unless your name is Adele or Taylor Swift, of course. If that’s your name, as if by magic you get your vinyl orders filled and shipped on time.

Jack White spotted the vinyl trend early on–in 2009–and is filling the gap through his Third Man pressing operations. But Jack is calling on the major labels to please compete with him–rather unusual–because it’s the right thing to do in order to meet the demand for the benefit of the consumer. And the elephant in the room of this discussion is that we don’t really have any idea what the vinyl sales would be because demand is not being met by supply.

Not even close.

When a major label abandons a configuration, it’s not really abandoned. It gets outsourced to an independent and as long as there is manufacturing capacity in the system, that independent still takes orders and fulfills those orders by using that manufacturing capacity. The titles still appear in the sales book, orders get taken and returns accommodated.

Major labels also hand off vinyl manufacturing to their “special markets” divisions. For example, if you have ever tried to get vinyl manufactured in a limited run for venue sales on a major label artist (or former major label artist) you will get put through the bureaucratic torture gauntlet for the privilege of paying top dollar on a product that the label will have nothing to do with selling.

But even so, at some point that manufacturing capacity begins to shrink because the majors are getting out of the configuration and they will eventually get out of the manufacturing business altogether. And that creates a great sucking sound as capacity tanks.

I raised this problem in comments to the Copyright Royalty Board about the frozen mechanicals debacle where the smart people have tried to extend the 2006 songwriter rates on vinyl and CDs without regard to rampant inflation and simply the value of songs to sell millions of units. Why? Because vinyl and CDs don’t matter according to the lobbyists. This is, of course, bunk.

The fact is–and Jack White’s plea illuminates the issue–we don’t know what the sales would be if the capacity increased to meet demand. But we do know that sales would be higher. Probably much higher.

You do see entrepreneurs entering the space using new technology. Gold Rush Vinyl in Austin is a prime example of that phenomenon. The majors need to reconsider how to meet demand and keep the consumer happy. They also need to clean up the sales and distribution channel so that it’s easy for record stores to actually get stock, which, frankly is a joke.

Why anyone wants to substitute away from high margin physical goods to low margin streaming goods with a “rich get richer” financial model is a head scratcher. Although maybe I answered my own question.

But–as Trichordist readers will recall, the major publishers and major labels as well as the Nashville Songwriters Association are trying to convince the Copyright Royalty Board that vinyl and CDs are not important and that songwriters should have their mechanical royalty rates frozen again. You do have to ask if Jack White is even aware that the major publishers and major labels are trying to get the Copyright Royalty Board to extend the 2006 freeze on mechanicals for the resurgent vinyl configuration for another five years.

Vinyl and CDs still account for about 15% of revenue on an industry wide basis–I’ll believe that it’s not significant when Lucian Grange says he doesn’t need 15% of billing. Yeah, that will happen.

The only reason that mechanicals for those configurations aren’t higher is because they have been artificially suppressed by the participants at the Copyright Royalty Board telling the judges that the revenue is low so please freeze the rates again. Kind of circular, yes? The current 2006 rate of 9.1¢ would be adjusted to 13¢ in current dollars just taking into account inflation and ignoring the value of the songs to create a nearly vertical chart like this:

You must be logged in to post a comment.