Snoop Dogg had strong words for Spotify, Apple Music, and other music streaming services during an interview with former Apple Music Creative Director Larry Jackson at the Milken Institute Global Conference.

“I know I’m going off-script right now, but fuck it. This is business,” said Snoop “In a room full of business people and somebody may hear this so the next artist don’t have to struggle and cry for his money because some of these artists are streaming millions and millions and millions and millions of fucking streams and they don’t got no millions of dollars in the pot.”

Spotify has one big governance problem that permeates its governance like a putrid miasma in the abattoir: “Dual-class stock” sometimes referred to as “supervoting” stock. If you’ve never heard the term, buckle up. I wrote an extensive post on this subject for the New York Daily News that you may find interesting.

Dual class stock allows the holders of those shares–invariably the founders of the public company when it was a private company–to control all votes and control all board seats. Frequently this is accomplished by giving the founders a special class of stock that provides 10 votes for every share or something along those lines. The intention is to give the founders dead hand control over their startup in a kind of corporate reproductive right so that no one can interfere with their vision as envoys of innovation sent by the Gods of the Transhuman Singularity. You know, because technology.

Google was one of the first Silicon Valley startups to adopt this capitalization structure and it is consistent with the Silicon Valley venture capital investor belief in infitilism and the Peter Pan syndrome so that the little children may guide us. The problem is that supervoting stock is forever, well after the founders are bald and porky despite their at-home beach volleyball courts and warmed bidets.

Spotify, Facebook and Google each have a problem with “dual class” stock capitalizations. Because regulators allow these companies to operate with this structure favoring insiders, the already concentrated streaming music industry is largely controlled by Daniel Ek, Sergey Brin, Larry Page and Mark Zuckerberg. (While Amazon and Apple lack the dual class stock structure, Jeff Bezos has an outsized influence over both streaming and physical carriers. Apple’s influence is far more muted given their refusal to implement payola-driven algorithmic enterprise playlist placement for selection and rotation of music and their concentration on music playback hardware.)

The voting power of Ek, Brin, Page and Zuckerberg in their respective companies makes shareholder votes candidates for the least suspenseful events in commercial history. However, based on market share, Spotify essentially controls the music streaming business. Let’s consider some of the implications for competition of this disfavored capitalization technique.

Commissioner Robert Jackson, formerly of the U.S. Securities and Exchange Commission, summed up the problem:

“[D]ual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms [Snap, Inc. and Google Class B shares] have recently issued shares that give ordinary public investors no vote at all.

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression. But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.” Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.

Spotify is the dominant streaming firm and the voting power of Spotify stockholders is concentrated in two men: Daniel Ek and Martin Lorentzon. Transitively, those two men literally control the music streaming sector through their voting shares, are extending their horizontal reach into the rapidly consolidating podcasting business and aspire soon to enter the audiobooks vertical. Where do they get the money is a question on every artists lips after hearing the Spotify poormouthing and seeing their royalty statements.

The effects of that control may be subtle; for example, Spotify engages in multi-billion dollar stock buybacks and debt offerings, but has yet makes ever more spectacular losses while refusing to exercise pricing power.

So yes, Spotify is starting to look like the kind of Potemkin Village that investment bankers love because they see oodles of the one thing that matters: Fees.

On the political side, let’s see what the company’s campaign contributions tell us:

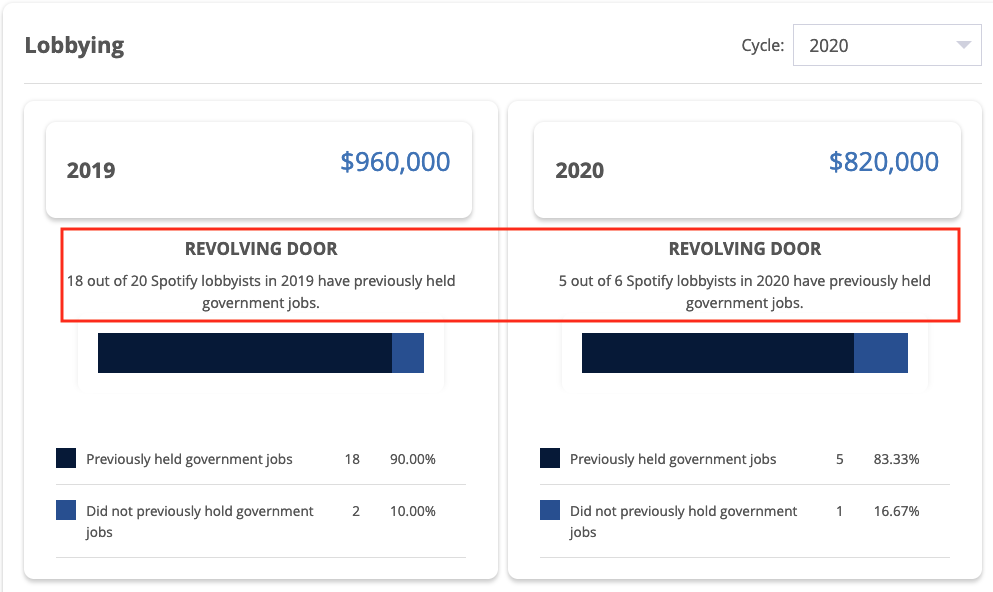

Spotify has also made a habit out of hiring away government regulators like Regan Smith, the former General Counsel and Associate Register of the US Copyright Office who joined Spotify as head of US public policy (a euphemism for bag person) after drafting all of the regulations for the Mechanical Licensing Collective;

Whether this is enough to trip Spotify up on the abuse of political contributions I don’t know, but the revolving door part certainly does call into question Spotify’s ethics.

It does seem that these are the kinds of facts that should be taken into account when determining Spotify’s ESG score. At this point, it looks like Spotify is an ESG fail–which may require divesting by some of the over 600 mutual funds that hold shares.

I started to write this post in the pre-Neil Young era and I almost feel like I could stop with the title. But there’s a lot more to it, so let’s look at the many ways Spotify is a fail on the Social part of ESG.

Before Spotify’s Joe Rogan problem, Spotify had both an ethical supply chain problem and a “fair wage” problem on the music side of its business, which for this post we will limit to fair compensation to its ultimate vendors being artists and songwriters. In fact, Spotify is an example to music-tech entrepreneurs of how not to conduct their business.

Treatment of Songwriters

On the songwriter side of the house, let’s not fall into the mudslinging that is going on over the appeal by Spotify (among others) of the Copyright Royalty Board’s ruling in the mechanical royalty rate setting proceeding known as Phonorecords III. Yes, it’s true that streaming screws songwriters even worse that artists, but not only because Spotify exercised its right of appeal of the Phonorecords III case that was pending during the extensive negotiations of Title I of the Music Modernization Act. (Title I is the whole debacle of the Mechanical Licensing Collective scam and the retroactive copyright infringement safe harbor currently being litigated on Constitutional grounds.)

The main reason that Spotify had the right to appeal available to it after passing the MMA was because the negotiators of Title I didn’t get all of the services to give up their appeal right (called a “waiver”) as a condition of getting the substantial giveaways in the MMA. A waiver would have been entirely appropriate given all the goodies that songwriters gave away in the MMA. When did Noah build the Ark? Before the rain. The negotiators might have gotten that message if they had opened the negotiations to a broader group, but they didn’t so now they’ve got the hot potato no matter how much whinging they do.

Having said that, you will notice that Apple took pity on this egregious oversight and did not appeal the Phonorecords III ruling. You don’t always have to take advantage of your vendor’s negotiating failures, particularly when you are printing money and when being generous would help your vendor keep providing songs. And Mom always told me not to mock the afflicted. Plus it’s good business–take Walmart as an example. Walmart drives a hard bargain, but they leave the vendor enough margin to keep making goods, otherwise the vendor will go under soon or run a business solely to service debt only to go under later. And realize that the decision to be generous is pretty much entirely up to Walmart. Spotify could do the same.

Is being cheap unethical? Is leveraging stupidity unethical? Is trying to recover the costs of the MLC by heavily litigating streaming mechanicals unethical (or unexpected)? Maybe. A great man once said failing to be generous is the most expensive mistake you’ll ever make. So yes, I do think it is unethical although that’s a debatable point. Spotify has not made themselves many friends by taking that course. But what is not debatable is Spotify’s unethical treatment of artists.

Treatment of Artists

The entire streaming royalty model confirms what I call “Ek’s Law” which is related to “Moore’s Law”. Instead of chip speed doubling every 18 months in Moore’s Law, royalties are cut in half every 18 months with Ek’s Law. This reduction over time is an inherent part of the algebra of the streaming business model as I’ve discussed in detail in Arithmetic on the Internet as well as the study I co-authored with Dr. Claudio Feijoo for the World Intellectual Property Organization. These writings have caused a good deal of discussion along with the work of Sharky Laguana about the “Big Pool” or what’s come to be called the “market centric” royalty model.

Dissatisfaction with the market centric model has led to a discussion of the “user-centric” model as an alternative so that fans don’t pay for music they don’t listen to. But it’s also possible that there is no solution to the streaming model because everybody whose getting rich (essentially all Spotify employees and owners of big catalogs) has no intention of changing anything voluntarily.

It would be easy to say “fair is where we end up” and write off Ek’s Law as just a function of the free market. But the market centric model was designed to reward a small number of artists and big catalog owners without letting consumers know what was happening to the money they thought they spent to support the music they loved. As Glenn Peoples wrote last year (Fare Play: Could SoundCloud’s User-Centric Streaming Payouts Catch On?,

When Spotify first negotiated its initial licensing deals with labels in the late 2000s, both sides focused more on how much money the service would take in than the best way to divide it. The idea they settled on, which divides artist payouts based on the overall popularity of recordings, regardless of how they map to individuals’ listening habits, was ‘the simplest system to put together at the time,’ recalls Thomas Hesse, a former Sony Music executive who was involved in those conversations.

In other words, the market centric model was designed behind closed doors and then presented to the world’s artists and musicians as a take it or leave it with an overhyped helping of FOMO.

As we wrote in the WIPO study, the market centric model excludes nonfeatured musicians altogether. These studio musicians and vocalists are cut out of the Spotify streaming riches made off their backs except in two countries and then only because their unions fought like dogs to enforce national laws that require streaming platforms to pay nonfeatured performers.

The other Spotify problem is its global dominance and imposition of largely Anglo-American repertoire in other countries. The company does this for one big reason–they tell a growth story to Wall Street to juice their stock price. In fact, Daniel Ek just did this last week on his Groundhog Day earnings call with stock analysts. For example he said:

The number one thing that we’re stretched for at the moment is more inventory. And that’s why you see us introducing things such as fan and other things. And then long-term with a little bit more horizon, it’s obviously international.

Both user-centric and market-centric are focused on allocating a theoretical revenue “pie” which is so tiny for any one artist (or songwriter) who is not in the top 1 or 5 percent this week that it’s obvious the entire model is bankrupt until it includes the value that makes Daniel Ek into a digital munitions investor–the stock.

Debt and Stock Buybacks

Spotify has taken on substantial levels of debt for a company that makes a profit so infrequently you can say Spotify is unprofitable–which it is on a fully diluted basis in any event. According to its most recent balance sheet, Spotify owes approximately $1.3 billion in long term–secured–debt.

You might ask how a company that has never made a profit qualifies to borrow $1.3 billion and you’d have a point there. But understand this: If Spotify should ever go bankrupt, which in their case would probably be a reorganization bankruptcy, those lenders are going to stand in the secured creditors line and they will get paid in full or nearly in full well before Spotify meets any of its obligations to artists, songwriters, labels and music publishers, aka unsecured creditors.

Did Title I of the Music Modernization Act take care of this exposure for songwriters who are forced to license but have virtually no recourse if the licensee fails to pay and goes bankrupt? Apparently not–but then the lobbyists would say if they’d insisted on actual protection and reform there would have been no bill (pka no bonus).

Right. Because “modernization” (whatever that means).

But to our question here–is it ethical for a company that is totally dependent on creator output to be able to take on debt that pushes the royalties owed to those creators to the back of the bankruptcy lines? I think the answer is no.

Spotify has also engaged in a practice that has become increasingly popular in the era of zero interest rates (or lower bound rates anyway) and quantitative easing: stock buy backs.

Stock buy backs were illegal until the Securities and Exchange Commission changed the law in 1982 with the safe harbor Rule 10b-18. (A prime example of unelected bureaucrats creating major changes in the economy, but that’s a story for another day.)

Stock buy backs are when a company uses the shareholders money to buy outstanding shares of their company and reduce the number of shares trading (aka “the float”). Stock buy backs can be accomplished a few ways such as through a tender offer (a public announcement that the company will buy back x shares at $y for z period of time); open market purchases on the exchange; or buying the shares through direct negotiations, usually with holders of larger blocks of stock.

A stock buyback is basically a secondary offering in reverse — instead of selling new shares of stock to the public to put more cash on the corporate balance sheet, a cash-rich company expends some of its own funds on buying shares of stock from the public.

Why do companies buy back their own stock? To juice their financials by artificially increasing earnings per share.

Spotify has announced two different repurchase programs since going public according to their annual report for 12/31/21:

Share Repurchase Program On August 20, 2021, [Spotify] announced that the board of directors [controlled by Daniel Ek] had approved a program to repurchase up to $1.0 billion of the Company’s ordinary shares. Repurchases of up to 10,000,000 of the Company’s ordinary shares were authorized at the Company’s general meeting of shareholders on April 21, 2021. The repurchase program will expire on April 21, 2026. The timing and actual number of shares repurchased depends on a variety of factors, including price, general business and market conditions, and alternative investment opportunities. The repurchase program is executed consistent with the Company’s capital allocation strategy of prioritizing investment to grow the business over the long term. The repurchase program does not obligate the Company to acquire any particular amount of ordinary shares, and the repurchase program may be suspended or discontinued at any time at the Company’s discretion. The Company uses current cash and cash equivalents and the cash flow it generates from operations to fund the share repurchase program.

The authorization of the previous share repurchase program, announced on November 5, 2018, expired on April 21, 2021. The total aggregate amount of repurchased shares under that program was 4,366,427 for a total of approximately $572 million.

Is it ethical to take a billion dollars and buy back shares to juice the stock price while fighting over royalties every chance they get and crying poor? I think not.

[This is the first in a series of three short posts examining how Spotify scores as an Environmental, Social and Governance (or “ESG”) investment. “ESG” is a Wall Street acronym often attributed to Larry Fink at Blackrock that designates a company as suitable for socially conscious investing based on its “Environmental, Social and Governance” business practices, that is “ESG”. See the Upright Net Impact data model on Spotify’s sustainability score. As of this writing, the last update of Spotify’s Net Impact score was before the Neil Young scandal and, of course, rocketing energy prices that compound the environmental impact of streaming. These posts first appeared on MusicTechSolutions]

Spotify closes $24 higher than its first day of trading after destroying the incomes of thousands of artists and even more songwriters. pic.twitter.com/HeHXnEXVHh

Spotify has an ESG problem, and a closer look may offer insights into a wider problem in the tech industry as a whole. If a decade of destroying artist and songwriter revenues isn’t enough to get your attention, maybe the Neil Young and Joe Rogan imbroglio will. But a minute’s analysis shows you that Spotify was already an ESG fail well before Neil Young’s ultimatum.

Streaming is an Environmental Fail

I first began posting about streaming as an environmental fail years ago in the YouTube and Google world. Like so many other ways that the BIg Tech PR machine glosses over their dependence on cheap energy right through their supply chain from electric cars to cat videos, YouTube did not want to discuss the company as a climate disaster zone. To hear them tell it, YouTube, and indeed the entire Google megalopolis right down to the Google Street View surveillance team was powered by magic elves running on appropriate golden flywheels with suitable work rules. Or other culturally appropriate spin from Google’s ham handed PR teams.

Mission creepy meets the Sound of Music

Greenpeace first wrote about “dirty data” in 2011–the year Spotify launched in the US. Too bad Spotify ignored the warnings. Harvard Business Review also tells us that 2011 was a demarcation point for environmental issues at Microsoft following that Greenpeace report:

In 2011, Microsoft’s top environmental and sustainability executive, Rob Bernard, asked the company’s risk-assessment team to evaluate the firm’s exposure. It soon concluded that evolving carbon regulations and fluctuating energy costs and availability were significant sources of risk. In response, Microsoft formed a centralized senior energy team to address this newly elevated strategic issue and develop a comprehensive plan to mitigate risk. The team, comprising 14 experts in electricity markets, renewable energy, battery storage, and local generation (or “distributed energy”), was charged by corporate senior leadership with developing and executing the firm’s energy strategy. “Energy has become a C-suite issue,” Bernard says. “The CFO and president are now actively involved in our energy road map.”

If environment is a C-suite issue at Spotify, there’s no real evidence of it in Spotify’s annual report (but then there isn’t at the Mechanical Licensing Collective, either). “Environment” word search reveals that at Spotify, the environment is “economic”, “credit”, and above all “rapidly changing.” Not “dirty”–or “clean” for that matter.

The fact appears to be that Spotify isn’t doing anything special and nobody seems to want to talk about it. But wait, you say–what about the sainted Music Climate Pact? (Increasingly looking like a PR effort worthy of Edward Bernays.) Guess who hasn’t signed up to the MCP? Any streaming service as far as I can tell. There is a “Standard Commitment Letter” that participants are supposed to sign up to but I wasn’t able to read it. Want to guess why?

That’s right. You know who wants to know what you’re up to.

If you haven’t heard much about streaming’s negative effects on the environment, don’t be surprised. It’s not a topic that’s a great conversation starter and very few journalists seem to have any interest in the subject at all. I wonder why.

But if you’re an artist who is concerned about the impact of streaming your music on the environment or an investor trying to see your way through the ESG investment, this should give you a few questions to ask about Spotify’s ESG score. And if that slipped by you, don’t feel bad–Blackrock reportedly holds 3.8 million shares of Spotify that are worth less all the time, so they didn’t catch it either. And Blackrock coined the phrase.

Next: Spotify’s “Social” Fail: Rogan, Royalties and The Uyghurs

Mansplaining, anyone? If you remember Spotify’s 2014 messaging debacle with Taylor Swift, we always suspected that the Spotify culture actually believed that artists should be grateful for whatever table scraps that Spotify’s ad-supported big pool model threw out to artists. They were only begrudgingly interested in converting free users to paid subscribers, which still pays artists nothing due to the big pool’s hyper-efficient market share revenue distribution model.

And then there was another one of Spotify’s artist and label relations debacles with Epidemic Sound–Spotify’s answer to George Orwell’s “versificator” in the Music Department that produced “countless similar songs published for the benefit of the proles by a sub-section of the Music Department.”

The common threads of most of Spotify’s crazy wrong turns–and they are legion–is what they indicate: An incredible heartless arrogance and an utter failure to understand the business they are in. A business that ultimately turns on the artists and the songwriters. As long as there is an Apple Music and the other music streaming platforms, artists can simply walk across the street–which is why Taylor Swift could make Daniel Ek grovel like a little…well, let’s just leave it at grovel.

But–this long history of treating artists and especially songwriters poorly is what makes it so important to preserve Apple Music as a healthy competitor to Spotify and the only thing that stops Spotify from becoming a monopolist. A fact that seems entirely lost on their boy Rep. David Cicilline’s anti-Apple bill that “seems aimed directly at Apple and has Spotify’s litigation against Apple written all over it.” (Mr. Cicilline runs virtually unopposed in his Rhode Island elections, which if you know anything about Rhode Island politics is just the way the “Crimetown” machine likes it.)

Why are ostensibly smart people given to such arrogance? Mostly because they are rich and believe their own hype. But never has that reality been on such public display in all its putridness than in a truly unbelievable exchange at the Sync Summit in 2019 in New York between home town independent artist Ashley Jana and former Spotify engineer Jim Anderson who was being interviewed by Mark Freiser who runs that conference (and who doesn’t exactly come off like a prize puppy either).

Ashley recorded the entire exchange in (what else) a YouTube video and Digital Music News reported on it recently. Here’s part of the exchange between Ashley and Mr. Anderson after Ashley had the temerity to bring up…money!

Jana: We’re not making any money off of the streams. And I know that you know this, and I’m not trying to put you on the spot. I’m just saying, one cent is really not even that much money if you add 2 million times .01, it’s still not that much. And if you would just consider —

Anderson: Oh, I’m going to go down this road, you know that.

Interviewer (Mark Frieser): This is really not a road we’ve talked about before, but I’m gonna let him do this —

Jana: Thank you again.

Anderson: Do you want me to go down this road? I’m gonna go down this road.

Frieser: Well, if you need to.

Anderson: Wait, do I go down the entitlement road now, or do I wait a minute?

Frieser: Well, you know what, I think you should do what you need to do.

Anderson: Should we do it now?

Frieser: Yeah, whatever you feel you need to do.

Anderson: So maybe I should go down the entitlement road now? Or should I wait a few minutes?

Frieser: Do you want to wait a few minutes? Maybe take another question or two?

Anderson: [to the audience] Do you guys want to talk about entitlement now? Or do we talk about —

[Crowd voices interest in hearing the answer from Anderson]

Jana: I don’t think it’s entitlement to ask for normal rates, like before.

Anderson: Normal rates?

Jana: No, the idea is to make it a win-win situation for all parties.

Anderson: Okay, okay. So we should talk about entitlement. I mean, I have an issue with Taylor Swift’s comments. I have this issue with it, and we’ll call it entitlement. I mean, I consider myself an artist because I’m an inventor, okay? Now, I freely give away my patents for nothing. I never collect royalties on anything.

I think Taylor Swift doesn’t need .00001 more a stream. The problem is this: Spotify was created to solve a problem. The problem was this: piracy and music distribution. The problem was to get artists’ music out there. The problem was not to pay people money.

You really should listen to the entire video to really comprehend the arrogance dripping off of Mr. Anderson’s condescension.

The Rolling Stones, Pet Shop Boys, Emeli Sandé, Barry Gibb, Van Morrison, Sir Tom Jones and the Estates of John Lennon and Joe Strummer have written to the Prime Minister “on behalf of today’s generation of artists, musicians and songwriters here in the UK”.

In an unprecedented show of solidarity, they have added their names to a joint letter with artists such as Annie Lennox, Paloma Faith, Kano, Joan Armatrading, Chris Martin, Gary Barlow, Paul McCartney, Melanie C, Jimmy Page, Boy George, Noel Gallagher and Kate Bush, calling on the PM to update UK law to “put the value of music back where it belongs – in the hands of music makers.”

This renewed call comes on the back of a report last week by The World Intellectual Property Organisation (WIPO)which said this is a “systemic problem [that] cries out for a systemic solution” and concluded that streaming should start to pay more like radio: “The more global revenues surge, the harder it is for performers to understand why the imbalance is fair—because it is not…streaming remuneration likely should be considered for a communication to the public right.”

More and more people are streaming music – heightened by the pandemic – but, as the artists point out, “the law has not kept up with the pace of technological change and, as a result, performers and songwriters do not enjoy the same protections as they do in radio,” with most featured artists receiving tiny fractions of a US cent per stream” and session musicians receiving nothing at all.

The letter suggests that “only two words need to change in the 1988 Copyright, Designs and Patents Act…so that today’s performers receive a share of revenues, just like they enjoy in radio” – a change which “won’t cost the taxpayer a penny but will put more money in the pockets of UK taxpayers and raise revenues for public services like the NHS” and which will contribute to the “levelling-up agenda as we kickstart the post-Covid economic recovery.”

The 234 signatories do not want streaming to be recognised as radio. Instead, they want streaming to share some of radio’s remuneration model so that they are paid more fairly. Legislation, despite recognising that streaming is replacing sales, is yet to recognise that the technology is on its way to replacing radio too.

The letter is backed by the Musicians’ Union, the Ivors Academy and the Music Producer’s Guild collectively representing tens of thousands of UK performers, composers and songwriters and producers, brought together in partnership with the #BrokenRecord campaign led by artist and songwriter, Tom Gray.

The Commons DCMS Committee has been examining this issue with its Economics of music streaming inquiry, expected to report by the end of this month, but it is understood that this issue falls between the remits of both the DCMS and BEIS departments, which is why the artists have chosen to address it to the Prime Minister.

The letter also recommends “an immediate government referral to the Competition and Markets Authority” because of “evidence of multinational corporations wielding extraordinary power” over the marketplace and the creation of an industry regulator.

They write that these changes “will make the UK the best place in the world to be a musician or a songwriter, allow recording studios and the UK session scene to thrive once again, strengthen our world leading cultural sector, allow the market for recorded music to flourish for listeners and creators, and unearth a new generation of talent.”

Tom Gray, Founder of the #BrokenRecord Campaign, said:

“It is amazing and timely that the World Intellectual Property Organisation, who create the global treaties that underpin UK law, are now reporting that we are right. This is the moment for the UK to lead the way. British music makers are suffering needlessly. There is an extraordinary amount of money in music streaming. It is a success story for a few foreign multinationals, but rarely for the British citizens who make the music”

“This letter is fundamentally about preserving a professional class of music-maker into the future. Most musicians don’t expect to be rich and famous or even be particularly comfortable, they just want to earn a crust.”

Horace Trubridge, General Secretary of the Musicians’ Union, said:

“I’m delighted to see so many artists, performers and songwriters backing our call. Streaming is replacing radio so musicians should get the same protection when their work is played on streaming platforms as they get when it’s played on radio.

“As the whole world has moved online during the pandemic, musicians who write, record and perform for a living have been let down by a law that simply hasn’t kept up with the pace of technological change. Listeners would be horrified to learn how little artists and musicians earn from streaming when they pay their subscriptions.

“By tightening up the law so that streaming pays more like radio, we will put streaming income back where it belongs – in the hands of artists. It’s their music so the income generated from it should go into their hands.”

Graham Davies, Chief Executive of the Ivors Academy, said:

“Paying music creators properly, which is what so many incredible artists have spoken up to ask for on behalf of present and future musicians and songwriters, will drive the streaming industry and sustain the UK creative economy. Music should and could be a major national asset, but its potential value is currently stripped by overseas interests.

We need to keep the value of British music in our nation by supporting, nurturing and investing in our creators, whilst ensuring the handful of foreign multinational corporations which dominate the music industry and have little interest in preserving British cultural heritage, contribute more value back into the UK. These easy steps will achieve exactly that.”

Crispin Hunt, Chair of the Ivors Academy, said:

“Major Music labels delude themselves that they are the sole providers of the music economy. They are not; the musicians, producers and composers who signed this letter are the true providers of the music economy; without them, no employment in music could exist.

“Britains Music Creators should be the primary beneficiaries of the value their creativity drives. The record companies are now glorified marketing firms, without manufacturing and distribution costs. Their extraordinary profits ought to be shared more equitably with creators. In streaming the song is king, yet songwriters are streaming’s serfs.

“British Music Creators want nothing more than a reasonable partnership with the companies that market and distribute our work. But a reasonable partnership should be based on shared rewards and responsibilities, not unilateral takings.

“With this letter, Britain’s greatest Music Creators say Music must reform, Government can and should help us fix it.”

At its meeting on the 21st of April 2021, the Nordic Musicians Union, NMU, discussed the issue of copyright buyouts.

Technological development has been rapid in connection with digitalisation and globalization. This has challenged existing remuneration models that have been developed over a long period of time. This includes legislation, agreements, and collective management organisations. This rapid development has affected the income of performers in a very negative way.

We note that the compensation levels generated via digital uses are unreasonably low. Therefore, the NMU, at both national and international levels, have introduced the need for stricter legislation regarding the balance of power in negotiations. This includes mandatory rules that ensure a reasonable remuneration for digital uses. The European Commission has acknowledged this need in the 2019 Copyright Directive by introducing provisions on appropriate and proportionate remuneration to authors and performers and further provisions to improve the bargaining position of performers. The Directive shall be implemented no later than 7 June 7, 2021.

The NMU recognise that business models are emerging that work around the legislation by maximizing the use of musicians’ and artists’ performances whilst ignoring long-standing practices and established copyright systems. Instead, they pay one-time compensation, undermine the moral rights, and might even demand that musicians and artists leave their own collection management organisations.

NMU’s view is that musicians should be paid fairly and correctly, both for their labour and for their copyright based on the actual exploitation over time. The moral rights must be fully respected and the choice to be a member of one’s own collective management organisation must be defended.

Performing artists receive far too little of the value that music generates when it is used. During the Corona pandemic, it has become all too clear that musicians need the backing and support of legislators as well as the audience and the music industry.

The NMU strongly opposes wholesale of rights for any possible use, known or yet to be discovered, against a one-off payment. Complete buyouts are not the future business model for performers!

[A bit of context: With all the riches being made from streaming, session musicians and vocalists make zero. And don’t forget that music made Daniel Ek a billionaire.]

Broken Record Campaign

Ivors Academy

Musicians Union

April 20, 2021

The Rt Hon Boris Johnson MP Prime Minister 10 Downing Street W1A 2AA

Dear Prime Minister,

We write to you on behalf of today’s generation of artists, musicians and songwriters here in the UK.

For too long, streaming platforms, record labels and other internet giants have exploited performers and creators without rewarding them fairly. We must put the value of music back where it belongs – in the hands of music makers.

Streaming is quickly replacing radio as our main means of music communication. However, the law has not kept up with the pace of technological change and, as a result, performers and songwriters do not enjoy the same protections as they do in radio.

Today’s musicians receive very little income from their performances – most featured artists receive tiny fractions of a US cent per stream and session musicians receive nothing at all.

To remedy this, only two words need to change in the 1988 Copyright, Designs and Patents Act. This will modernise the law so that today’s performers receive a share of revenues, just like they enjoy in radio. It won’t cost the taxpayer a penny but will put more money in the pockets of UK taxpayers and raise revenues for public services like the NHS.

There is evidence of multinational corporations wielding extraordinary power and songwriters struggling as a result. An immediate government referral to the Competition and Markets Authority is the first step to address this. Songwriters earn 50% of radio revenues, but only 15% in streaming. We believe that in a truly free market the song will achieve greater value.

Ultimately though, we need a regulator to ensure the lawful and fair treatment of music makers. The UK has a proud history of protecting its producers, entrepreneurs and inventors. We believe British creators deserve the same protections as other industries whose work is devalued when exploited as a loss-leader.

By addressing these problems, we will make the UK the best place in the world to be a musician or a songwriter, allow recording studios and the UK session scene to thrive once again, strengthen our world leading cultural sector, allow the market for recorded music to flourish for listeners and creators, and unearth a new generation of talent.

We urge you to take these forward and ensure the music industry is part of your levelling-up agenda as we kickstart the post-Covid economic recovery.

Ever heard the expression, “you’re making my argument?”

You may have seen the book reviews of “Spotify Untold” (or in Swedish “Spotify Inifrån”). The book is currently only available in Swedish and has not been released in the US, but in a new marketing twist the authors are on a book tour in the US promoting their book in Swedish to an English language audience. Must be nice.

The writers not only seemed to have missed the streaming gentrification part, which is of great consequence to artists, songwriters, and especially MP/TV composers–but those groups are pretty clearly not the authors’ audience. They are also peddling a ghoulish yarn about Steve Jobs that gives far more insight into Daniel Ek’s midnight of the soul than anything else. A simple fact check should have made one inquire further in my view.

If their interview with Variety is any indicator, the story line of “Spotify Untold” revolves around (1) music is a commodity (with no discussion of Spotify’s role in the commoditization of what is now openly called “streaming friendly music” not unlike “radio friendly” music–both equally loathed by artists whose name does not begin with “Justin”; and (2) Daniel Ek is a heroic genius (despite the resemblance to Damian in his teen pictures they are also handing out–he thankfully shaves his head).

But most importantly (3) Ek was pursued by Steve Jobs, the evil giant whose company he just happens to have filed a competition complaint against who was aided by the equally evil Sony and Universal as they were all in on it to keep our hero from entering the fabled land of Wall Street. Yes, a yarn straight out of Norse mythology as retold by Freud; perhaps a little too much so.

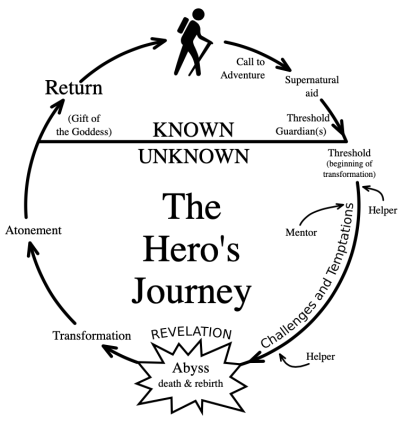

But the book may also be a corporatized version of Joseph Campbell’s hero’s journey from The Hero With A Thousand Faces aka Star Wars). You can plug Daniel Ek into the hero’s role pretty easily:

Barely a page into the book “Spotify Untold,” Swedish authors Jonas Leijonhufvud…and Sven Carlsson paint an odd scene. The year is 2010 and Spotify co-founder and CEO Daniel Ek [the hero] is facing a succession of obstacles [the Threshold Guardians] gaining entry into the U.S. market [the region of supernatural wonder] — or, more specifically, infiltrating the tightly-networked and often nepotistic to a fault music industry. [Unwelcoming of the stranger from Asgard, so unlike Silicon Valley.] As stress sets in [Challenges and Temptations], Ek becomes convinced that Apple’s Steve Jobs is calling his phone just to breathe deeply on the other end of the line, he purportedly confesses to a colleague[a Helper].

There’s a saying, “don’t speak ill of the dead.” That’s probably a bit superstitious for the authors, but is good advice. It’s unbecoming and Spotify should denounce it, although it’s highly unlikely that they will given their fatal attraction to PR disasters.

There’s also a saying, “don’t mock the afflicted,” so before you laugh hysterically at the story, realize that Steve Jobs caring enough about Daniel Ek to do such a thing (which assumes Steve knew Daniel Ek existed) was something that was very important to Daniel Ek. Or in a word–is Daniel Ek more Loki than Thor?

What is really objectively and factually odd about the authors’ 2010 Steve Jobs story about heavy breathing phone calls is that Steve got a liver transplant in 2009 and was very, very sick throughout 2010–the year they say these calls occurred.

Steve left Apple for good in August 2011 and passed in October 2011. It is implausible to me that he was even paying attention to Daniel Ek in 2010, assuming that Steve even knew or cared who Daniel Ek was. Aside from the fact that at that time Spotify was small potatoes, Steve had many more important things on his mind like staying alive. Plus, in my experience if Steve was going to leave you a testy voicemail or phone call, you knew exactly who it was. Exactly.

I for one think that the entire anecdote simply does not scan and is unsubstantiated by the authors’ own admission. Bizarre. Freudian. Not to mention a crass and thoughtless smear against a man who really did change the world. Who can’t defend himself because he is dead.

Variety reports that the authors were not able to confirm this rather insulting and perverse allegation. But don’t let that stop anyone from publishing gossip.

What Variety does report is this statement from the authors:

To us, Ek’s claim is as a reflection of how paranoid and anxious he must have felt in 2010, when Spotify was being denied access to the U.S. market, in large part due to pressure from Apple. The major record companies seem to have been quite loyal to the iTunes Music Store, and to Jobs personally….Because Spotify was hindered by Steve Jobs [it’s called competition], it forced the company to sweeten its deals with the record companies [also called competition]….Spotify is challenging Apple on a legal level right now.We address Spotify’s constant struggle with Apple in our book. If Ek were to talk about such sensitive topics in book form, [Spotify would] do it in their own way with full control.

The first thing I thought of when reading the story of “Spotify Untold” was that very competition claim that Spotify is pursuing in Europe right now. That claim appears to have been scripted–Spotify pursued it with the Obama competition authorities a few years ago. And then of course there was the New York and Connecticut state competition claim that curiously came out the same time as Apple Music launched in the US, apparently manipulated by Spotify’s very own Clintonista lobbying operative who was a political ally of Eric Schneiderman the former (ahem) New York Attorney General. (Spotify tried to drag Universal into that one, too–so this is a movie script that Spotify pulls down every so often for a polish and sometimes changes the supporting characters.)

While the authors claim that they spoke to many Spotify executives but not Ek, the book still has curious timing–as does the authors’ disclaimer that the book is not connected to Spotify directly, the plausible deniability that is the hallmark of black bag operations.

And if you believe as I do that Daniel Ek actually hates the major labels (read the Spotify DPO filing and you’ll get the idea), it’s only natural that he would try to twist Sony and Universal into the story. He just didn’t know that his major label negotiation experience was garden variety stuff and not unusual in any way. They didn’t get stock in iTunes so they damn well would in everything that came after iTunes. Daniel Ek was not singled out–rather, he opted in.

I would be very curious to know why the authors of “Spotify Inifrån” came away from their research thinking that the major labels were “quite loyal” to iTunes and to Steve Jobs. While that may have been true of certain executives, the reason that the labels required licensees to sell in Windows Media DRM (i.e., the format nobody wanted) was because they wanted to encourage competition with iTunes.

The labels eventually ended that failed policy after Steve called them out and suggested that they drop the DRM part (about which I strongly agreed in one of the first posts on MusicTechPolicy in 2006). Even after the labels dropped that failed idea, record companies large and small did not want a single digital retailer dominating the online market. So the idea that they colluded with Steve Jobs and Apple to make life difficult for a poor little hacker boy from Sweden is so inconsistent with reality to be laughable.

In fact, one could argue that were it not for Steve asking for more competition with iTunes Music Store (and in fairness, sell more iPods and later iPhones), there may never have been a Spotify at all. What that does not include is the accelerating failing belief in one of Spotify’s major selling point–the free service converts users from piracy to a paid service. That didn’t happen at anything like the rates that Spotify sold, nobody believes it anymore and it was unbelievable in the first place. But exactly what you’d expect a hacker to say.

And here’s some other research that got left out: Spotify’s psychographic data profiling is largely based on the work of Dr. Michael Kosinski, whose work also inspired the techniques of Cambridge Analytica and the Internet Research Agency. See Kosinski et al, The Song Is You: Preferences for Musical Attribute Dimensions Reflect Personality (2016). More on this influence another time.

So why would these authors be slinging this unlikely brew? It’s possible that the book is an answer to “Spotify Teardown,” funded by a grant and published (in English) earlier in 2019 with a much less mythological and much more recognizable approach to a Spotify reality according to an NPR review:

[“Spotify Teardown”] argues that Spotify isn’t a media company per se – and…asserts that it’s structurally much closer to a Facebook or Google, particularly in its digital business model. Indeed, Spotify was never really so much a music company as an Internet brand. “Spotify’s business model never benefited all musicians in the same manner but rather appeared — and still appears — highly skewed toward major stars and record labels, establishing a winner-takes-all market familiar from the traditional media industries.”

You won’t find that in a corporate bio. That sounds like the streaming gentrification reality and definitely wasn’t written by anyone named Justin. So while I don’t know what motivated the “Spotify Inifrån” authors, I do think that there’s a definite whiff of Astroturf in a book that tells a story that fits almost perfectly with the hero’s journey that Spotify would like to be telling competition authorities. I think the authors are aware of this, hence their disclaimers.

And I’m still waiting for the last leg of Daniel Ek’s hero’s arc, the transformation and atonement. Which is the part that makes the hero a hero. As the authors tell us, “[Spotify] would probably rather tell their story themselves than have us do it for them, but I think they understand our role as journalists.”

I just bet they do.

But look–credit where credit’s due. Ek used the music to make himself rich and he changed the economics of the music industry to keep making himself even richer. He gets million dollar performance bonuses when he doesn’t meet his performance targets. There are a growing number of niche and cultural artists who hate him. He’s also changed the way that fans interact with music online through the use of personality traits and data profiling instead of genre or artist based selection. And he invented “streaming friendly music” to the great joy of elevator operators everywhere.

For all his idiosyncrasies, Steve is largely revered and recognized as someone who really did change the world. Or as Daniel Ek tweeted when Jobs passed in 2011–after supposedly being harassed by Steve:

“Thank you Steve. You were a true inspiration in so many parts of my life, both personal and professional. My hat off to our time’s Da Vinci.”

Exactly. That Danny is a complex little man.

Remember those Mac/PC ads? You could just as easily run the same ad campaign for Spotify/Apple Music with only a few tweaks. And when it comes to marketing, what should be keeping Ek up at night is not devising sick stories he can tell about Steve Jobs but rather very justified fear of what will happen when Apple turns its marketing team loose on Spotify. He ain’t seen nothing yet.

If you think this is paranoid, watch this video from the distinguished journalist Sharyl Attkisson. Let’s just say I don’t put anything past these guys.

We’ve been hearing an alarming narrative that “record labels are making more money than ever from streaming, but they’re just not paying musicians”. To be clear, we certainly have our issues with major labels, however we also need facts and to be truthful.

The truth is, that a decade after losing half of it’s revenues due to piracy as reported by CNN (click here), record labels are now only getting back up to half of what the peak business was in 1999. Half of where we were in 1999, twenty years later. Let that sink in. As unpopular as he was twenty years ago, Lars Ulrich was right.

Twenty years later, and we’re still only half of where we were in 1999.

There are only three numbers that matter when looking at the record industry post-piracy and here they are:

1999 : $14.6b = $22.01 in 2018 Dollars 2009 : $6.3b = $7.37 in 2018 Dollars 2018 : $9.8b = $9.8b in 2018 Dollars

This is clearly illustrated in the chart below provided by the RIAA, the trade group responsible for tracking these figures. At their lowest point in 2014, revenues from record sales were less than one third of their peak.

What this chart also shows is a decade long loss of $10b or more annually, which is over $100b in lost revenues to labels and artists. That’s $100b in lost revenues to labels and artists in just the past decade.

If we track total lost revenue to labels and artists since the launch of Napster in 1999 it totals just under $200 Billion Dollars in the USA alone.

The fundamental problem remains the same. There’s a hole in our bucket and all that revenue falling out though the bottom leads more or less to advertising funded piracy and YouTube. Many have suggested that YouTube is effectively the largest ad supported piracy platform. As we reported earlier this year in our updated Streaming Price Bible, the YouTube Value Gap is very, very real.

In future posts we’ll offer solutions and suggestions that should be under consideration at every major label. Not the least of which is transitioning subscription streaming models to incorporate a per stream transactional baseline, or a minimum wholesale price per stream.

In streaming, consumption does not grow revenues. More consumption and more streams do not generate more money. Revenue can only be generated by charging more for subscriptions, generating more advertising revenue (ad supported only, obviously) and expanding into more markets (gaining new subscribers). But eventually, everything flattens.

So the biggest question remains. What happens to overall revenues as streaming matures and cannibalizes the remaining revenue sources into purely niche markets. Digital Downloads will account for less than 10% of recorded music revenues by the end of the year, if not already. The CD market continues drop, and vinyl also declined slightly from 2017 (4.4%) to 2018 (4.3%).

Will streaming compensate for the lost revenues in other formats and continue to grow revenues towards a true recovery? It’s possible, but there will have to be some changes to address the economics presented to consumers despite what Goldman Sachs says. For the year of 2018 the industry reported $9.8b in revenues. To make that $37.2b by 2030 the industry needs to add nearly $3b a year for the next 10 years!

We don’t know what else they’ve got in that crystal ball that can predict revenues over a decade into the future but even by their bullish estimate of $37.2b in 2030, that is only $28b in 2019 dollars. Right now we’re still about $20b short.

You must be logged in to post a comment.