Several of our posts on streaming pay rates aggregated into one single source. Enjoy…

[UN to Airlift Calculators, Behavioral Economics Textbooks to Digital Music Industry]

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

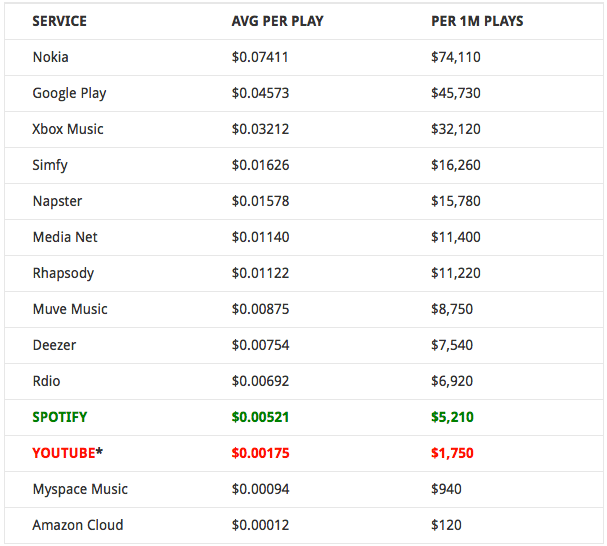

If the services at the top of the list like Nokia, Google Play and Xbox Music can pay more per play, why can’t the services at the bottom of the list like Spotify and YouTube?

We’ll give you a hint, the less streams/plays there are the more each play pays. The more plays there are the less each stream/play pays. Tell us again about how these services will scale. Looking at this data it seems pretty clear that the larger the service get’s, the less artists are paid per stream.

So do you think streaming royalty rates are really going to increase as these services “scale”? No, we didn’t either.

We’ve been waiting for someone to send us this kind of data. This info was provided anonymously by an indie label (we were provided screenshots but anonymized this info to a spreadsheet). Through the cooperative and collaborative efforts of artists such as Zoe Keating and The Cynical Musician we hope to build more data sets for musicians to compare real world numbers.

In our on going quest for openness and transparency on what artists are actually getting paid we’d love to hear from our readers if their numbers and experience are consistent with these numbers below. At the very least, these numbers should be the starting point of larger conversations for artists to share their information with each other.

Remember, no music = no business.

For whatever reason there appear to be a lot of unmonetized views in the aggregate. So let’s just focus on the plays earning 100% of the revenue pool in the blue set. These are videos where the uploader retains 100% of the rights in the video including the music, the publishing and the video content itself.

For whatever reason there appear to be a lot of unmonetized views in the aggregate. So let’s just focus on the plays earning 100% of the revenue pool in the blue set. These are videos where the uploader retains 100% of the rights in the video including the music, the publishing and the video content itself.

| Plays | Earnings | Per Play |

| 2,023,295 | $3,611.84 | $0.00179 |

| 1,140,384 | $2,155.69 | $0.00189 |

| 415,341 | $624.54 | $0.00150 |

| 240,499 | $371.47 | $0.00154 |

| 221,078 | $313.47 | $0.00142 |

| TOTALS | TOTALS | AVERAGE |

| 4,040,597 | $7,077.01 | $0.00175 |

So it appears that YouTube is currently paying $1,750 per million plays gross.

We understand that people reading this may report other numbers, and that’s the point. There is no openness or transparency from either Spotify or YouTube on what type of revenue artists can expect to earn and under what specific conditions. So until these services provide openness and transparency to musicians and creators, “sharing” this type of data is going to be the best we’re going to be able to do as East Bay Ray comments in his interview with NPR.

As we’re now in a world where you need you need a million of anything to be meaningful here’s a benchmark of where YouTube ranks against Spotify.

| Service | Plays | Per Play | Total | Notes |

| Spotify To Performers/Master Rights | 1,000,000 | 0.00521 | $5,210.00 | Gross Payable to Master Rights Holder Only |

| Spotify To Songwrtiers / Publishers | This revenue is for the same 1m Plays Above | 0.000521 | $521.00 | Gross Payable to Songwriter/s & Publisher/s (estimated) |

| YouTube Artist Channel | 1,000,000 | 0.00175 | $1,750.00 | Gross Payable for All Rights Video, Master & Publishing |

| YouTube CMS (Adiam / AdRev) ** | 1,000,000 | 0.00032 | $321.00 | Gross Payable to Master Rights Holder Only |

The bottom line here is if we want to see what advertising supported free streaming looks like at scale it’s YouTube. And if these are the numbers artists can hope to earn with a baseline in the millions of plays it speaks volumes to the unsustainability of these models for individual creators and musicians.

Meet the New Boss: YouTube’s Monopoly on Video | MTP

It’s also important to remember that the pie only grows with increased revenue which can only come from advertising revenue (free tier) and subscription fees (paid tier). But once the revenue pool has been set, monthly, than all of the streams are divided by that revenue pool for that month – so the more streams there are, the less each stream is worth.

All adrev, streaming and subscription services work on the same basic models as YouTube (adrev) and Spotify (adrev & subs). If these services are growing plays but not revenue, each play is worth less because the services are paying out a fixed percentage of revenue every month divided by the number of total plays. Adding more subscribers, also adds more plays which means that there is less paid per play as the service scales in size.

This is why building to scale, on the backs of musicians who support these services, is a stab in the back to those very same artists. The service retains it’s margin, while the artists margin is reduced.

[** these numbers from a data set of revenue collected on over 8 million streams via CMS for an artist/master rights holder]

Here’s what 1 million streams looks like from different revenue perspectives on the two largest and mainstream streaming services.

| Service | Units | Per Unit | Total | Notes |

| Spotify | 1,000,000 | $0.00521 | $5,210.00 | Gross Payable to Master Rights Holder Only |

| Spotify | same million units as above | $0.00052 | $521.00 | Gross Payable to Songwriter/s & Publisher/s (est) |

| YouTube | 1,000,000 | $0.00175 | $1,750.00 | Gross Payable for All Rights Video, Master & Publishing |

| YouTube CMS Master Recording (Audiam / AdRev) | 1,000,000 | $0.00032 | $321.00 | Gross Payable to Master Rights Holder Only |

| STREAMING TOTALS | 3,000,000 | $7,802.00 | TOTAL REVENUE EARNED FOR 3 MILLION PLAYS ON SPOTIFY AND YOUTUBE | |

| Itunes Album Downloads | 1,125 | $7.00000 | $7,875.00 | Gross payable including Publishing |

Here are some compelling stats on the break down of what percentage of videos on YouTube actually achieve breaking the 1 million play threshold, only 0.33%

CHART OF THE DAY: Half Of YouTube Videos Get Fewer Than 500 Views | Business Insider

Some 53% of YouTube’s videos have fewer than 500 views, says TubeMogul. About 30% have less than 100 views. Meanwhile, just 0.33% have more than 1 million views.

That’s not a huge surprise. But it highlights some of the struggles Google could have selling ads around all those unpopular videos, despite the money it has to spend to store them.

An artist needs to generate THREE MILLION PLAYS on the two largest and most popular streaming platforms to equal just 1,125 album downloads from Itunes. This is an important metric to put in context. In 2013 only 4.8% of new album releases sold 2,000 units or more. So if only 4.8% of artists can sell 2,000 units or more, how many artists can realistically generate over four million streams from the same album of material?

in 2013 there were 66,565 new releases, only 3,237 sold more than 2,000 units = 4.8% of new releases sold over 2,000 units

in 2013 there were 915,482 total releases in print, only 14,856 sold more than 2,000 units = 1.6% of ALL RELEASES in print sold more than 2,000 units.

This is even more important when you start to consider that many artists feel that growing a fan base of just 10,000 fans is enough to sustain a professional career. Note we said solo artists because these economics probably need to be multiplied by each band member added for the revenue distribution to remain sustainable. So a band of four people probably need a sales base of 40,000 fans to sustain a professional career for each member of the band.

Each 10,000 albums sold on iTunes (or 100,000 song downloads) generates $70,000 in revenue for the solo artist or band. To achieve the same revenue per 10,000 fans in streams, the band has to generate 30 million streaming plays (as detailed above) if they are distributing their music across the most common streaming services including Spotify and YouTube.

In 2013 the top 1% of new releases (which happen to be those 620 titles selling 20k units or more) totaled over 77% of the new release market share leaving the remaining 99% of new releases to divide up the remaining 23% of sales.

This appears to confirm our suspicion that the internet has not created a new middle class of empowered, independent and DIY artists but sadly has sentenced them to be hobbyists and non-professionals.

Meanwhile the major artists with substantial label backing dominate greater market share as they are the few who can sustain the attrition of a marketplace where illegally free and consequence free access to music remains the primary source of consumption.

What’s worse is that it is Silicon Valley corporate interests and Fortune 500 companies that are exploiting artists and musicians worse than labels ever did. New boss, worse than the old boss, indeed.

So whose feeling empowered?

RELATED:

UN to Airlift Calculators, Behavioral Economics Textbooks to Digital Music Industry

Streaming Is the Future, Spotify Is Not. Let’s talk Solutions.

Who will be the First Fired Label Execs over Spotify Fiasco & Cannibalization?

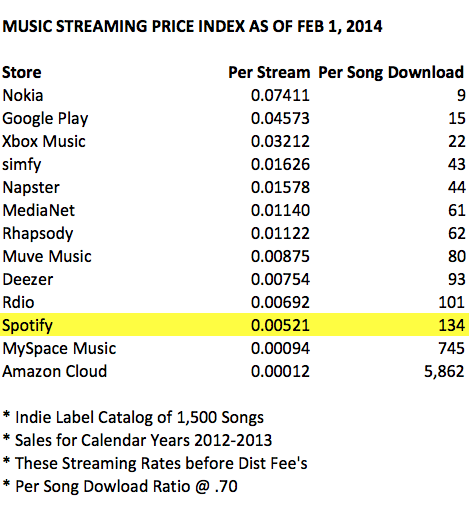

The first graphic – in US $? cents? airplanes? eggs?

Put a $ in front of the number, $0.07411 or, about Seven Cents for Nokia and $0.00521 or about half a cent for Spotify.

Hi, and thank you for this enlightening editorial.

I’ve a question regarding the numbers of new releases and releases in print you mention in your post: “In 2013 there were 66,565 new releases, only 3,237 sold more than 2,000 units”, and again “in 2013 there were 915,482 total releases in print, only 14,856 sold more than 2,000 units”.

Is this data for the US or the World? And can you be so kind to point me to your source?

Thanks again!

Johann

USA only, the source is Soundscan.

The average indie artist sells less than 1000 units so showing nice figures of 70,000 sales is nonsensical. Also in this day and age no one forces you to put your music on Youtube or Spotify for that matter and as Taylor Swift has shown, if you and your label decide to boycott these services, the sky will not fall. Why artists and labels don’t have their own streaming sites with either the subscription or ad funded model beggars belief.

We would agree with you if this were true. And, although that may be true for Spotify, ask any artists if they have been able to actually remove their work from YouTube with any effectiveness. They will say no.

https://thetrichordist.com/2013/01/24/two-simple-facts-about-technology-and-piracy-itunes-vs-youtube/

Here’s the thing people and celebs don’t get about SPOTIFY. You may not get alot of $$$ up front, but you will get MORE $$ in the long term. Consider me 1 user, and buying 1 album for $20. The label gets that $20 and that’s it. I can listen to that album for 30 years and play the songs a million times, but they only got $20.

Now with SPOTIFY however, you get paid, everytime I play the song. So yes, you may only get a part of a penny for this play of the 1 song. But at the end of the week, you may have gotten a couple dollars. By the end of tte year you may have over 50 dollars. by the end of the decade you may have over $1,000 .. just from one user. You see with spotify, you get money everytime it’s played. So all celebs and muscians should LOVE this model.

And it’s a win win. Consumers should love the Paid subsription to spotify as well! You pay a low monthly fee, and you can listen to unlimited music. (like netflix, but for music. Who buys dvd’s anymore??) And each song you listen to, the $$ go to that artist or label, etc. Embrace Spotify, it will work, but you have to think MACRO scale and think of the future.

If an artist has a really good hit. A person may want to listen to that song on repeat over and over. And just think, that artist is getting paid everytime. So yes, up front you don’t get the $20. But over the course of my life, you will have earned well over that amount (Double / triple/ hundred fold) from the amount that i listen. 🙂

George – unfortunately, that’s just not true. If it was this conversation would not be happening. The simple fact is that math does not work, and the revenue is determined by 1) the number of PAID subscribers, and 2) the amount of advertising revenue that can be sold (this is explained in th post above, you may need to re-read it). Neither of those revenue streams have anything to do with the number of times a song is played. It is mathematically impossible for Spotify to scale and pay fair revenues to artists… please see the links below.

https://thetrichordist.com/2014/11/07/but-spotify-is-paying-70-of-gross-to-artists-isnt-that-fair-no-and-heres-why/

https://thetrichordist.com/2013/02/08/music-streaming-math-will-it-all-add-up/

Once you understand this, you understand this, you will understand the larger problem and no amount of doublespeak will outrun the raw numbers. It’s just math.

Another way to dissect the ‘you get more over time’ argument is to look at how many plays you would need to ‘break even’ compared to a sale, which is currently about 134 plays on Spotify, according to the data here. How often does any individual listen to a song over 100 times? In 20 years of listening to music I doubt I’ve heard even my favourite songs much more than 50 times, with the average play rate for songs I like being somewhere between 10 and 20 times. So there’s no way I could contribute as much via streaming as I have via purchasing.

I truly enjoy reading your articles–lots of information here that is otherwise hidden from view. I used to be all about “rah-rah-free-music! No Copyright!” as a musician and listener. You have definitely opened my eyes to a tragic reality–we cut out the old bosses, and the new bosses are way, way worse (while pretending to be very different).

However, I do have to tell you: please get someone to help you proofread your work (I may be able to volunteer a few hours a week). I sometimes have to re-read a sentence several times to understand what you are writing. The constant confusion between “it’s” (it is) and its (belongs to it) leads to a bunch of double-takes, and slows me down reading. If your articles were written a bit better, they may get more distribution (it’s not everything–just like with music, there are some albums you will listen to anyway, even on a banged-up cassette), and would definitely encourage me to read your work more often.

Regardless, keep up the good work and keep fighting the good fight!

ha! this is what happens when musicians try to run a blog…

Ha ha! Love that reply…

Either force this kind of services to be pay to play for everyone or have ISP’s collect royalty money for every song you stream on your monthly bill. Or keep consuming the crappy music they are feeding you, because he who has the most money, gets heard the most anyway. The illusion of choice.

Compared to MY BMI statements, these rates here are actually HIGHER. I’ve calculated Pandora payouts at $.000003 per play. That’s five zeros before we get a real number. Your numbers don’t have as many zeros after the decimals. Not questioning the accuracy, just saying I’ve made far less according to certain line items on my statements.

The ‘inaccuracy’ has been explained and no many variables in play but the general message is correct. I’m not even a musician and it angers me…

*no doubt

Thank you for being the ONLY site talking about song writers/artists getting ripped off. I can send you guys my statements and you will laugh at the fact I made $8 in Oct for over 100,000 plays. Insanity! Thank you guys for educating the public! Us song writers thank you!!! 🙂

As an extra point of anecdata, for my unsigned band (with theoretically nobody taking a cut without me knowing about it), the Spotify streams are slightly higher than the figure here (about $0.009 per track) but Google Play All Access is significantly lower by comparison ($0.012 per track).

Interesting information, which is rarely shared clearly, so thanks for that.

However to be fair it’d need to be ponderated based on market shares of all these services.

In other words what is the likeliness to do 1 million streams on, let’s say, xbox music, compared to Spotify or YouTube? (keeping in mind more than 50% of people regularly listen to music on YouTube as the primary source).

Per-unit stream or per-download rates do not matter that much really, whereas market share does, meaning volume of transactions, volume of users, number of subscribers of free / paid tiers, market penetration rate based on demographics…Etc.

At the moment, looking at our numbers, the ratio between Spotify and iTunes is 1:10.

Meaning for a given release, when an artist generates 1$ of revenue on Spotify, he/she also generates 10$ of revenue on iTunes. These are complementary incomes, rather than something to oppose.

Same goes for YouTube, as soon as you start monetizing your songs, and as long as your official videos or the ones from UGC (user generated content) make a decent number of views (at least 100,000) the money starts to flow in, not crazy amounts but still.

Complementary income as well.

Actually Itunes to Spotify is 134:1 on individual songs… it takes 134 streams on Spotify to equal 1 song download on Itunes. Since this post was published we’re hearing from a lot of people that their net aggregate play per stream is DROPPING well below what we’ve posted which also proves the point that you can not grow the pie with streams. In streaming the pie does not grow based on consumption – only advertising revenue or subscription fees, once those two sources of revenue are capped the pie can only be cut into smaller pieces no matter how many more streams are consumed. Very simply this means the effective per stream rates will continue to decrease as the size of the service grows larger (this is also explained in the post).

also see this:

http://thecynicalmusician.com/2014/11/new-money/

I was not referring to how many streams are required to equal a download.

If you forget about the per-unit values and look at the bigger picture, things are not as “bad” as presented here and on various other blogs.

Take a look at the latest studies from Midia for example, iTunes is still huge in value compared to any other music services.

Spotify is, like many others, a drop in the bucket but still generating heaten debates…

You might want to read this Midia Research as it confirms what we’ve been saying about the economics and sustainability of free streaming services:

http://www.midiaresearch.com/blog/view/unlocking-youtube-how-youtube-will-change-music-subscriptions.html

“If we discount both rates and apply them to the US and UK population, Music Key would contribute about $400 million dollars in revenue in one year but would be responsible for more than $2.6 billion in lost subscription revenue, meaning its net impact would be around -$2.3 billion.”

Yes… negative 2.3 billion…

“If the services at the top of the list like Nokia, Google Play and Xbox Music can pay more per play, why can’t the services at the bottom of the list like Spotify and YouTube?”

You focus on math and that’s fine. I won’t argue against it.

1. However, I’d just like to point out that that is just part of the question and you seemed to have overlooked a major question. The artist/label is paying for a service. That service is profoundly different in the case of Xbox Music, Google Play, Youtube or even Spotify.

Example: I have no clue how Spotify is operating in the US market, but they have been striking deals with mobile operators so that streaming does not count towards mobile data traffic. That’s a pretty substantial difference. It may be irrelevant if you have unlimited data in the US (no clue) but it certainly isn’t common in Europe and, I guess, in most of the world.

Point is: you have to carefully look at what the artists/labels are paying for in their deals with the various streaming services. I am not saying this justifies the price difference, but that it certainly justifies a price difference. I wouldn’t expect services to ever offer awfully similar prices on that reason alone: it’s a payment for a service by the artists/label.

2. One problem with your overall argument (or rather strategy), however, is that while you are crying unfair(!) and duly using math to demonstrate it, you do not seem to indicate what would be fair. Assessing fairness is not an entirely subjective endeavor and it can certainly be used to spot unfairness as well as to determine what’s fair. It would be a very interesting read.

If you – or Taylor Swift – actually strive for change, that’s the step to take. In truth, Taylor is (or would) have been in a much better position to do so individually and renegotiate her terms – and thus initiating positive action -, but she preferred to take a more general stance – by taking a highly buzzing but merely disruptive action.

There are arguments for either strategy, but I find that just by pointing out unfairness or stepping out you are leaving the remaining part of the task to others (which may be entirely imaginary beings at this point in time).

In sum: You should not leave the determination of what’s fair to others. You should actually build a fairness argument and not merely try to throughly point out the unfairness of the status quo.

There are a lot of ways to achieve fairness with different variables, windows, price tiers and value propositions. The problem is, Spotify is not open to any of them and YouTube does not allow you to opt out of their service (try the DMCA some time). So until there is fairness over choice and consent, as well as these services providing openess, transparency and audit rights, these issues are going to exist.

https://thetrichordist.com/2014/10/14/streaming-is-the-future-spotify-is-not-lets-talk-solutions/

https://thetrichordist.com/2014/11/11/how-to-fix-music-streaming-in-one-word-windows-two-more-pay-gates/

https://thetrichordist.com/2013/10/17/why-spotify-is-not-netflix-and-why-it-maybe-should-be/

https://thetrichordist.com/2013/02/08/music-streaming-math-will-it-all-add-up/

“Three weeks ago, I started running 5k every Wednesday. Every time I ran I got around 30 seconds quicker than the last time. Based off some projections on the back of a napkin, in about 6 months, i’ll be faster than the speed of light.” – this post.

Bottom line – if you want more money per play from me, i’ll either listen to your music less, or i’ll stop paying for it entirely. I don’t have infinite money. The industry as a whole has a value, and it’s entirely independent of the number of plays. I appreciate that you want more money. I appreciate you do not have a degree in economics or statistics. I appreciate you put a lot of work into getting these numbers, and you want something to show for that work. But i didn’t appreciate the post. If you want to show how Spotify is taking your money, analyse their end of year balance sheet, not their play list.

Or, you could pay 99 cents for a song on Itunes and listen to infinitely, which we’re totally OK with… The choice is not be between less or not at all, the choice is between fair and exploitation. It sounds like you prefer exploitation when you could simply just pay 99 cents and own the song forever, no longer tethered to Spotify or anyone else.

I am quite deeply educated in economics. The quantitative part especially. There is nothing wrong with Trichordist editor part. Your comment about balance sheet vs playlist is stunningly ignorant. Streaming is the future. It replaces ownership for most or at least many people. So each spin must make up some of the fixed costs of writing recording, producing and promoting the music. My preliminary UGA data shows that on average a purchased song is spun 7 times. A song that seems to be popular with the owner is spun between 25-20 times. In order to replace the cannibalized sale the song needs to be spun 134 times. Most of us would rather not take the low rate of pay offered by spotify. It’s criminal that we are forced into these deal by government mandates and record company back room deals.