Back in October of 2014 we asked the question “Who will be the First Fired Label Execs over Spotify Fiasco & Cannibalization?“. Now we know. In one week, two senior major label digital music execs have resigned. First Rob Wells on Monday, and on Friday David Ring followed.

We don’t know if these resignations are related to the realization that Spotify actually is cannibalizing transactional revenues, or that YouTube Music Key will do more and worse, but the timing is suspect given recent statements by label chief Lucian Grange.

“We want to accelerate paid subscriptions… Ad-funded on-demand is not going to sustain the entire ecosystem of the creators as well as the investors” – Lucian Grange

Spotify has been a disaster from bad artist relations to the catalyst for declining transactional revenues. We celebrate the move for more aggressive positioning to paid subscriptions, but even at current rates of $9.99 a month it’s hard to see subs gain the marketshare and revenue needed to compensate for the rapidly declining transactional revenues. In 2014 Itunes revenues dropped by double digits with Apple reporting a decrease of 13%-14% year to year. This following a decrease in overall digital revenues in 2013 (the first decrease ever in digital format sales since their inception).

So that’s two consecutive years of reduced revenue in what should be a growing market segment. So what went wrong? In a word, Spotify. Two more, YouTube.

In other words, Free Doesn’t Pay…

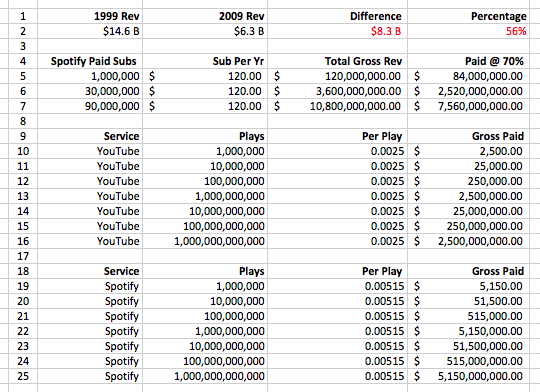

We’ve said it before and we’ll say it again, it’s just math. Below is a table we first published two years ago in February of 2013 when we asked the question, “Music Streaming Math, Can It All Add Up?”.

Although the aggressive move to paid subscriptions is a very positive one, we’re still concerned when looking at the numbers in the tables above when put in the context of the current state of the mature subscription based businesses (see below).

Netflix only has 36m subscribers in the US, no free tier, and massive limitations on available titles of both catalog and new releases. Sirius XM, 26.3m in the US as a non-interactive curated service installed in homes, cars and accessible online. Premium Cable has 56m subscribers in the US paying much more than $10 a month and also with many limitations. Spotify… 3m paid subscribers in the US after four years. Tell us again about this strategy of “waiting for scale.” Three Million Paid… Three…

* 3m Spotify Subs Screen Shot

* 26.3m Sirius XM Subs Screen Shot

* 36m Netflix Subs Screen Shot

* 56m Premium Cable Subs Screen Shot

* $7b Music Business Screen Shot

Of course none of this is to say that streaming can’t work. It can. It’s that Spotify (and YouTube) are just really bad music business models that have unsustainable economics and exploit artists because they are financial instruments and not a music companies.

Let’s be clear about this. We do believe that streaming is the future of music delivery and distribution, but thus far the transition has been horribly mismanaged. What is needed is clear leadership to define the models and value propositions that work for all stakeholders. We’ve made some suggestions in our common sense post “Streaming Is the Future, Spotify Is Not. Let’s talk Solutions.”

We’re open minded about new business models, but before people get ahead of themselves with wild claims about a $100 Billion Record Business based on magic unicorn math we need to get back to earth, and get out the calculators.

It’s just math.

As revenue spirals down from licensing deals, the major labels at some point may be looking at class action lawsuits from the artists they represent. Is there a conflict of interest when equity deals/signing bonuses are part of the negotiation process to determine streaming rates and those side deals are not shared with the artists?

Or made public.