Several of our posts on streaming pay rates aggregated into one single source. Enjoy…

[UN to Airlift Calculators, Behavioral Economics Textbooks to Digital Music Industry]

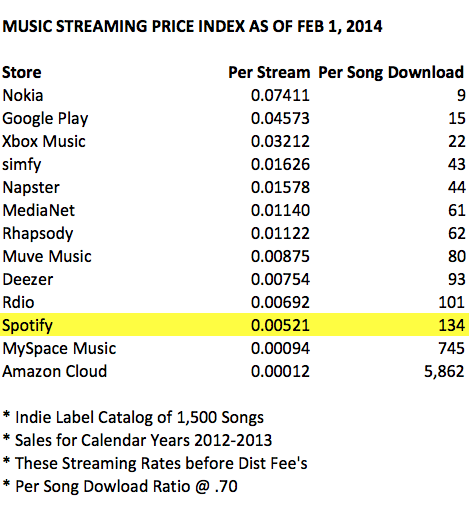

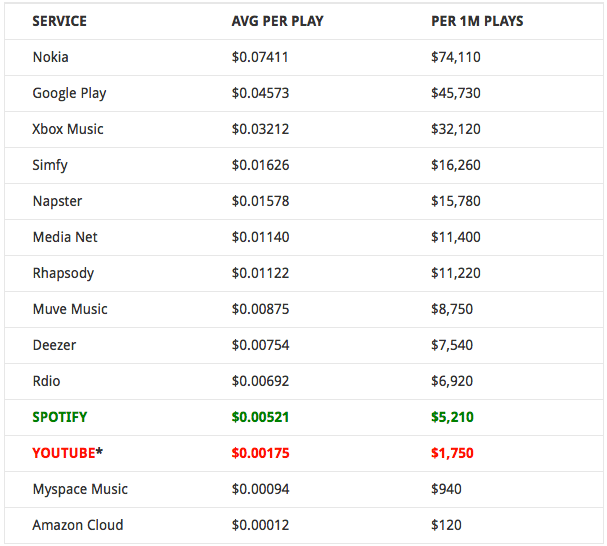

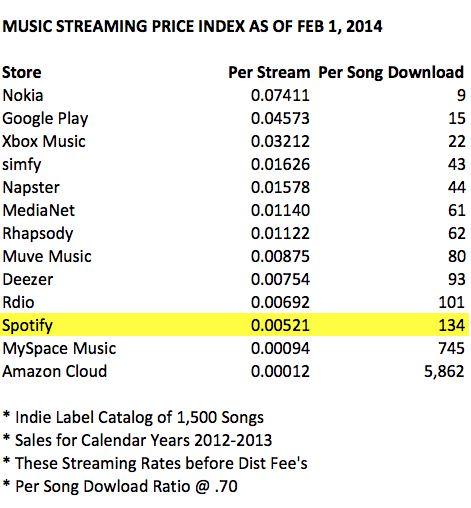

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

[EDITORS NOTE: All of the data above is aggregated. In all cases the total amount of revenue is divided by the total number of the streams per service (ex: $5,210 / 1,000,000 = .00521 per stream). In cases where there are multiple tiers and pricing structures (like Spotify), these are all summed together and divided to create an averaged, single rate per play.]

If the services at the top of the list like Nokia, Google Play and Xbox Music can pay more per play, why can’t the services at the bottom of the list like Spotify and YouTube?

We’ll give you a hint, the less streams/plays there are the more each play pays. The more plays there are the less each stream/play pays. Tell us again about how these services will scale. Looking at this data it seems pretty clear that the larger the service get’s, the less artists are paid per stream.

So do you think streaming royalty rates are really going to increase as these services “scale”? No, we didn’t either.

[ BREAKING! Apple Announces Itunes One Dollar Albums and Ten Cent Song Downloads In Time For The Holidays! | Sillycon Daily News ]

We’ve been waiting for someone to send us this kind of data. This info was provided anonymously by an indie label (we were provided screenshots but anonymized this info to a spreadsheet). Through the cooperative and collaborative efforts of artists such as Zoe Keating and The Cynical Musician we hope to build more data sets for musicians to compare real world numbers.

In our on going quest for openness and transparency on what artists are actually getting paid we’d love to hear from our readers if their numbers and experience are consistent with these numbers below. At the very least, these numbers should be the starting point of larger conversations for artists to share their information with each other.

Remember, no music = no business.

For whatever reason there appear to be a lot of unmonetized views in the aggregate. So let’s just focus on the plays earning 100% of the revenue pool in the blue set. These are videos where the uploader retains 100% of the rights in the video including the music, the publishing and the video content itself.

For whatever reason there appear to be a lot of unmonetized views in the aggregate. So let’s just focus on the plays earning 100% of the revenue pool in the blue set. These are videos where the uploader retains 100% of the rights in the video including the music, the publishing and the video content itself.

| Plays |

Earnings |

Per Play |

| 2,023,295 |

$3,611.84 |

$0.00179 |

| 1,140,384 |

$2,155.69 |

$0.00189 |

| 415,341 |

$624.54 |

$0.00150 |

| 240,499 |

$371.47 |

$0.00154 |

| 221,078 |

$313.47 |

$0.00142 |

| TOTALS |

TOTALS |

AVERAGE |

| 4,040,597 |

$7,077.01 |

$0.00175 |

So it appears that YouTube is currently paying $1,750 per million plays gross.

We understand that people reading this may report other numbers, and that’s the point. There is no openness or transparency from either Spotify or YouTube on what type of revenue artists can expect to earn and under what specific conditions. So until these services provide openness and transparency to musicians and creators, “sharing” this type of data is going to be the best we’re going to be able to do as East Bay Ray comments in his interview with NPR.

As we’re now in a world where you need you need a million of anything to be meaningful here’s a benchmark of where YouTube ranks against Spotify.

| Service |

Plays |

Per Play |

Total |

Notes |

| Spotify To Performers/Master Rights |

1,000,000 |

0.00521 |

$5,210.00 |

Gross Payable to Master Rights Holder Only |

| Spotify To Songwrtiers / Publishers |

This revenue is for the same 1m Plays Above |

0.000521 |

$521.00 |

Gross Payable to Songwriter/s & Publisher/s (estimated) |

| YouTube Artist Channel |

1,000,000 |

0.00175 |

$1,750.00 |

Gross Payable for All Rights Video, Master & Publishing |

| YouTube CMS (Adiam / AdRev) ** |

1,000,000 |

0.00032 |

$321.00 |

Gross Payable to Master Rights Holder Only |

The bottom line here is if we want to see what advertising supported free streaming looks like at scale it’s YouTube. And if these are the numbers artists can hope to earn with a baseline in the millions of plays it speaks volumes to the unsustainability of these models for individual creators and musicians.

Meet the New Boss: YouTube’s Monopoly on Video | MTP

It’s also important to remember that the pie only grows with increased revenue which can only come from advertising revenue (free tier) and subscription fees (paid tier). But once the revenue pool has been set, monthly, than all of the streams are divided by that revenue pool for that month – so the more streams there are, the less each stream is worth.

All adrev, streaming and subscription services work on the same basic models as YouTube (adrev) and Spotify (adrev & subs). If these services are growing plays but not revenue, each play is worth less because the services are paying out a fixed percentage of revenue every month divided by the number of total plays. Adding more subscribers, also adds more plays which means that there is less paid per play as the service scales in size.

This is why building to scale, on the backs of musicians who support these services, is a stab in the back to those very same artists. The service retains it’s margin, while the artists margin is reduced.

[** these numbers from a data set of revenue collected on over 8 million streams via CMS for an artist/master rights holder]

Here’s what 1 million streams looks like from different revenue perspectives on the two largest and mainstream streaming services.

| Service |

Units |

Per Unit |

Total |

Notes |

| Spotify |

1,000,000 |

$0.00521 |

$5,210.00 |

Gross Payable to Master Rights Holder Only |

| Spotify |

same million units as above |

$0.00052 |

$521.00 |

Gross Payable to Songwriter/s & Publisher/s (est) |

| YouTube |

1,000,000 |

$0.00175 |

$1,750.00 |

Gross Payable for All Rights Video, Master & Publishing |

| YouTube CMS Master Recording (Audiam / AdRev) |

1,000,000 |

$0.00032 |

$321.00 |

Gross Payable to Master Rights Holder Only |

| STREAMING TOTALS |

3,000,000 |

|

$7,802.00 |

TOTAL REVENUE EARNED FOR 3 MILLION PLAYS ON SPOTIFY AND YOUTUBE |

| Itunes Album Downloads |

1,125 |

$7.00000 |

$7,875.00 |

Gross payable including Publishing |

Here are some compelling stats on the break down of what percentage of videos on YouTube actually achieve breaking the 1 million play threshold, only 0.33%

CHART OF THE DAY: Half Of YouTube Videos Get Fewer Than 500 Views | Business Insider

Some 53% of YouTube’s videos have fewer than 500 views, says TubeMogul. About 30% have less than 100 views. Meanwhile, just 0.33% have more than 1 million views.

That’s not a huge surprise. But it highlights some of the struggles Google could have selling ads around all those unpopular videos, despite the money it has to spend to store them.

An artist needs to generate THREE MILLION PLAYS on the two largest and most popular streaming platforms to equal just 1,125 album downloads from Itunes. This is an important metric to put in context. In 2013 only 4.8% of new album releases sold 2,000 units or more. So if only 4.8% of artists can sell 2,000 units or more, how many artists can realistically generate over four million streams from the same album of material?

in 2013 there were 66,565 new releases, only 3,237 sold more than 2,000 units = 4.8% of new releases sold over 2,000 units

in 2013 there were 915,482 total releases in print, only 14,856 sold more than 2,000 units = 1.6% of ALL RELEASES in print sold more than 2,000 units.

This is even more important when you start to consider that many artists feel that growing a fan base of just 10,000 fans is enough to sustain a professional career. Note we said solo artists because these economics probably need to be multiplied by each band member added for the revenue distribution to remain sustainable. So a band of four people probably need a sales base of 40,000 fans to sustain a professional career for each member of the band.

Each 10,000 albums sold on iTunes (or 100,000 song downloads) generates $70,000 in revenue for the solo artist or band. To achieve the same revenue per 10,000 fans in streams, the band has to generate 30 million streaming plays (as detailed above) if they are distributing their music across the most common streaming services including Spotify and YouTube.

In 2013 the top 1% of new releases (which happen to be those 620 titles selling 20k units or more) totaled over 77% of the new release market share leaving the remaining 99% of new releases to divide up the remaining 23% of sales.

This appears to confirm our suspicion that the internet has not created a new middle class of empowered, independent and DIY artists but sadly has sentenced them to be hobbyists and non-professionals.

Meanwhile the major artists with substantial label backing dominate greater market share as they are the few who can sustain the attrition of a marketplace where illegally free and consequence free access to music remains the primary source of consumption.

What’s worse is that it is Silicon Valley corporate interests and Fortune 500 companies that are exploiting artists and musicians worse than labels ever did. New boss, worse than the old boss, indeed.

So whose feeling empowered?

RELATED:

You must be logged in to post a comment.