Since Spotify launched in 2010 the music business has been in an existential crisis. Convinced that ad-supported unlimited free access to on-demand music would ultimately grow recorded music revenues the major labels opted into what may be their worst decision ever. This decision aided by an estimated 18% (or more) equity position in Spotify has not grown overall music revenues over the past five years. In fact, for the year ending 2014 global revenues reported by the IFPI stated that revenues were at the lowest point in decades. So what to do?

For starters the first and most obvious solution would be to eliminate the unlimited ad-supported free access to on-demand music. This is the model that made ad funded, for profit piracy so popular on over half a million infringing links from unlicensed businesses served by Google search and delivered to your inbox by Google Alerts complete with social media sharing buttons. These unlicensed businesses are receiving hundreds of millions of DMCA notices annually from artists and rights holders. Let us not forget that this is also the same model that Daniel Ek helped to perfect as the CEO of u-torrent the worlds most installed bit-torrent client. Ek has said he’d rather shut down Spotify than give up his failed ad supported business model. We thought Spotify was built on converting ad supported (where Spotify board member Google makes money serving ads) to subscription (where artists make money). So much for that.

And this is who the record business is taking notes from? Perhaps that’s why Universal is restructuring. This may have seemed like a good idea to some senior executives but it turned out to be a complete disaster. Time to change.

Despite moves in the right direction by Tidal and Apple Music the optics for both of these companies at launch of their respective streaming models have been somewhere between missteps and an absolute disaster. Dismissing for a second that both Apple and Tidal could be the targets of public relations campaigns by competing corporations such as Spotify, Pandora and Google (YouTube) let’s look at what each is offering. Tidal and Apple Music offer no unlimited ad-supported free access to on-demand music. That means no business to those selling advertising… like, Google.

There is nothing more important to the future of the recorded music ecosystem than removing the unlimited ad-supported free access to on-demand music.

For all intents and purposes even free streaming is ownership and here’s how you can tell. If you can chose it, and access it, you essentially own it whether you pay for it or not. Streaming replaces ownership at the consumer level but does not compare to ownership on price. At some point there needs to be a market correction to properly value music consumption.

The launch of Tidal should have been a rallying cry for all artists to support a business model that limited free streaming, incentivized paid subscriptions through exclusive offerings and diversified consumer experiences with higher quality streaming formats. This is the model we should be focused on. As the Buddhist saying goes, “trust the teaching, if not the teacher.” In other words it doesn’t matter if you don’t like Jay-Z and Madonna. And securities laws makes the whole stock issue so difficult that Tidal would have been far better off saying they’d pay all participating artists a bonus in the cash from the company’s own stock sales rather than get down the rabbit hole of who gets stock and who doesn’t.

Unfortunately the celebrity that could have united a community, instead divided it through messaging that most would acknowledge appeared to be less than inclusive. Worse, the optics appeared to be elitist whereby those already rich and famous seemed to be more focused on their own fortunes as opposed to a sustainable ecosystem for the next generation of musicians.

Perhaps if each of the artists at the Tidal launch would have appeared with a developing artist they were supporting the messaging and optics would have been more inclusive and more about community than celebrity.

We have to acknowledge what kind of business we want going forward. Clearly, unlimited ad-supported free access to on-demand music is not working. Both Tidal and Apple Music do NOT have unlimited ad-supported free access to on-demand music. So what’s the problem?

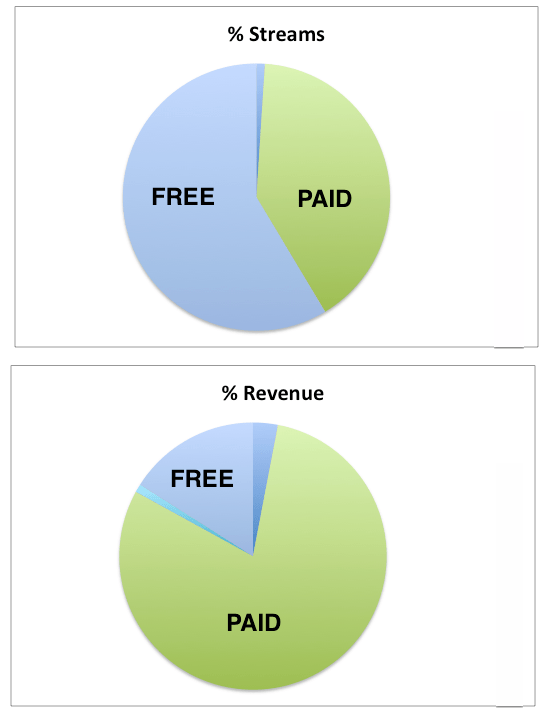

Following the Apple Music launch Spotify announced it had achieved 75m global users (we love that, “users” no kidding) and 20m paid subscribers. So let’s look at the numbers in relationship to what Apple Music could bring to the market place. Keep in mind that 55m of Spotify’s user base are NOT paying for the service. Based on reporting we’ve been provided the free tier accounts for 58% of plays which is only 16% of the total revenue.

With all the back and forth between Apple and labels and the announcement last week by NMPA of the publisher’s deal—freely negotiated without government “help” by the way–it’s pretty clear that Apple announced Apple Music without all their ducks in a row contractually. This opened up an opportunity for haters who are just gonna hate. Now that the picture is becoming a bit clearer, we feel more confident than ever that most of the noise is coming from competitors who would like to create yet another consent decree situation but this time for artists and record companies.

So there are a few questions we need to ask about the launch of Apple Music to evaluate the trade-off for eliminating the unlimited ad-supported free access to on-demand music. But before we ask those questions, we need to understand the mechanics of the Apple Music ecosystem.

First, the 90 days free without payment at launch requires the understanding that all consumers will get 90 days free at Apple Music whether they sign up at launch or at any other point later. This means that some people will opt in at launch, some will opt in at some later time. Based on what we have seen of how these streaming subscription services scale we have to ask a few questions.

How many people will have access to opt into Apple Music Streaming on launch? We’ll assume it’s the entire installed user base who upgrade into iOS 8.4. Here’s some back of the napkin math from the iPhone 6 launch when Apple dropped that U2 album into everyone’s Itunes.

According to CBS News 33 Million people of the 500 Million Global Itunes users “experienced” the U2 album. That’s just 6.7 percent of Apple’s reported consumer base.

So what kind of adoption and conversion rate could one expect from the launch of Apple Music? 10 million paid subscribers? 20 million paid subscribers? 50 million paid subscribers? It’s hard to know, but anything north of 20 million pretty much beats Spotify on paid subscribers. And if you are looking for the company that has defined a paid music service, who you gonna call? Apple or Spotify? Who do you trust going forward?

What if Apple is able to convert 30 million or more consumers to paid streaming in only four months when it has taken Spotify five years to acquire 20 million paid?

BREAKING NEWS AT PRESS TIME. APPLE WILL PAY ARTISTS DURING THE FREE TRIAL PERIOD!

Apple Reverses Course, Will Pay Artists During Apple Music Free Trial | Mac Rumors

Of course, Apple should use a couple of bucks from it’s 178 billion dollars in cash reserves to compensate musicians for the consumption of their music during the initial 90 day launch of Apple Music. This would incentivized artists to promote the service as being both fair and artist friendly and give Apple the thumbs up from the people that matter the most, the artists themselves. Apple’s purchase of Beats was a three billion dollar acquisition, so surely there’s enough money in those coffers to pay artists something.

To put these numbers into perspective Spotify claimed to have paid artists and rights holders two billion dollars globally from it’s initial launch in 2008 through October of 2014.

Here’s some more perspective from asymco.com: In 2012, global music revenues were reported at $16.5 billion, with $5.6 billion coming from digital music. Of that $5.6 billion in music downloads, Apple paid labels $3.4 billion for iTunes sales, which is about 60% of the total digital revenues industry wide—IN LESS THAN ONE YEAR.

In 2012, Apple’s transactional digital model created more revenue for artists and rights holders in less than a year in then it took for Spotify to earn almost 6 years.

If we want to break the death spiral of unlimited ad-supported free access to on-demand music we have to embrace the trade-off of offering limited free trial periods as an incentive for consumers to make the switch.

And by the way—compare the classy way that Eddie Cue of Apple handled Taylor Swift compared to Daniel Ek who comes off like a semi-stalker. Who understands artist relations the best?

The problem with ad-supported unlimited free access to on-demand music is illustrated below showing Spotify domestic streams and revenues. It’s just math and it’s time to move on. Apple Music and Tidal are showing us the way.

You must be logged in to post a comment.