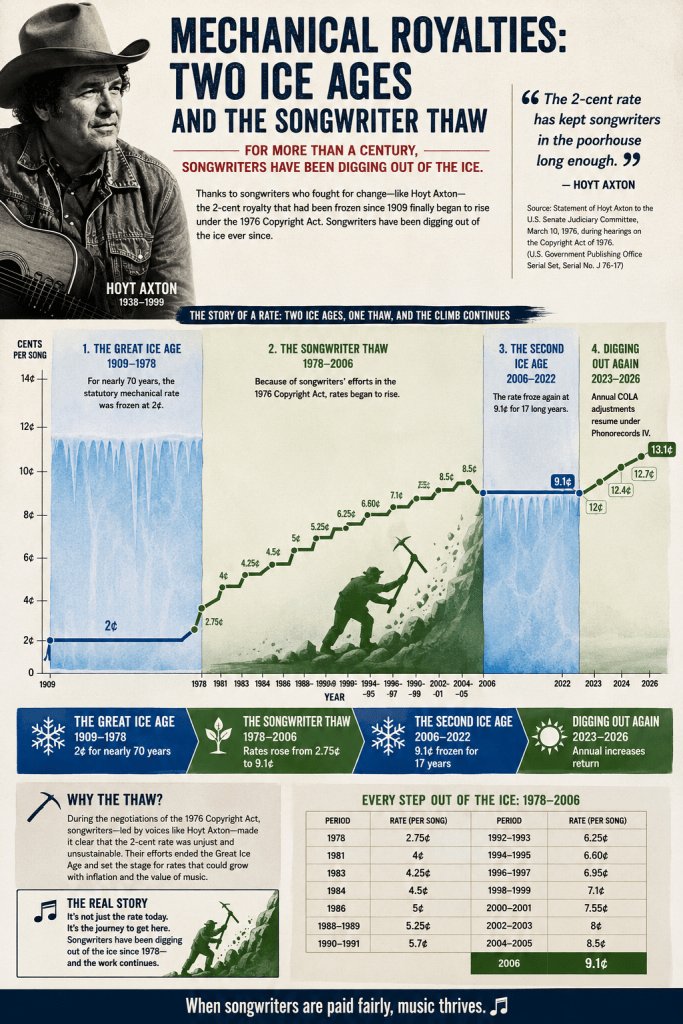

The compulsory mechanical license was created by Congress in the Copyright Act of 1909 as a response to the rise of player pianos and piano rolls, which threatened to place control of a new music reproduction technology in the hands of a few dominant companies. To prevent monopoly control, Congress established a compulsory license allowing anyone to reproduce a musical composition upon payment of a statutory royalty. That royalty was set at 2 cents per song. Remarkably, the 2-cent rate remained unchanged for nearly seven decades, surviving the birth of commercial radio, records, tapes, and the modern recording industry until the Copyright Act of 1976. Given that the dominant music users are either monopolies themselves or effectively monopolies (Google, Amazon, Spotify), the entire purpose of the compulsory license seems laughable today, but oh, well—they’re from Washington and they’re here to help.

The Copyright Act of 1976 did more than end the 2-cent mechanical royalty freeze. It established a framework for periodic review of statutory rates so that songwriters would not again be trapped for generations at a rate set by Congress decades earlier. Over time, Congress refined that system, eventually replacing ad hoc adjustment proceedings with the modern Copyright Royalty Board (CRB). Today, the CRB conducts recurring rate-setting proceedings that evaluate economic conditions and marketplace developments. While the process is often contentious, the result has generally been upward movement in mechanical royalties, reflecting inflation, changing markets, and the enduring value of musical works.

The next mechanical royalty rate-setting hearings before the Copyright Royalty Board are upon us (called “Phonorecords V” follow it here). Like so many other aspects of the CRB, it seems that awareness of the hearing varies inversely to its economic importance for songwriters—meaning that the more it affects your pocketbook, the fewer people appear to know about it. Let’s see if we can change that dynamic.

The CRB will set rates for streaming mechanicals, a whole saga unto itself, but the Board also sets rates for the sale of physical records like vinyl and permanent downloads. It was these rates that created a dust up the last time around in Phonorecords IV, because the first tentative settlement was rejected by the Judges. Had the Judges not rejected the first settlement, the insiders would have frozen the physical/download rates for another five years in addition to the freeze that was already in place since 2006 for a total of 21 years.

The PR V resolution should be simple: whatever inflation-adjusted rate that is in effect at the end of the Phonorecords IV rate period should become the starting point for the next rate period in Phonorecords V. Why? Because the CRJs proposed the 12¢ PR IV base reference rate (plus COLA) as a compromise recognizing that the statutory rate had not been adjusted for inflation from 2006 through 2023. Having adopted an actual inflation-adjusted rate through a revised settlement in PR IV, choosing to revert to 12¢ in 2026 for PR V would effectively disregard the very rationale that justified the compromise in the first place. There’s nothing economically magical about a 12¢ rate in 2022 that should inform a new rate in 2028.

Yet there is a risk that some stakeholders may argue that the 12¢ reference rate established in Phonorecords IV should remain the permanent benchmark and that future proceedings should effectively restart from that 12¢ figure even though they know that the real rate is actually the inflation adjusted rate. This is the kind of thing lawyers come up with and is completely divorced from reality.

If the CPI-adjusted rate reaches approximately 13.6¢ by 2027, as current inflation projections suggest, such a 12¢ approach would amount to an immediate reduction in songwriter and publisher compensation. Rough justice, that 12¢ rate would actually be worth around 11¢ today, so asking for a 12¢ reference rate is like saying would you take 11 which would be roughly a 20% reduction. That would make little sense economically, legally, or as a matter of regulatory policy.

The key point is that the annual CPI adjustments adopted in Phonorecords IV are not temporary bonuses. They are part of the rate structure. The Judges did not establish a 12¢ rate and then provide a series of discretionary supplements. Rather, they established a rate that increases annually according to a defined formula. The resulting rate is the actual statutory royalty rate in effect at the time. If the rate reaches 13.6¢ in 2027, then 13.6¢ is the reference rate for PR V.

Resetting the benchmark to 12¢ would create a downward ratchet unlike anything that participants in a functioning market would expect not to mention in the post-1978 history of the Copyright Act. Songwriters and publishers would receive annual increases throughout the rate period only to see those increases erased at the start of the next one. Such a result would be arbitrary and would undermine confidence in the stability of the statutory license.

For years, the mechanical royalty remained frozen at 9.1¢ while inflation steadily eroded its economic value. Phonorecords IV represented an acknowledgment that perpetual freezes are difficult to justify in a modern economy. It would be strange indeed if the solution to one rate freeze were simply to create another.

There is also a practical problem. If the statutory rate can be reset downward whenever a new proceeding begins, then the annual CPI adjustment becomes less meaningful. Parties will spend years litigating a rate structure only to find that the resulting increases can be wiped away at the start of the next cycle. That is not how durable rate regulation is supposed to work.

The cleaner approach is the obvious one. The final rate in effect during one period should become the reference rate for the next period unless the evidentiary record demonstrates that a different rate is warranted. This is how the rate was set from 1978 to 2006 and how most regulated systems operate. The existing rate serves as the baseline, and adjustments are made from there.

The issue is ultimately one of continuity. The statutory mechanical royalty should evolve through evidence-based proceedings, not through accounting tricks that erase previously awarded increases. If the rate reaches 13.6¢ in 2027, then 13.6¢ should become the starting point for the next rate period.

The rate clock should move forward, not backward. A songwriter named Hoyt Axton worked his tail off getting the rate on a track to increase with the passing of the 1976 Copyright Act. And I for one will never forget him.

[A version of this post first appeared on MusicTechPolicy]

You must be logged in to post a comment.